.png)

.png?width=171&height=239&name=2025%20Trends%20Report%20Nav%20(1).png)

CMS recently reported that the U.S. health economy represents $4.3T of GDP, a 4.9% increase over 2020 as a result of higher prices for all services for all payers (i.e., Medicare, Medicaid, and private insurers) and increased spending on retail prescription drugs.1

The only thing that grows faster than U.S. health spending is the number of initiatives to improve the financing, delivery, and organization of healthcare services. Between Christmas and New Year’s, analysts, researchers, consultants, executives, and financiers perennially cast their predictions for the industry in the year to come.2,3,4,5,6,7 A review of these predictions suggests that remote patient monitoring, retail-based care, and e-prescribing will continue to – or finally be – key developments in 2023, while emerging trends, such as genomics, may gain traction. Last week’s J.P. Morgan Healthcare Conference was replete with these themes in sessions, articles, and company presentations.

This special edition of The Compass seeks to analyze a few popular 2023 health economy predictions by raising key questions that will ultimately influence the trajectory and implications of these projections.

Veteran healthcare professionals will continue to leave the workforce, but to what extent will the resulting void in experience have longstanding consequences for the next generation?

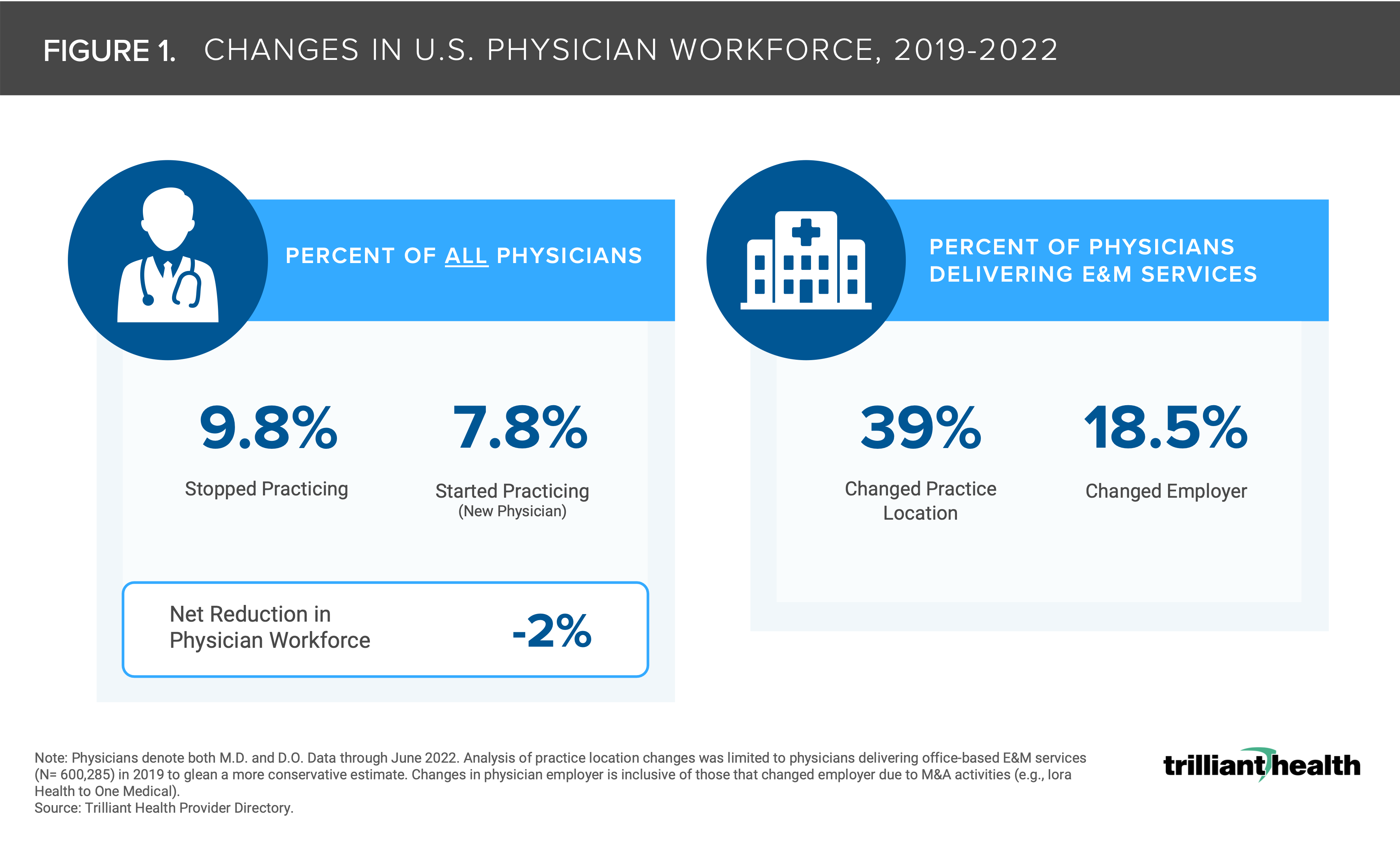

While burnout in the healthcare workforce has been present for years, the COVID-19 pandemic exacerbated the workloads and seemingly catalyzed increased violence towards workers, accelerating a decline in supply of clinicians (e.g., Great Resignation, early retirement). In turn, the shortage of nurses has constrained staffed bed capacity for hundreds of hospitals. The net difference between the number of physicians starting and stopping practice from 2019 to 2022 represented a 2.0% decline, and the Association of American Medical Colleges projects the physician gap will range from 27.8K (25th percentile) to 124K (75th percentile) by 2034 (Figure 1).8,9

Notably, physicians, nurses, support staff, etc. with the most experience represent the largest segment of those exiting the workforce. The physicians, nurses and other healthcare professionals who switch employers (e.g. inpatient settings to ambulatory and retail settings), retire or leave the industry sooner than anticipated take their experience with them, leaving new medical and nursing school graduates with fewer opportunities to learn from tenured colleagues and patients to be treated by less experienced caregivers (i.e., “an experience-complexity gap”).10,11

-

Will Congress pass meaningful legislation (e.g., financial incentives) to bolster the physician and allied health workforce to address the persistent shortage and levels of burnout?

-

Could major changes to scope of practice for non-physician providers address the gap in experience and volume of providers, and is Congress willing or able to preempt state licensure requirements?

-

Will the increasing trend of physicians becoming employees, whether by a traditional provider, payer or retail player, further alter the composition and expectations of the provider workforce and resource allocation across all employer types?

-

With fewer experienced physician mentors, will the nation’s medical education system be equipped to sufficiently motivate and guide future trainees?

Some think that remote patient monitoring (RPM) is here to stay, but how will adoption grow when the current rate of change is slow?

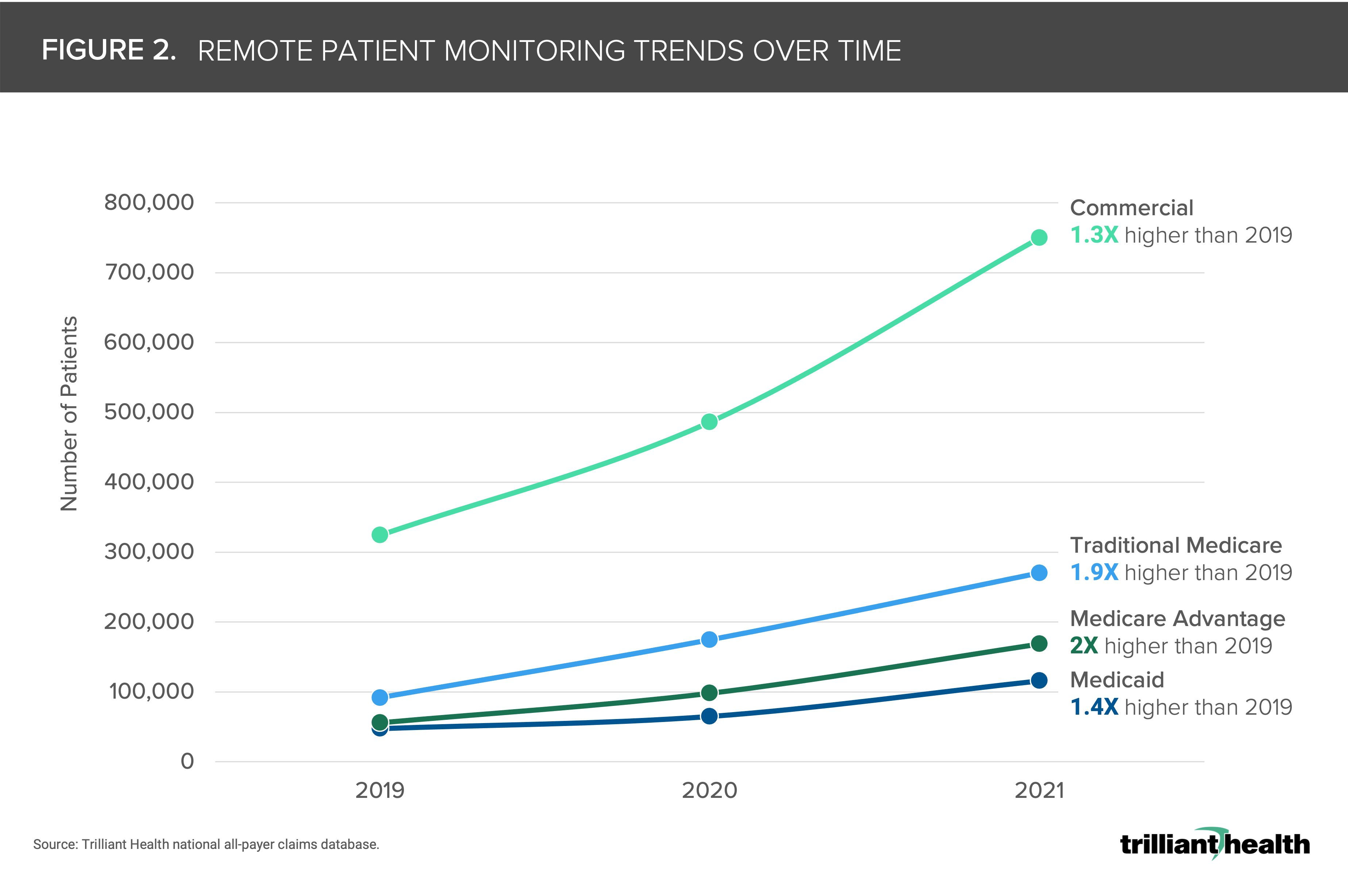

RPM, defined here as the automated collection of patient physiological measurements and asynchronous delivery to health care practitioners, is frequently used for cardiology and pulmonology patients.12

While some digital health proponents tout continued proliferation of the technology, the pace at which adoption is happening is slow. Between 2019 and 2021, the increase in the number of patients with a RPM claim ranged from 1.3X (commercially insured) to 2X (Medicare Advantage) (Figure 2). As also noted in Figure 2, RPM is currently utilized by a small patient population (<5% of Americans) with recent utilization increases attributed to a select few providers.13 While interest in RPM is growing as a result of technological advancements, pandemic-related increase in virtual care for specific use cases, and expanded reimbursement,14,15,16 the long-term viability of RPM remains to be seen. As a passive technology, RPM is inherently different from telehealth – which, despite pandemic-induced increases in utilization, is also still used by a small share of the population at <30% of Americans. However, the same access, technology, and quality barriers to telehealth also apply to RPM.17

-

What levers (e.g., is it a provider preference or comfort with technology) are needed to facilitate greater provider uptake of RPM for treatment of chronic disease patients, both regionally and across clinical areas?

-

What are the implications for RPM if quality assessments conclude that RPM is not as clinically effective as in-person monitoring? How will policymakers and payers balance the benefits of continuous, but possibly lower quality, RPM with higher quality, but intermittent, in-person care?

-

Given the rapid deceleration in digital health investments, will RPM utilization plateau or even decline similar to trends of reduced use of telehealth for non-behavioral health conditions?

M&A activity is predicted to grow, but can every healthcare company benefit from that growth?

In 2023, Forbes and the American Hospital Association (AHA) predict a “feeding frenzy” in venture capital and private equity (PE).18,19 Women’s health has drawn increased attention from investors in both the technology (i.e., patient communication and medication adherence) and specialist providers in consulting and family planning (i.e., fertility, IVF). Even so, many digital health companies will be forced to choose from unattractive options, including attempting to raise capital under unfavorable terms, implementing layoffs to preserve cash, or selling the company in a distressed market environment. Companies that cater to specific conditions through targeting poorly managed diseases may be particularly vulnerable, as they struggle to sustain a smaller total addressable market. At the same time, financial buyers impacted by higher interest rates, threats of recession, and tight credit markets will be more risk-averse to companies without positive cash flow.20

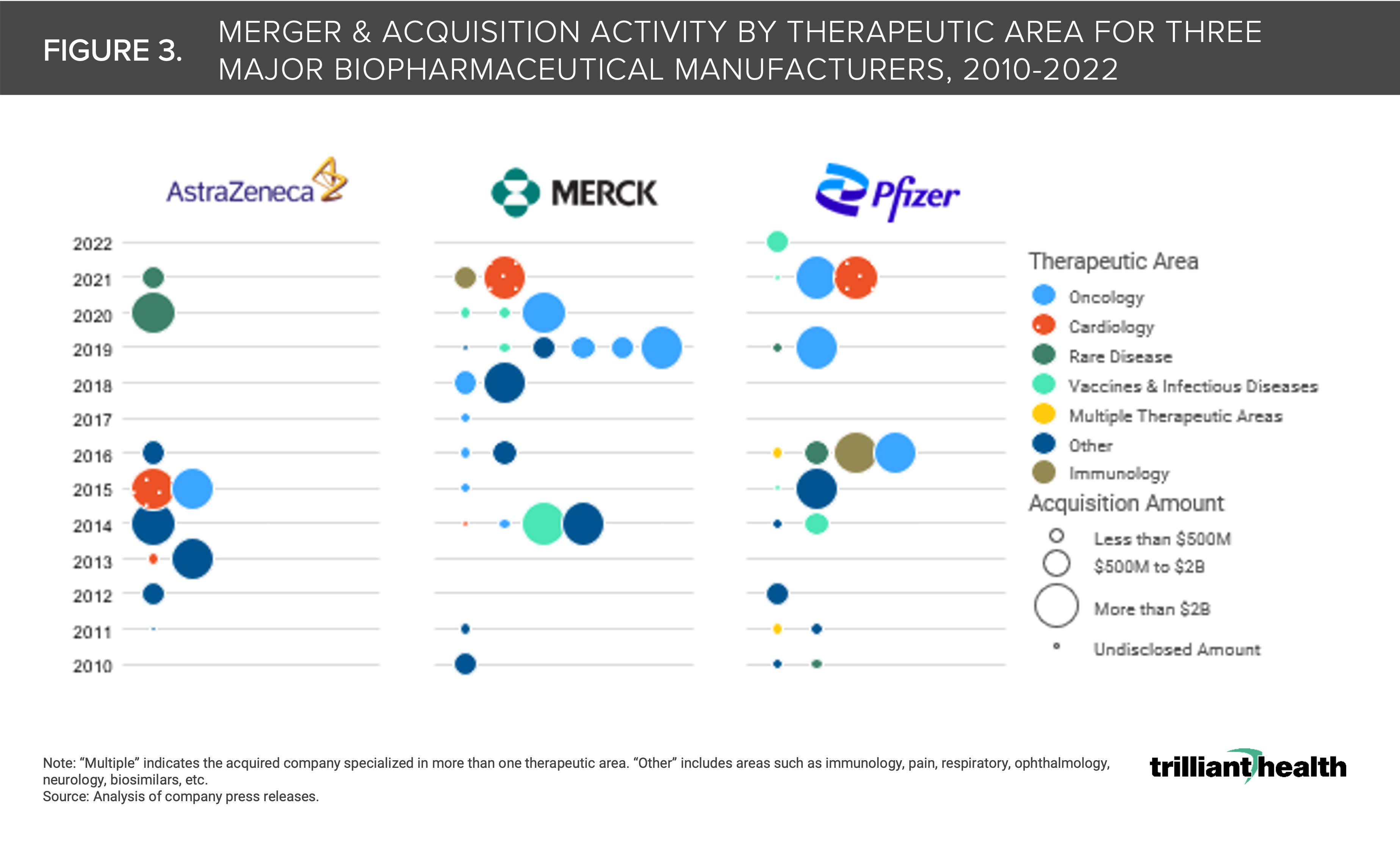

In contrast, challenging market conditions should have a more limited impact on M&A in the life sciences sector. Oncology, cardiology, and immunology were the focus of increased activity over the past decade, with even larger deals occurring in the past few years (Figure 3).

-

Will PE activity in areas like women’s health materially move the needle in the quality and equitable distribution of care?

-

What is the viability of digital health investments, given the notable 48% decline in funding totals in 2022 compared to 2021?

-

Will niche digital health companies faced with limited growth prospects due to a discrete patient population focus their efforts on increasing the number of users or pivot to expanding the number of services per user?

Retail keeps expanding its healthcare footprint, but how threatening is that expansion to traditional primary care providers?

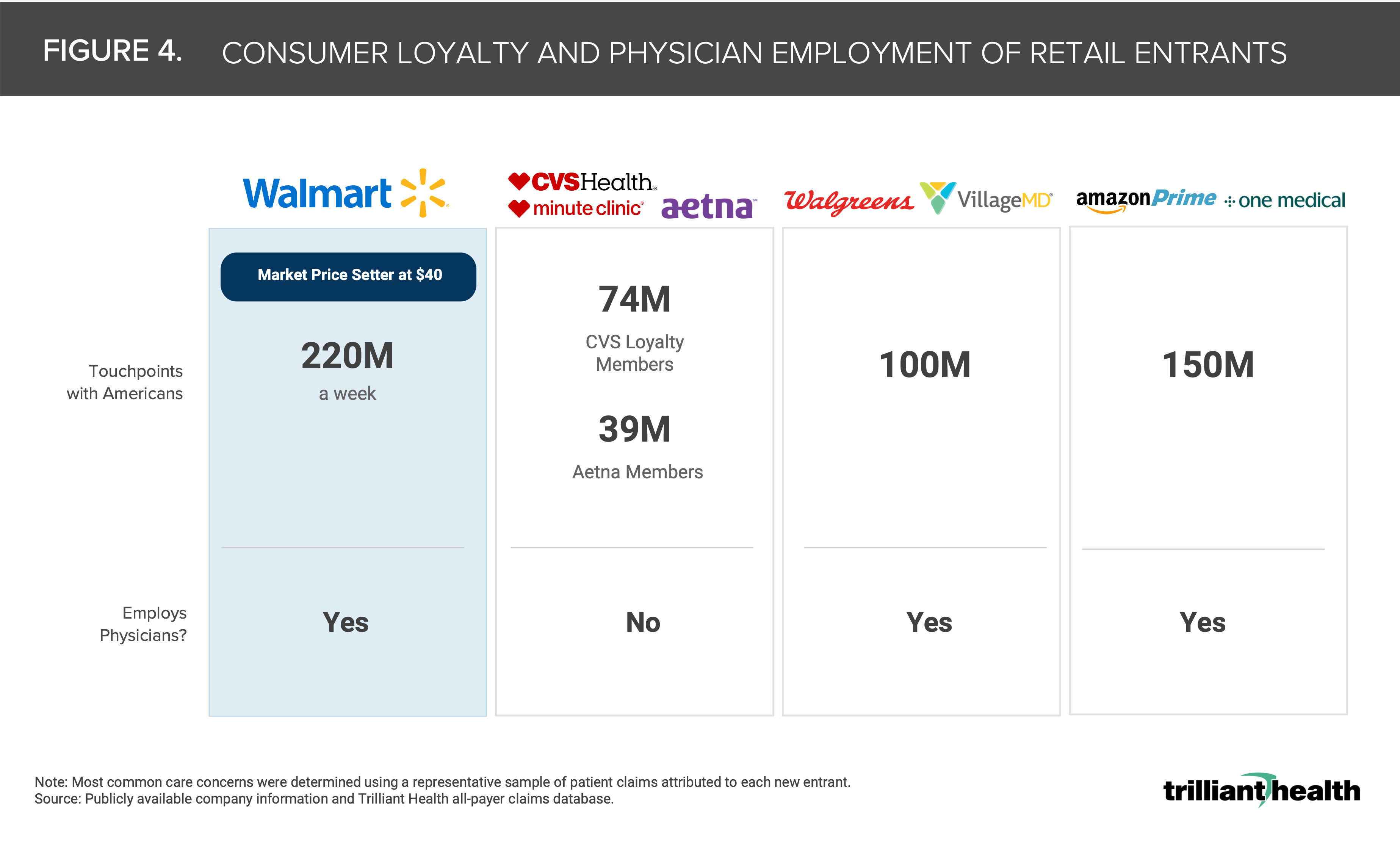

Much has been written about the implications of large retailers such as Amazon, CVS, Walgreens and Walmart entering the healthcare market, offering consumers more convenience and lower prices for low-acuity services (Figure 4).21,22,23,24,25 The so-called “retailification” of primary care will increase clinical fragmentation, which the AHA cautions will lead to inconsistent quality.26 What is lost in the media interest of Amazon, CVS and Walgreens’ acquisition of primary care companies is the inherently flawed business model of the companies being acquired.27 One question is whether Walmart follow suit by acquiring a primary care operator or leverage their new partnership with United, the largest employer of physicians in the U.S.? Another consideration is whether the large retailers will adapt their primary care models to mimic successful operators like LEON Medical Center or, alternatively, will treat primary care as a “loss leader.”

-

Are traditional players (i.e., hospitals and health systems) “okay” with lower-acuity patients moving towards retail and tech-enabled settings of care and focus more resources on treating the sickest patients?

-

How will referral patterns, coverage arrangements, and physician networks be fragmented as more low-acuity services are delivered outside of traditional settings of care.

-

If retailers do embrace a “loss leader” mindset for delivering primary care, how soon will these players see revenue growth across their other business lines?

Precision medicine and genomics are predicted to further personalize healthcare, but how long will it be until we see the impacts on the nation’s overall burden of disease?

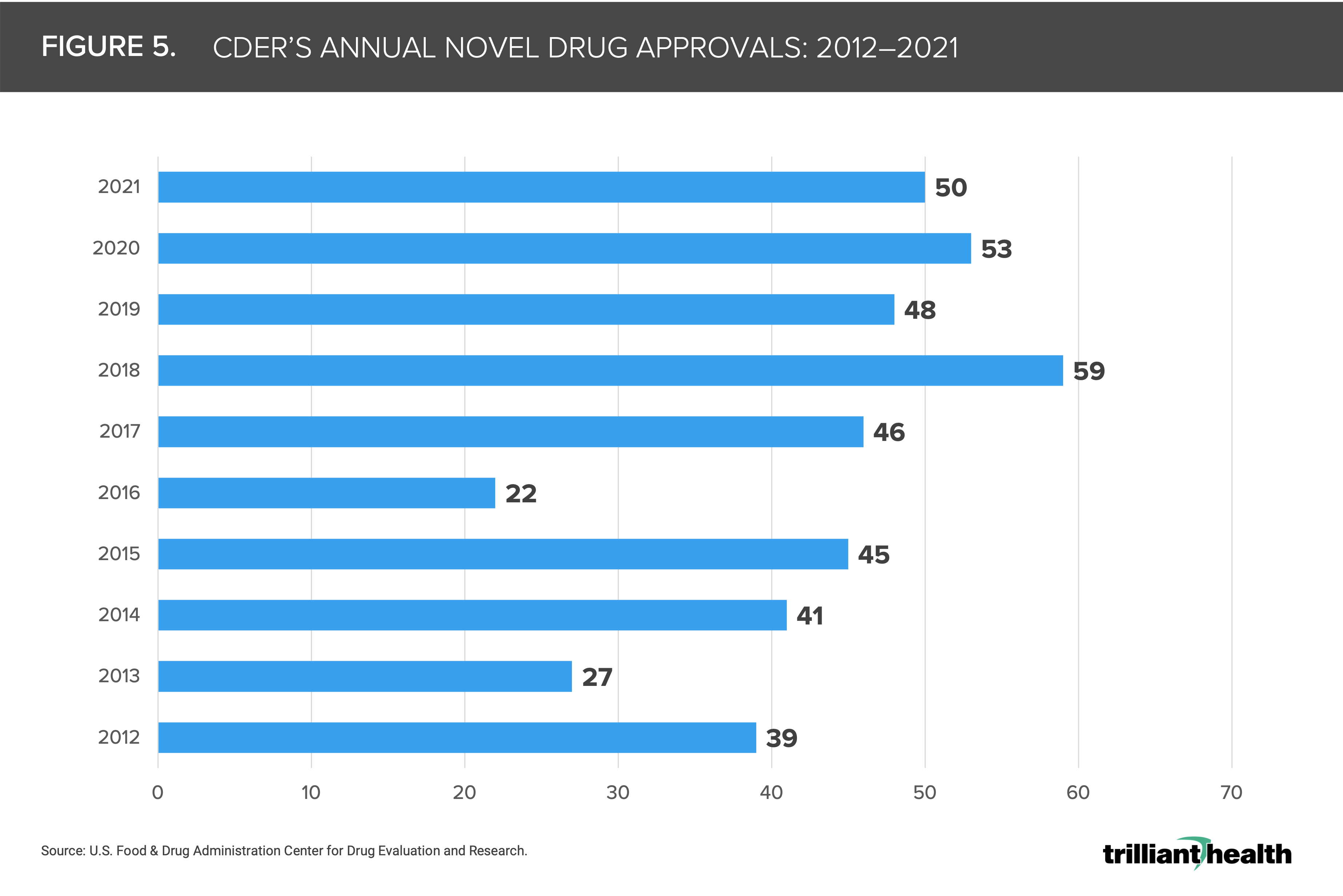

Gene therapy approvals doubled in 2022, most notably Zolgensma for spinal muscular atrophy that generated $1.5B in 2021, only two years post-approval.28 Increases in precision medicine will focus on factors such as age and genetics to create tailored treatment to individuals. In an effort to combat COVID-19 variants, the Biden administration announced a $1B investment to expand genomic sequencing to help the CDC, states, and other jurisdictions to identify mutations and monitor variants and an additional $400M to support innovation initiatives, such as the launch of the new Centers of Excellence in Genomic Epidemiology.29 The FDA’s Center for Drug Evaluation and Research (CDER) averaged 43 novel drug approvals per year, with 54% of drugs approved in 2021 deemed “first-in-class” (Figure 5).30

-

Given the high costs related to precision medicine treatments, are payers and employers willing to absorb these costs as precision medicine expands into more disease states?

-

What are the long-term implications of novel drug development in a research ecosystem where an increasingly large share of R&D dollars are allocated towards diseases with smaller patient populations?

-

Given the increasing pharmaceutical industry energy dedicated to precision testing and medicine with high costs, is there a risk of exacerbating existing inequities in healthcare access?

Conclusion

While this summarized list of healthcare predictions is not remotely exhaustive, each of the highlighted topics are top of mind for many stakeholders across the healthcare industry. Every payer, provider, life science company – and consumer – has a stake in every topic, and 2023 holds the potential for advancements (e.g., developments in genomics) and challenges (e.g., continued financial strain for providers and patients alike) for the $4.3T health economy. While predictions may provide insight to what is top of mind for each stakeholder group in 2023, the pace at which these predictions manifest will inevitably extend beyond this year.

Thanks to Katie Patton for her research support.