.png)

.png?width=171&height=239&name=2025%20Trends%20Report%20Nav%20(1).png)

Key Takeaways

-

Through a majority investment in VillageMD, Village Medical at Walgreens will provide integrated primary care in coordination with Walgreens pharmacists.

-

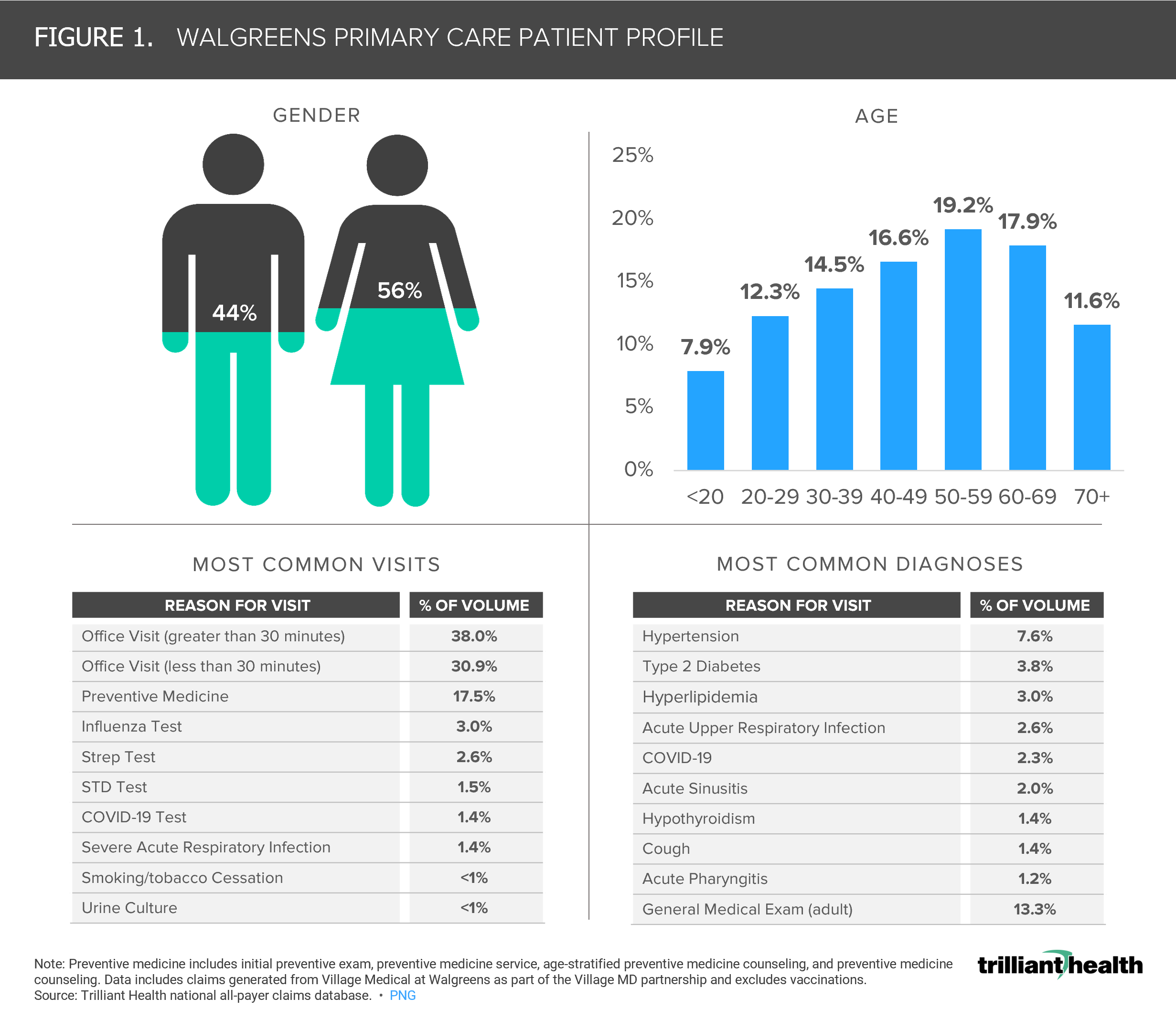

Of the patients receiving healthcare services via Walgreens, approximately 56% are female and nearly half (48.7%) are 50 years of age or older.

-

Compared to its competitor CVS, the patient profile of a Walgreens patient is, on average, 9.6 years older.

In part one of our “Characterizing the Patient Populations of New Entrants” series, we analyzed CVS Health’s patient population to begin to understand its foray into the care delivery market.1 In this second edition of the ongoing series, we take a deeper dive into Walgreens and its expansion into the primary care market.

Background

Walgreens continues to evolve from a drugstore and retail pharmacy to a full-service healthcare provider. Walgreens has expanded its capabilities from preventive care and wellness visits to chronic condition management, even employing full-time physicians.2 Evaluating the extent to which Walgreens is disrupting traditional care delivery begins with understanding who they are treating.

Walgreens has introduced in-store health clinics in large part to counteract increasing competition from retailers like CVS, Walmart, and Amazon.3,4,5 With an 18% share of the prescription drug market, second only to CVS at 24.5%, and its sizeable investment in VillageMD, Walgreens is now positioned as the first national pharmacy chain to offer full-service primary care practices with primary care physicians and pharmacists.6,7

Walgreens’ multi-billion-dollar investment in VillageMD is the foundation of Walgreens’ primary care strategy. Walgreens recently expanded its pharmacy capabilities by acquiring Welsh Carson’s (WCAS) interest in Shields Health Solutions, providing Walgreens with 100% ownership of a premier health system-owned specialty pharmacy integrator with partnerships with 30 health systems.8 Walgreens also consummated the acquisition of a majority ownership in CareCentrix, the leading independent home-centered platform.9 Through its investments in VillageMD, Shields, and CareCentrix, Walgreens has expanded its reach in the health sector and positioned itself as a formidable competitor in the primary care market.

In partnership with Walgreens, Village Medical, a subsidiary of VillageMD, has announced plans to open more than 600 primary care clinics in over 30 U.S. markets over the next four years, with a sizeable share in medically underserved communities.10 According to CEO Roz Brewer, this investment is part of Walgreens’ effort to build “key relationships…with the consumer between the primary care physician and the pharmacist.”11

Analytic Approach

To better understand who seeks healthcare services at Walgreens and why, we leveraged our national all-payer claims database to identify medical services accessed at Walgreens locations across five states. We examined VillageMD-associated claims from Village Medical at Walgreens locations from 2019 to present. The analysis excluded vaccination data. Among this patient panel, we characterized age, and gender, as well as the most common reasons for medical visits.

Findings

Females represent 56% of the patients receiving healthcare services at Walgreens, and 48.7% are 50 years of age or older (Figure 1). The gender distribution of patients seen by Walgreens is comparable to that of its rival CVS Health, which also skews female (59% female: 41% male). The average patient age seen by Walgreens is 48.1, which is 9.6 years higher, on average, than that of CVS.

The most common diagnoses by volume among Walgreens patients are adult general medical exams (13.3%), hypertension (7.6%), Type 2 Diabetes (3.8%), and Hyperlipidemia (3.0%). Notably, 83.3% of Walgreens patients are commercially insured.

The reasons for seeking care are substantially different between Walgreens and CVS’s patient panels. While the greatest volumes for Walgreens patients were related to chronic conditions and general exams (27.7%), CVS patient volumes were largely attributed to general contact with communicable disease and sore throat (86.6%). These findings are not only consistent with the demographics of each retailer, but also suggests COVID-19-related care contributed to a greater share of care for CVS than Walgreens (excluding vaccinations). Given older patients more frequently have an established primary care relationship, the older patients attributed to Walgreens may be more likely to continue pursuing primary care with the retailer.12

The entrance of retailers like Amazon, CVS, Walgreens, and Walmart has resulted in an increasing amount of low-acuity primary care migrating from physician offices to retail locations, meeting increasing consumer demand for fast and convenient access to care. Even so, the American public is accessing primary and preventive care services at a lower rate than pre-pandemic despite increased access to multiple healthcare services and platforms, including walk-in care at retail clinics.13

The convergence of flat to declining demand for primary care services together with increasing supply of primary care providers provokes many questions. How will the migration of primary care from established primary care physicians to more transactional retail providers affect traditional referral relationships between primary care and specialist physicians? How will care coordination initiatives be impacted with so many different retailers competing to provide low-acuity primary and preventive care? Can retailers with longstanding consumer loyalty programs leverage those relationships to expand their “share of care” for healthcare services? Or will retail healthcare companies continue their dependence on acquiring physician practices to grow their primary care patient volume?

Thanks to Megan Davis and Austin Miller for their research support.