.png)

.png?width=171&height=239&name=2025%20Trends%20Report%20Nav%20(1).png)

Study Takeaways

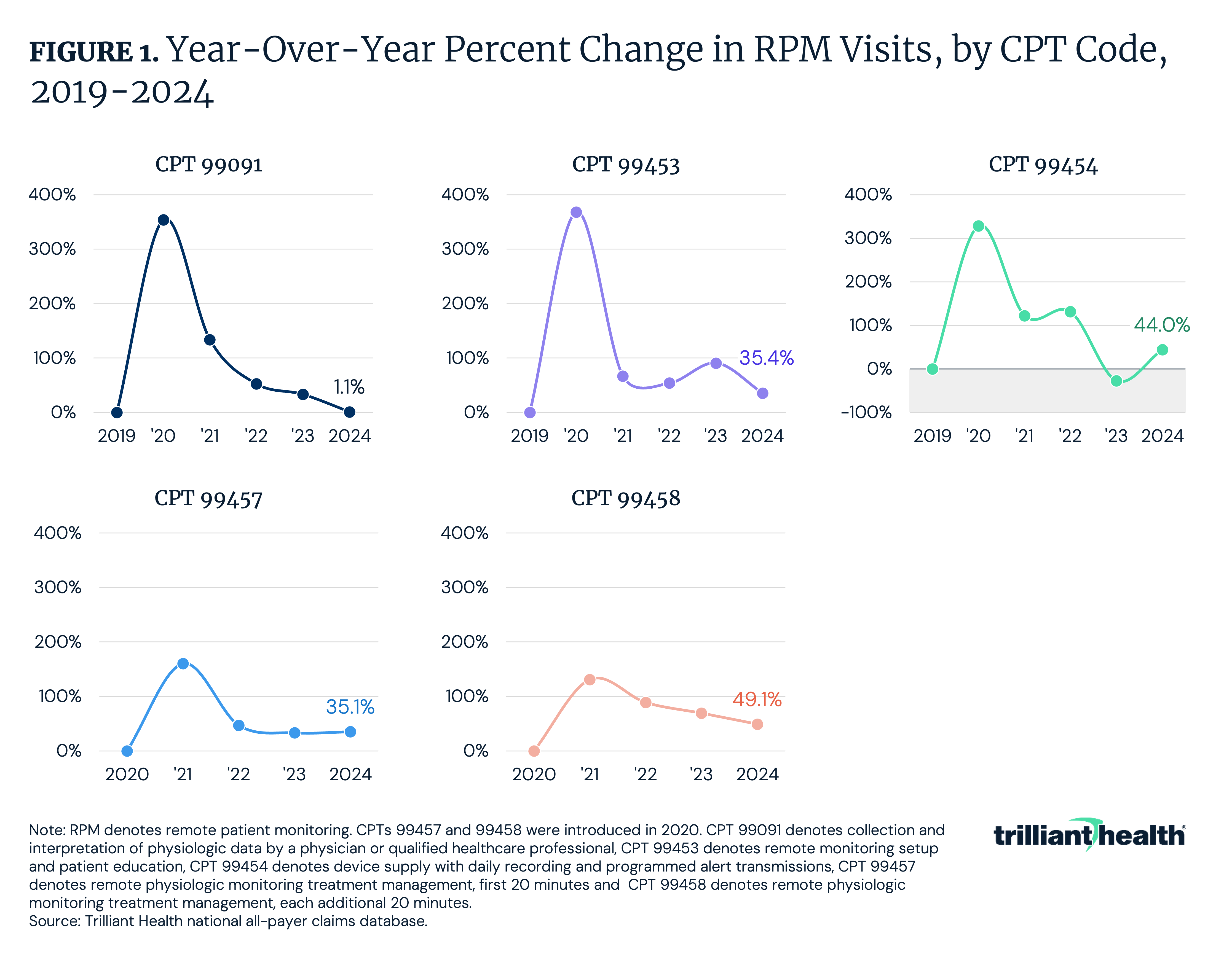

- Remote patient monitoring (RPM) utilization growth has decelerated in recent years. Among codes introduced prior to 2020 (CPTs 99091, 99453 and 99454), year-over-year growth averaged 350% among the three codes from 2019 to 2020 before slowing steadily through 2024.

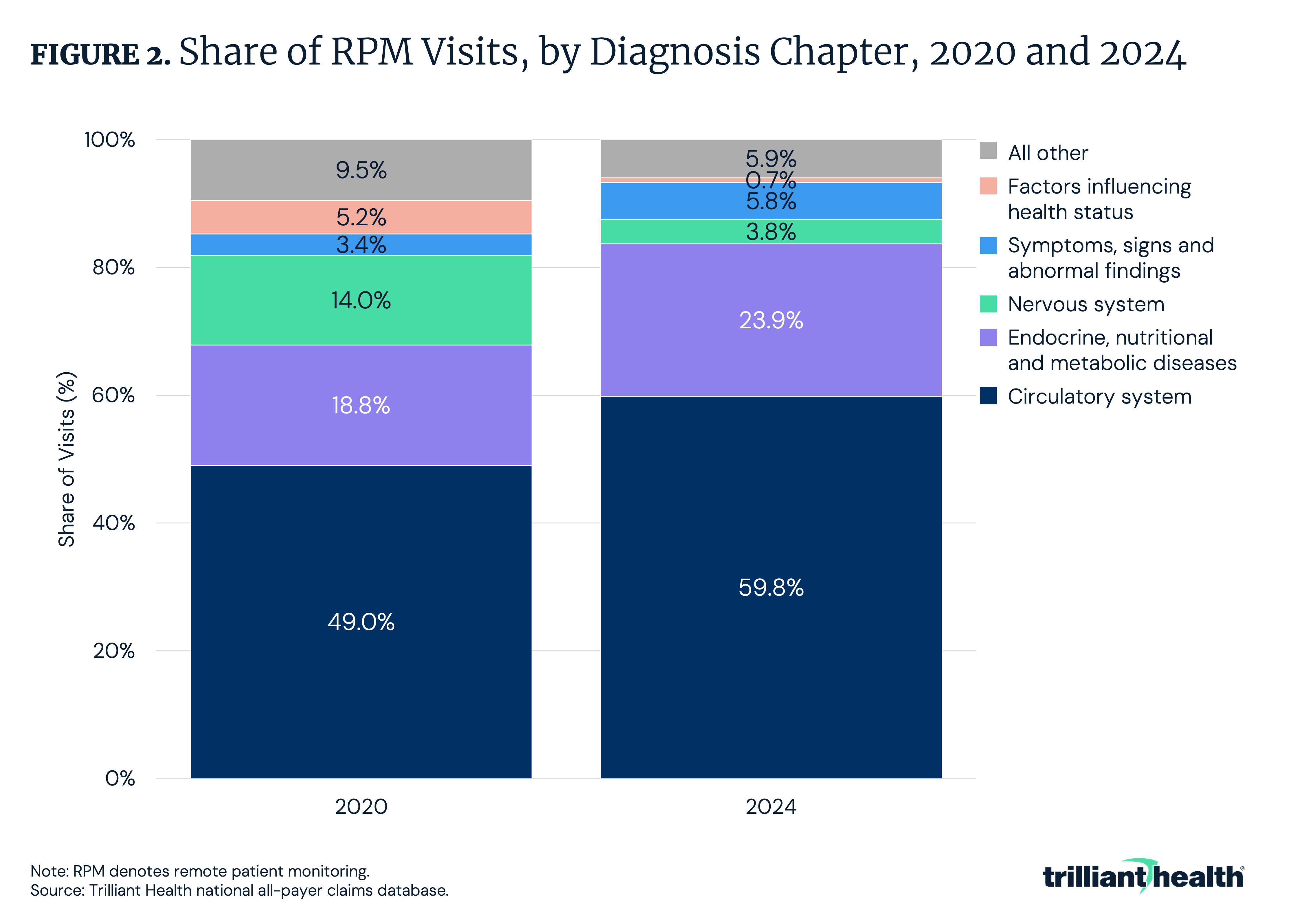

- RPM utilization has become increasingly concentrated in cardiovascular and metabolic conditions, with circulatory system diagnoses rising from 49.0% of visits in 2020 to 59.8% in 2024 and endocrine/metabolic conditions increasing from 18.8% to 23.9%, while all other diagnostic categories each represented less than 10% of visits in 2024.

Five years after Medicare established broad coverage for RPM, the technology is at an inflection point. Medicare spending on RPM grew from approximately $15M in 2019 to over $300M by 2022, coinciding with the formation of hundreds of digital health companies dependent on RPM reimbursement.1 However, evidence on RPM's clinical and cost effectiveness has been mixed, and utilization has remained concentrated among a small subset of patients and clinical applications. Commercial payers are beginning to respond, with UnitedHealthcare (UHC) announcing plans to restrict RPM coverage to heart failure and hypertensive disorders of pregnancy in 2026, a notable reversal relative to Medicare's continued coverage expansion.2 These developments reinforce the importance of examining how RPM has been applied in practice, the conditions it has addressed and how its utilization has evolved over time.

Background

RPM is defined as the automated collection of patient physiological measurements (e.g., blood pressure, blood glucose, weight and oxygen saturation) and their asynchronous transmission to healthcare providers for clinical review. RPM was originally designed on the premise that continuous or frequent asynchronous monitoring of patient-generated data between in-person clinical encounters would enable earlier intervention, improve chronic disease management and reduce the frequency of office visits.

Medicare began reimbursing RPM services in 2019 and, in 2020, finalized a rule affirming that RPM "may be medically necessary for patients with acute conditions as well as patients with chronic conditions," establishing a broad coverage framework.3 Subsequently, most commercial insurers followed suit, establishing similarly permissive coverage policies for RPM. The timing of this coverage expansion coincided with the COVID-19 pandemic-era acceleration of telehealth adoption, creating favorable market conditions for RPM operators, resulting in a 20x increase in Medicare spending on RPM over three years.

This rapid spending growth has led to regulatory scrutiny, with a 2024 Department of Health and Human Services Office of Inspector General (HHS OIG) report identifying billing patterns considered potentially problematic and raising concerns about the clinical necessity and benefit of certain RPM services, noting high-volume billing without clear evidence of meaningful patient engagement or clinical follow-up.4 Notably, HHS OIG reported approximately 1M Medicare beneficiaries received RPM in 2024. Despite these findings, Medicare finalized 2026 payment updates that expand RPM reimbursement by allowing providers to bill when patients transmit data for as few as 16 days per month and to receive separate payment for supplying monitoring devices even when clinician communication is minimal.5 In contrast, commercial reimbursement for RPM and digital health programs could tighten as payers apply more rigorous criteria for coverage, increasingly limiting expansion to use cases with clear and demonstrable clinical efficacy and return on investment. Providers have also expressed issues regarding RPM payment, with 65% reporting challenges related to RPM coding, billing and payment.6

Studies have shown meaningful clinical benefit in patients with heart failure and certain high-risk cardiovascular conditions, but evidence for other chronic conditions (e.g., hypertension and diabetes management) has been more inconsistent.7,8,9,10 Regarding the pending UHC RPM coverage reversal, researchers raised concerns related to the company's interpretation of cost-effectiveness research on RPM.11 While UHC's proposal to limit RPM coverage to heart failure and hypertensive disorders of pregnancy has been criticized and led to a delay in initiation, it is an example highlighting how payers may increasingly be orienting coverage toward condition-specific evidence requirements.

Analytic Approach

National all-payer claims were analyzed to examine the volume of RPM codes and the associated diagnoses/clinical reasons. Year-over-year visit volumes were examined for CPT codes 99091 (collection and interpretation of physiologic data by a physician or qualified healthcare professional), 99453 (remote monitoring setup and patient education), 99454 (device supply with daily recording and programmed alert transmissions), 99457 (remote physiologic monitoring treatment management, first 20 minutes) and 99458 (remote physiologic monitoring treatment management, each additional 20 minutes) from 2019 to 2024. Change in utilization over time was based on the year in which each code was introduced: CPTs 99457 and 99458 in 2020 and CPTs 99453, 99454 and 99091 in 2019, although CPT 99091 was introduced in 2002.

Findings

Across all RPM CPT codes, extreme growth in the first year after introduction was followed by more modest year-over-year increases. Among codes introduced prior to 2020 (99091, 99453 and 99454), year-over-year growth averaged 350% among the three codes from 2019 to 2020 before slowing steadily through 2024 (Figure 1). By 2024, growth had slowed to 1.1% for 99091, 35.4% for 99453 and 44.0% for 99454, although 99454 declined by 27.2% from 2022 to 2023. Among codes introduced in 2020 (99457 and 99458), initial year-over-year growth was 160.4% and 130.8%, respectively. Growth for both codes has since moderated, declining to 35.1% and 49.1% from 2023 to 2024, totaling approximately 2.3M visits among commercially insured patients in 2024.

The clinical reasons for RPM visits have remained fairly consistent over time, although the relative utilization has changed substantially. Diseases of the circulatory system accounted for the largest share of RPM visits in both 2020 and 2024, increasing from 49.0% to 59.8% over the period (Figure 2). Endocrine, nutritional and metabolic diseases, including diabetes, represented the second largest share, growing from 18.8% to 23.9%. The remaining diagnostic categories each accounted for less than 10% of visits in both years. Diseases of the nervous system declined from 14.0% to 3.8%, and factors influencing health status declined from 5.2% to 0.7%, while symptoms and abnormal clinical findings increased modestly from 3.4% to 5.8%.

Conclusion

The five-year trajectory of RPM reflects the predictable progression of a reimbursement-enabled innovation amid a favorable regulatory environment. Following Medicare’s broad coverage framework in 2019 and subsequent alignment by many commercial payers, RPM utilization increased, with some codes reaching 350% in year-over-year growth. By 2024, growth had slowed substantially and become concentrated in cardiovascular and metabolic conditions rather than diffusing across a wide range of clinical categories.

This pattern is consistent with broader healthcare "innovation" adoption patterns. Technologies that experience rapid uptake following reimbursement expansion often enter a stabilization phase in which volumes plateau and utilization concentrates in one or a few clinical applications. Telehealth followed a similar trajectory after the COVID-19 peak, with sustained utilization largely concentrated in behavioral health.12 RPM is undergoing a comparable maturation process, with cardiovascular conditions representing the most durable use case.

Employers, insurers and public programs face increasing fiscal pressure, and clinical interventions without strong and conclusive evidence of value will be subject to heightened review. Digital health solutions that expanded under permissive pandemic-era coverage environments may encounter greater scrutiny regarding return on investment and clinical impact. Where evidence remains mixed or inconclusive, coverage may narrow rather than expand. RPM, and digital health more broadly, raises a more fundamental question about the role of technology in care delivery. Most digital health solutions that benefited from pandemic-era expansion were already available, rather than newly entering the market to address a gap in care or inefficiency. These solutions can create additional touchpoints, monitoring or administrative complexity within existing workflows without materially changing outcomes. This scenario of growing utilization without corresponding improvements in outcomes or reductions in avoidable spending is the definition of low-value care. Over time, solutions that cannot demonstrate incremental added value will inevitably face utilization management restrictions or exclusion from coverage arrangements altogether.

Capital market activity mirrors these observations, with digital health investments, including companies reliant on RPM reimbursement, decreasing significantly from pandemic-era levels. Simultaneously, the broader ecosystem of consumer-generated health data is facing additional scrutiny. Personal health tracking devices, including wearable technologies that report physiologic measurements, have raised questions regarding accuracy and clinical reliability. Many of these products are not regulated as medical-grade diagnostic devices, yet their data may inform clinical workflows or patient expectations regarding remote monitoring. Under the framework of the U.S. Food and Drug Administration (FDA), many wearable or app-based technologies operate under general wellness provisions and are not held to the same evidentiary standards as cleared medical devices. As payers and regulators place greater emphasis on evidence standards, distinctions between consumer wellness tools and validated medical technologies may become increasingly relevant.

Research suggests that consumer sentiment toward RPM is generally, if not universally, favorable, as adherence and engagement varies meaningfully by clinical condition and digital literacy.13 Privacy concerns, data security risks, technology errors and the potential for added burden or reduced human interaction are reported concerns with RPM. Monitoring may feel additive, layering additional tasks onto existing care without a clear perceived benefit.

Without stronger evidence of clinical and cost effectiveness beyond cardiovascular applications, broader commercial coverage expansion is unlikely. As spending growth and value scrutiny intensify, RPM will be assessed on measurable clinical outcomes and cost savings, rather than technological potential.

Get the latest insights delivered to your inbox.

Was this shared with you?

Subscribe for weekly insights.

Subscribe to receive weekly insights from Trilliant Health's Research Team

Interested in citing our research? Please follow this guide.