.png)

.png?width=171&height=239&name=2025%20Trends%20Report%20Nav%20(1).png)

Lower-cost care settings, such as retail clinics, ambulatory surgery centers (ASCs) and virtual care platforms, have emerged as alternatives to traditional, higher-cost settings. These settings can offer more affordable treatment options and address consumer demand for things like convenience and accessibility. However, increasing utilization of alternative care settings underscores broader systemic challenges, such as care fragmentation and questions about long-term cost-effectiveness.

This week, we explore how integrating these lower-cost settings can enhance value, improve outcomes and meet evolving patient needs.

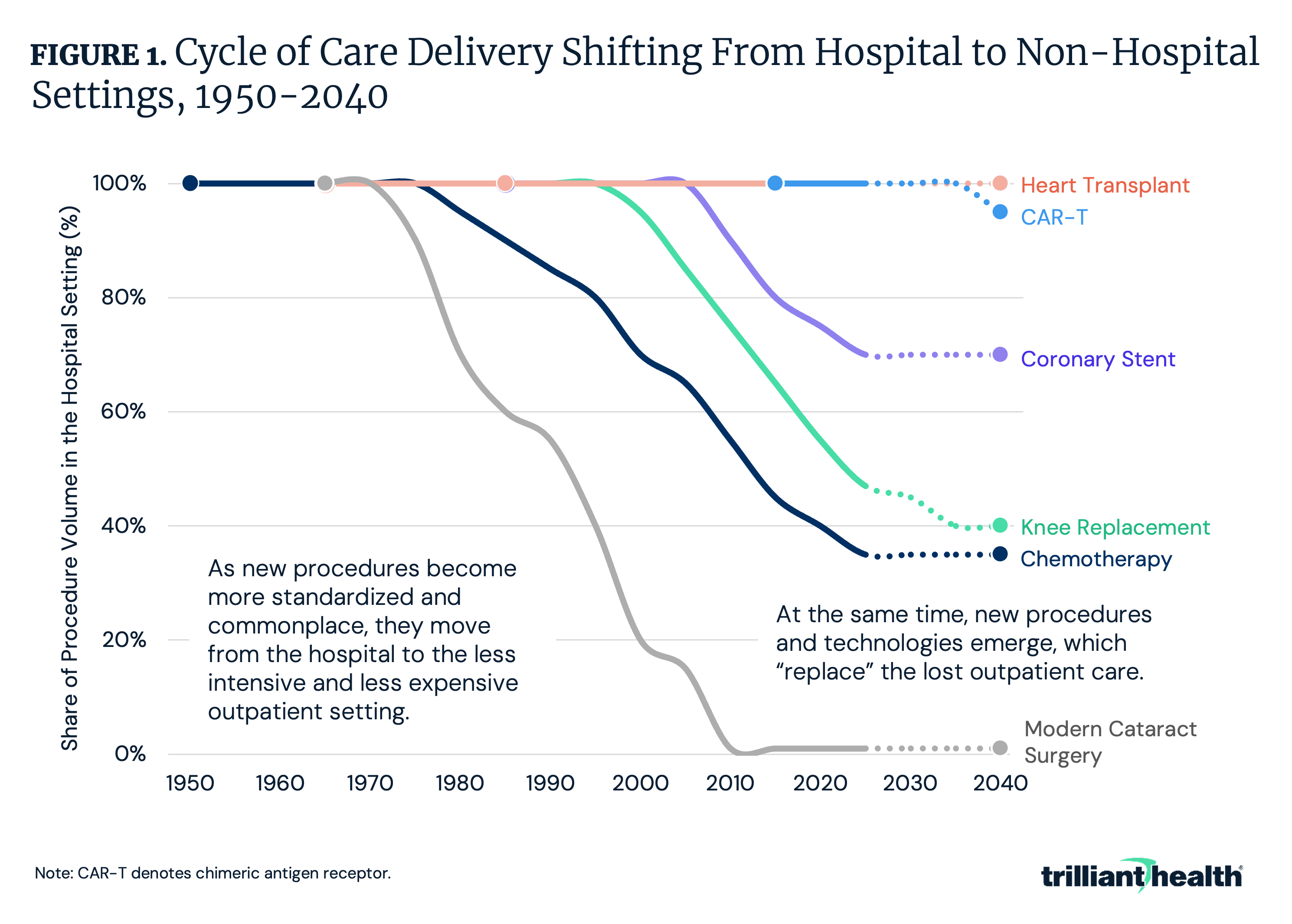

Cycle of Innovation Influences Rate of Care Migration Outside the Hospital

New treatment paradigms often start in the hospital setting. Over time, technology and innovation (e.g., new tools, payment reform) can enable these treatments to transition to outpatient or alternative settings, improving accessibility and reducing costs. Common procedures that increasingly are performed in outpatient settings – joint replacements, coronary stents, chemotherapy, etc. – originated in exclusively inpatient settings (Figure 1). This migration of care to lower-acuity settings is a catalyst for a broader trend in healthcare toward decentralization and consumer-focused care.

Historically, however, as innovation reduces the need for traditional inpatient care, novel complex procedures, such as CAR-T cell therapy, emerge to fill the gap, sustaining the demand for hospital-based services. This “cycle of innovation” raises important questions: will this pattern continue and will future advancements disrupt or reinforce the existing dynamic, especially as the healthcare system grapples with resource constraints and shifting consumer expectations?

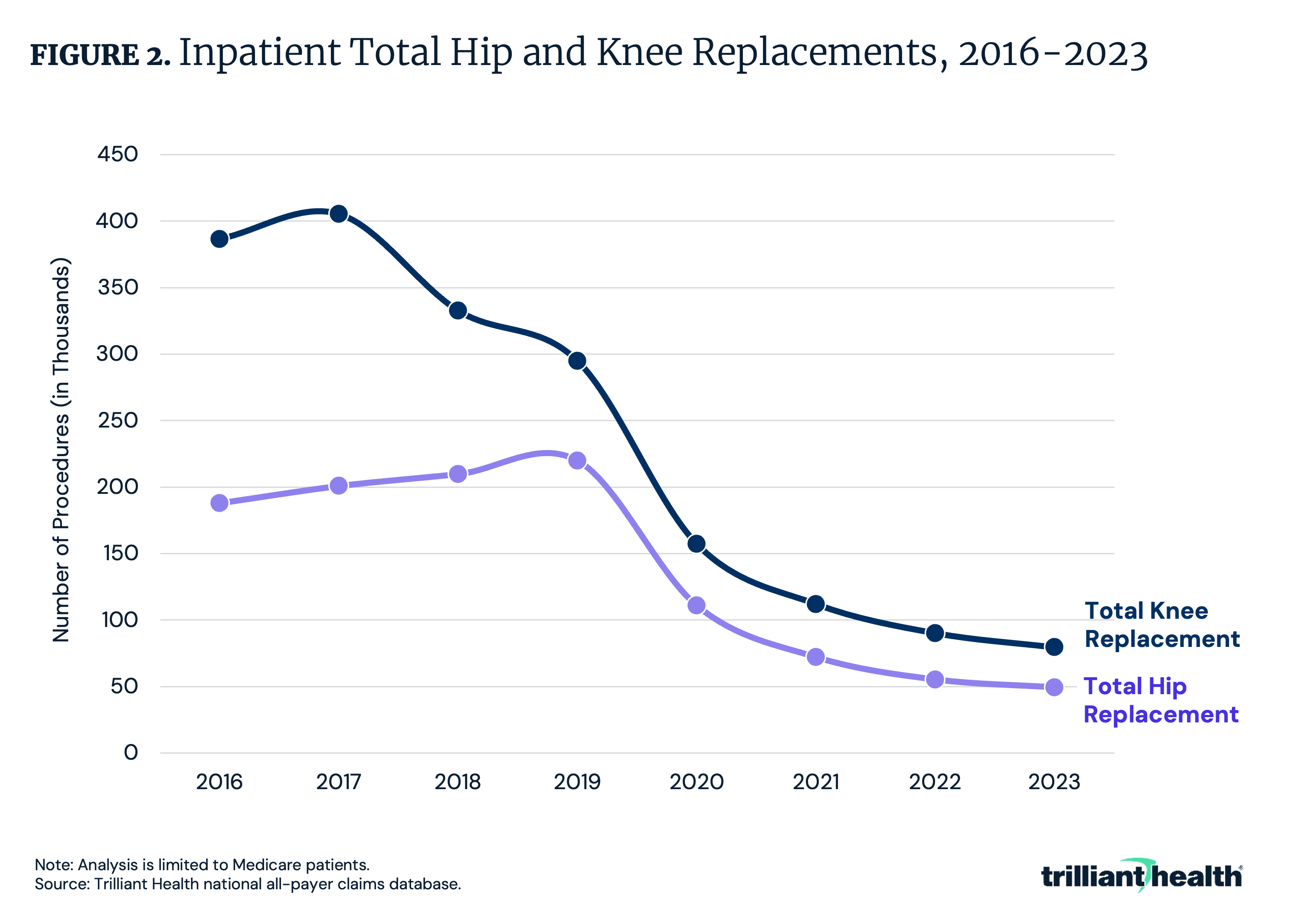

As Procedures Are Removed from the IPO List, ASC Volumes Will Increase

The Inpatient Only (IPO) list is a group of services for which Medicare will only reimburse if performed in an inpatient setting, and the removal of procedures from the IPO list has a substantial impact on inpatient volume. After total knee replacements were removed from the IPO list in 2018, inpatient volume declined by 17.9% from 2017 to 2018 (Figure 2). Similarly, inpatient volume for total hip replacements declined by 35% in the year following their removal from the list in 2020. As surgical procedures are removed from the IPO list, the number of surgeries performed in ASCs and other outpatient settings will increase.

Between 2019 and 2023, the share of ASC-eligible surgeries delivered at ASCs increased by 7.0 percentage points, reaching 50.3% of eligible procedures in 2023.1 Notably, readmissions, post-surgical complications and costs for total joint replacements are lower in outpatient settings compared to inpatient settings, indicating higher value for lower-acuity patients who do not require inpatient care.2

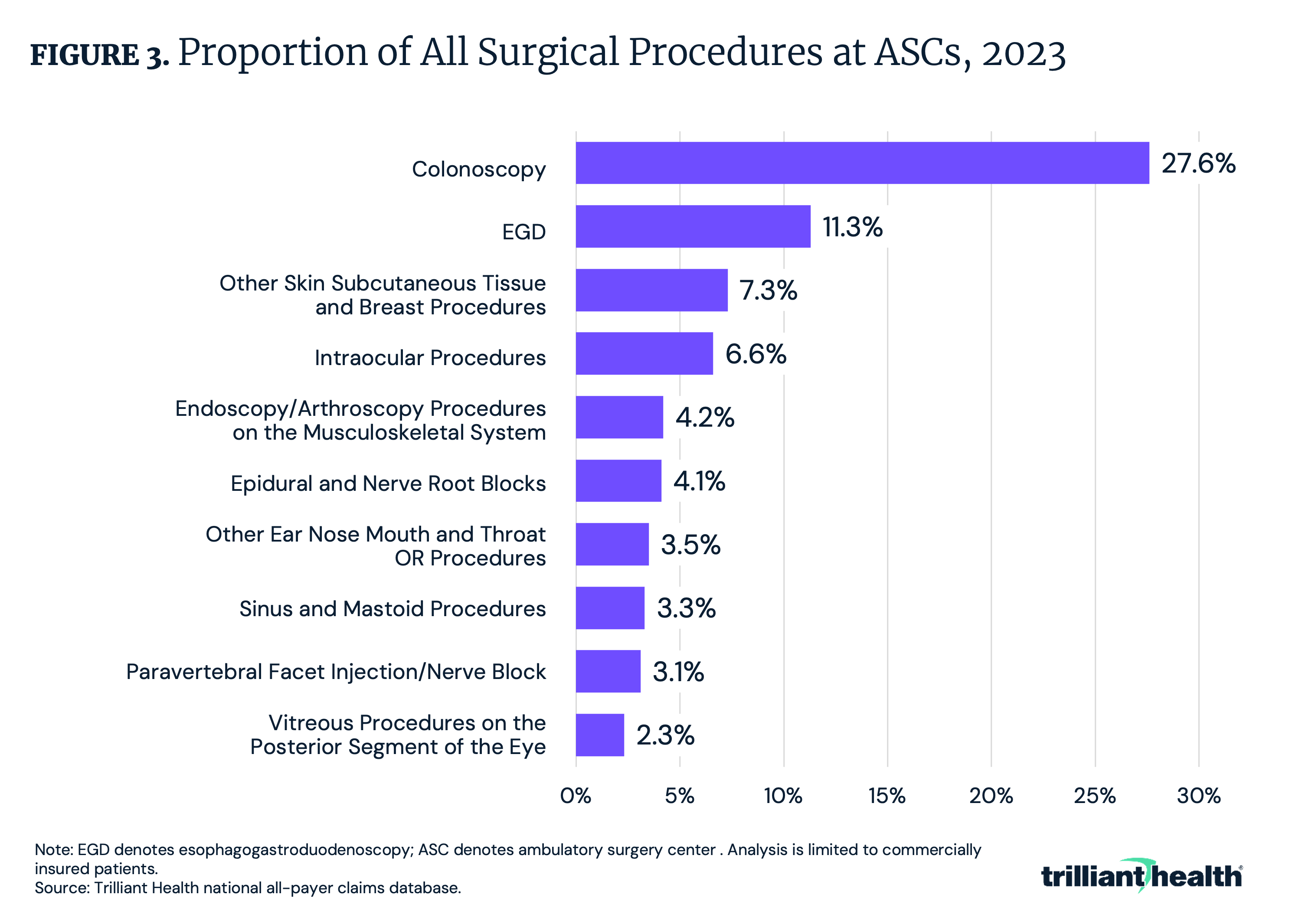

The Most Common Procedures Rendered at ASCs

With more surgical procedures migrating to ASCs and hospital outpatient departments (HOPDs), we examined the highest volume procedures rendered at ASCs in 2023. Colonoscopy represents the largest share of procedures performed at ASCs, accounting for 27.6% of total ASC surgical volume (Figure 3). The next most common procedures were esophagogastroduodenoscopy (EGD) (11.3%) and intraocular procedures (6.6%). Minimally invasive surgical procedures, particularly those related to diagnostic or preventive care, are driving the shift to outpatient facilities.

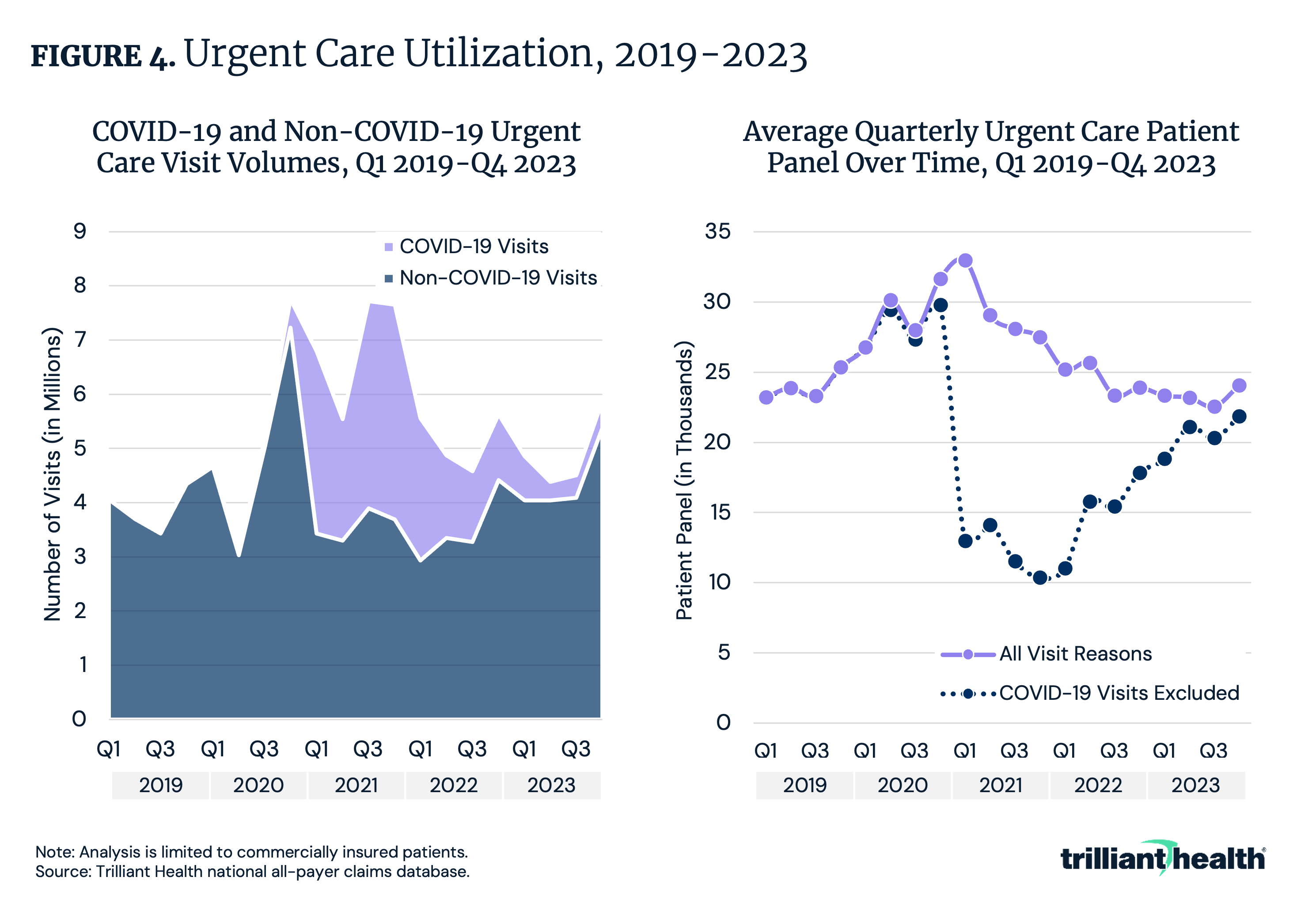

Urgent Care Growth Is No Longer COVID-Dependent

Once considered a “disruptor” in redirecting low-acuity and non-emergent care, urgent care facilities have evolved and matured to the point where many consider urgent care to be a “traditional” provider setting. Between Q1 2019 and Q4 2023, urgent care volumes increased by 44.6% in aggregate and 32.5% with COVID-19 related visits removed (Figure 3). While average quarterly patient panels at U.S. urgent care centers for all visit reasons spiked in Q4 2020, they declined over the following quarters.

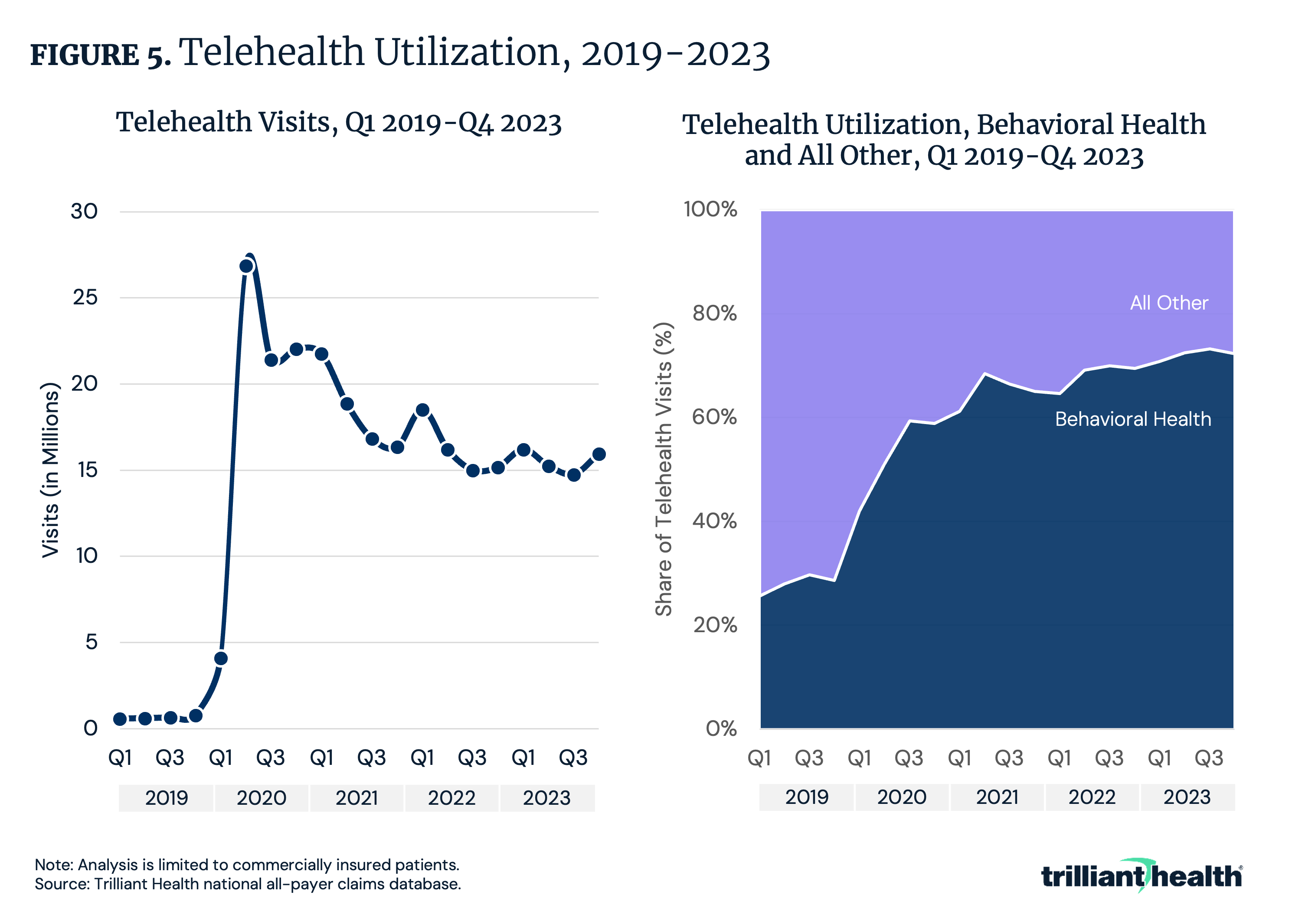

Behavioral Health Remains the Most Frequent Application of Virtual Care

The substantial increase in telehealth utilization at the pandemic’s onset in 2020 catalyzed a rapid expansion of telehealth capacity throughout the health economy, but without evidence of future demand or an understanding of the patient preferences of likely telehealth customers. Telehealth for the treatment and management of behavioral health conditions has increased consistently since 2019, a trend not seen in any other clinical application of virtual care. Compared to Q1 2020, the share of telehealth for behavioral health reasons increased from 42.0% to 72.3% in Q4 2023 (Figure 4). Overall telehealth utilization declined by 40.5% in the same period. As behavioral health demand continues to grow, telehealth can serve to bridge the gap in supply, potentially offering more cost-effectiveness in terms of direct and indirect costs.

Conclusion

Lower-cost care settings are reshaping the healthcare landscape by improving access and offering more cost-effective alternatives to traditional inpatient care. The continued migration of procedures to outpatient and alternative settings will depend on several factors, such as innovation cycles driving treatment shifts and regulatory changes (e.g., implementation of site-neutral payment, removal of the IPO list). Likewise, many services traditionally delivered by healthcare providers will be replaced by pharmaceuticals.

While the migration of care to lower acuity settings will likely reduce costs and expand care access, stakeholders must ensure that outcomes are not compromised. What factors should be considered when deciding which services are most appropriate for lower-cost settings like urgent care or outpatient clinics? What barriers exist to expanding access to lower-cost care settings, and how can they be addressed? How can employers and health plans promote the use of lower-cost care settings?

Ultimately, achieving sustainable value will require integrating these lower-cost settings into a broader, cohesive system that prioritizes patient needs, optimizes financial and tactical resources and adapts to emerging complexities in care delivery.

Get the latest insights delivered to your inbox.

Related Research

Was this shared with you?

Subscribe for weekly insights.

Subscribe to receive weekly insights from Trilliant Health's Research Team

Interested in citing our research? Please follow this guide.