.png)

.png?width=171&height=239&name=2025%20Trends%20Report%20Nav%20(1).png)

Key Takeaways

-

It is widely understood in the care delivery business that primary care is a loss leader. However, companies like CVS, Amazon and Optum have the pharmacy distribution, scale and consumer loyalty to absorb the financial losses associated with primary care.

-

Nationally, about 66% of American adults have a chronic condition, while 96% of Oak Street Health (OSH) patients had at least one chronic condition in 2022.

-

The OSH acquisition does not meaningfully change the CVS patient population, as Aetna already has 3.1M Medicare beneficiaries enrolled in Medicare Advantage plans. But with CVS’s scale, they can afford to absorb OSH’s significant operating losses in exchange for expanded prescription distribution and general retail sales.

Earlier this month, CVS Health (“CVS”) joined the ranks of Amazon, Walgreens and Optum in expanding its primary care capabilities by agreeing to acquire Oak Street Health (“OSH”) for $10.6B (including debt), a transaction that is expected to close in 2023.1 Beginning with its acquisition of Aetna in 2018, CVS has made significant investments in the payer, primary care, virtual care and home care markets.

For decades, health systems have underwritten losses associated with primary care practices as a “loss leader” that generates referrals for higher acuity, and more profitable, services. Large retailers cannot offset primary care losses from orthopedic surgery, for example, which raises this question: Do Amazon (One Medical), Walgreens (VillageMD and Summit Health), and CVS (OSH) believe they can operate primary care practices more profitably than healthcare executives?2,3 Or do those retailers have a different strategy to offset the losses that are reliably generated by employed primary care practices? One thing that Amazon, CVS, Optum and Walgreens have in common is the pharmacy distribution, scale and consumer loyalty to absorb the financial loss from owning primary care operations.4

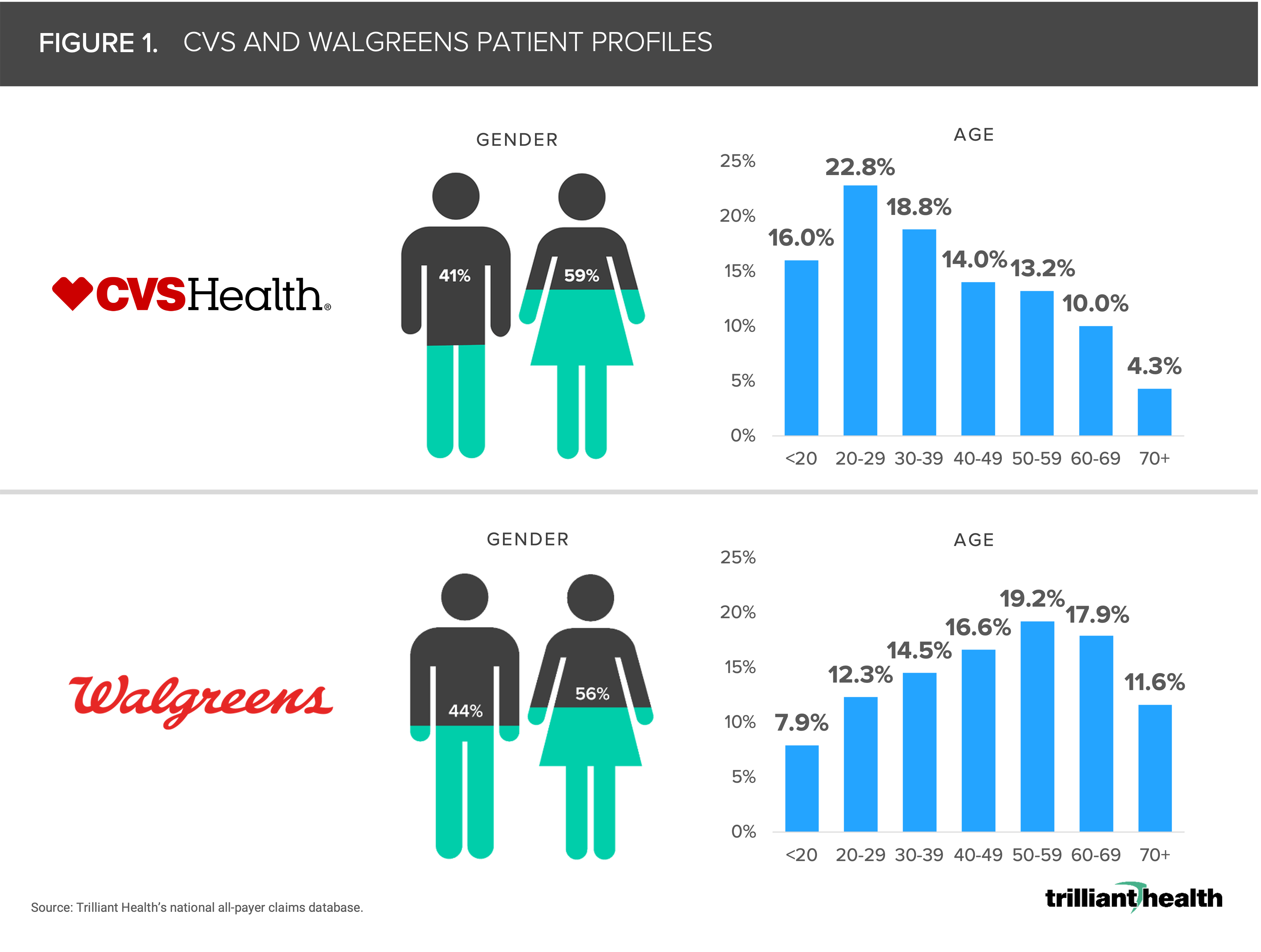

Previous research found that the current patient population that CVS serves through its urgent and primary care services is young and lower-cost.5 Of the patients receiving healthcare services at CVS, almost 60% are female, while more than 41% were between the ages of 21 and 39, and the most common services are lower acuity (Figure 1). However, the average patient age seen by Walgreens clinics is 48.1, which is 9.6 years higher, on average, than that of CVS.

In contrast to the CVS patient population, OSH’s patient population—which focuses on older adults and is comprised of 159K Medicare Advantage (MA) beneficiaries (0.6% of total MA enrollment)—is characteristically older and sicker, with 42% of their patients being dual-eligible patients.6 OSH’s focus on the MA population is logical, as 47M Americans are projected to be enrolled in MA plans by 2032, representing 61% of all Medicare enrollment.7 Notably, 96% of OSH patients had at least one chronic condition in 2022 as compared to approximately 66% of American adults with a chronic condition. Generally speaking, the more chronic conditions that a patient has, the higher the pharmaceutical expense.

CVS’s proposed acquisition of OSH does not meaningfully change their MA membership, as Aetna already has 3.1M Medicare beneficiaries enrolled in MA plans. But with CVS’s scale, they could afford for primary care to be a loss leader for expanded prescription distribution and general retail sales (Figure 2).

CVS serves 5M pharmacy patients daily.8 OSH’s current provider footprint spans 561 providers and 174 clinics across 21 states, all of which overlap with CVS’s pharmacy footprint. But how much OSH prescription volume does CVS already have? If CVS is focused on increased pharmaceutical distribution, CVS’s interest in OSH implies that CVS can increase its market share with OSH patients. Even so, OSH’s patient population would need to grow substantially for the prescription volume to make a positive financial impact on CVS.

Primary care is a critical function for effective disease prevention and management, particularly for older adults. It remains to be seen whether these retail acquisitions of value-based care providers further streamlines or fragments care coordination for the patients they now serve. How traditional providers view these new retail entrants depends on how referral patterns evolve. If CVS follows Aetna’s traditional provider network strategy, health systems could focus more resources on higher-acuity, specialized care. If not, health systems may be forced to invest more heavily in primary care practices to create a more “closed loop” system of coordinated care.

Thanks to Allison Oakes, Katie Patton, and Chris Rash for their research support.