.png)

.png?width=171&height=239&name=2025%20Trends%20Report%20Nav%20(1).png)

Study Takeaways

- From 2018 to 2021, prior to the approval of Wegovy® in June 2021, patient volume for anti-obesity therapies increased by 16.4%, compared to 94.5% from 2021 to 2024.

- Among women ages 18-44, non-GLP/GIP therapies accounted for 96.1% of prescriptions in 2018, but declined to 37.3% by 2024 as GLP-1 and GIP/GLP-1 therapies accounted for the majority of treatment.

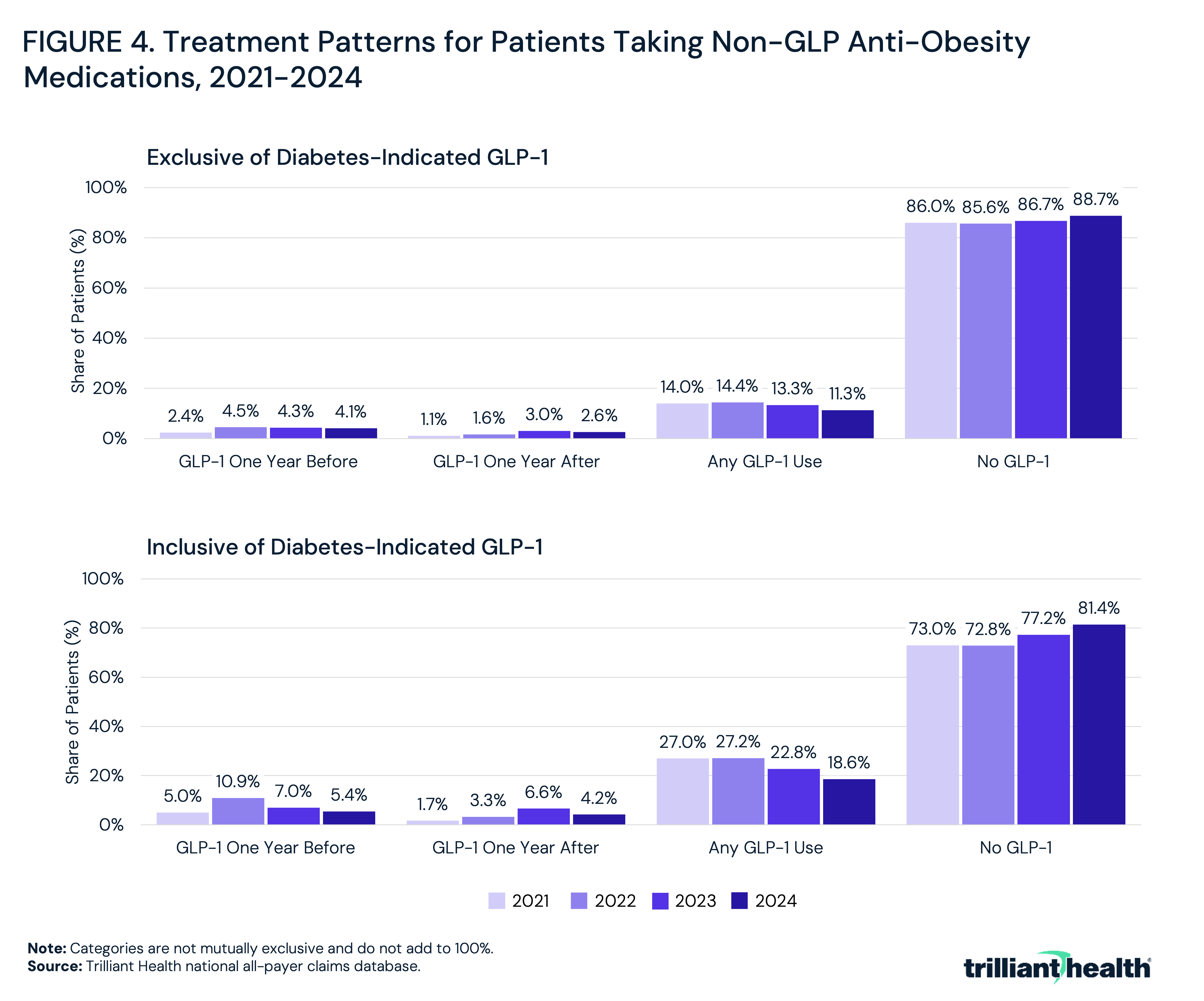

- Despite GLP-1 growth, the majority of patients on non-GLP anti-obesity medications had no observed GLP-1 use for weight loss within the same year, suggesting these populations remain largely distinct.

The meteoric rise of GLP-1 therapies over the past five years makes it easy to forget that anti-obesity medications have been available for decades. Earlier pharmacologic options, including naltrexone-bupropion and phentermine-topiramate, are associated with moderate weight loss and are relatively well tolerated. However, compared to the eligible patient population, adoption has been somewhat limited. As GLP-1 medications have become a cultural phenomenon and gained associated market share, the role of legacy non-GLP anti-obesity drugs has become less clear. While some prescribing may be shifting toward GLP-1 therapies, cost, coverage restrictions and contraindications would support continued utilization of non-GLP anti-obesity medications in certain patient populations. Examining trends across these drug classes provides insight into how the proliferation of GLP-1 therapies is influencing, and potentially replacing, treatment patterns for legacy obesity products and changing the approach to weight management writ large.

Background

Approximately 40% of U.S. adults are considered obese.1 Several prescription medications for chronic weight management were approved by the U.S. Food and Drug Administration (FDA) during the 2010s, including naltrexone-bupropion, sold under the brand name CONTRAVE®. In clinical trials, these oral therapies result in weight loss of approximately 5% to 10% of baseline body weight when combined with lifestyle interventions.2

Despite availability, insurance coverage for anti-obesity medications has historically been inconsistent, particularly among commercial plans and in Medicare, which does not include Part D coverage of weight loss drugs for obesity. However, CMS announced a GLP-1 coverage demonstration starting July 2026.3 Additionally, like almost all pharmaceutical therapies, medications such as CONTRAVE® have contraindications (e.g., uncontrolled hypertension, seizure disorders, opioid dependence) that can limit use in certain patient populations. As a result, first-line treatment for obesity management has historically continued to focus on lifestyle modification and bariatric surgery for eligible patients as opposed to pharmacologic treatment.

The approvals of GLP-1 receptor agonists for obesity and weight management in recent years represent a significant change in the clinical standards for obesity treatment. Initially developed for type 2 diabetes, this drug class has demonstrated significant weight-loss effects through mechanisms including appetite suppression and delayed gastric emptying. Clinical trials of newer GLP-1 therapies for obesity have reported substantially larger average reductions in body weight than those observed with earlier drug classes (e.g., naltrexone-bupropion). There has been rapid growth in prescribing of GLP-1 medications for weight management, with high rates of off-label prescribing of diabetes-indicated GLP-1s for weight loss. Coverage of GLP-1s for weight loss under employer-sponsor plans is variable, with just 19% of large employers reporting offering coverage of GLP-1 therapies indicated for weight loss in 2025.4 For patients willing to pay out-of-pocket, list prices of GLP-1s average around $1,000, although direct-to-consumer (DTC) platforms offer self-pay monthly rates ranging from $300 to $500 per month. Notably, total U.S. spending on GLP-1 therapies increased by more than 500% from 2018 to 2023, from $13.7B to $71.7B.5 While the initial costs have decreased substantially in recent years, limited insurance coverage and high monthly costs continue to be cited as barriers to accessing GLP-1 therapies.

Given the high demand for GLP-1 medications and cultural norms favoring a "pharmaceutical first" approach to weight loss management, this study examines trends in anti-obesity prescribing, both for GLP-1 therapies and legacy anti-obesity medications.

Analytic Approach

Patient-level prescriptions for non-GLP anti-obesity drugs – diethylpropion, naltrexone-bupropion (i.e., CONTRAVE®), orlistat, phendimetrazine, phentermine, phentermine-topiramate – and GLP-1 drugs – semaglutide, liraglutide, tirzepatide – indicated for weight loss were examined between 2018 and 2024. For GLP-1 and GIP/GLP-1 therapies, brand names are used to distinguish indication (obesity management vs. type 2 diabetes), whereas non-GLP obesity therapies are reported by generic drug name. Given known trends in off-label prescribing, GLP-1 drugs indicated for type 2 diabetes (e.g., Ozempic®) were also examined. Among patients prescribed a non-GLP weight loss drug, prescriptions one year before or after for GLP-1 weight loss drugs were also examined.

Findings

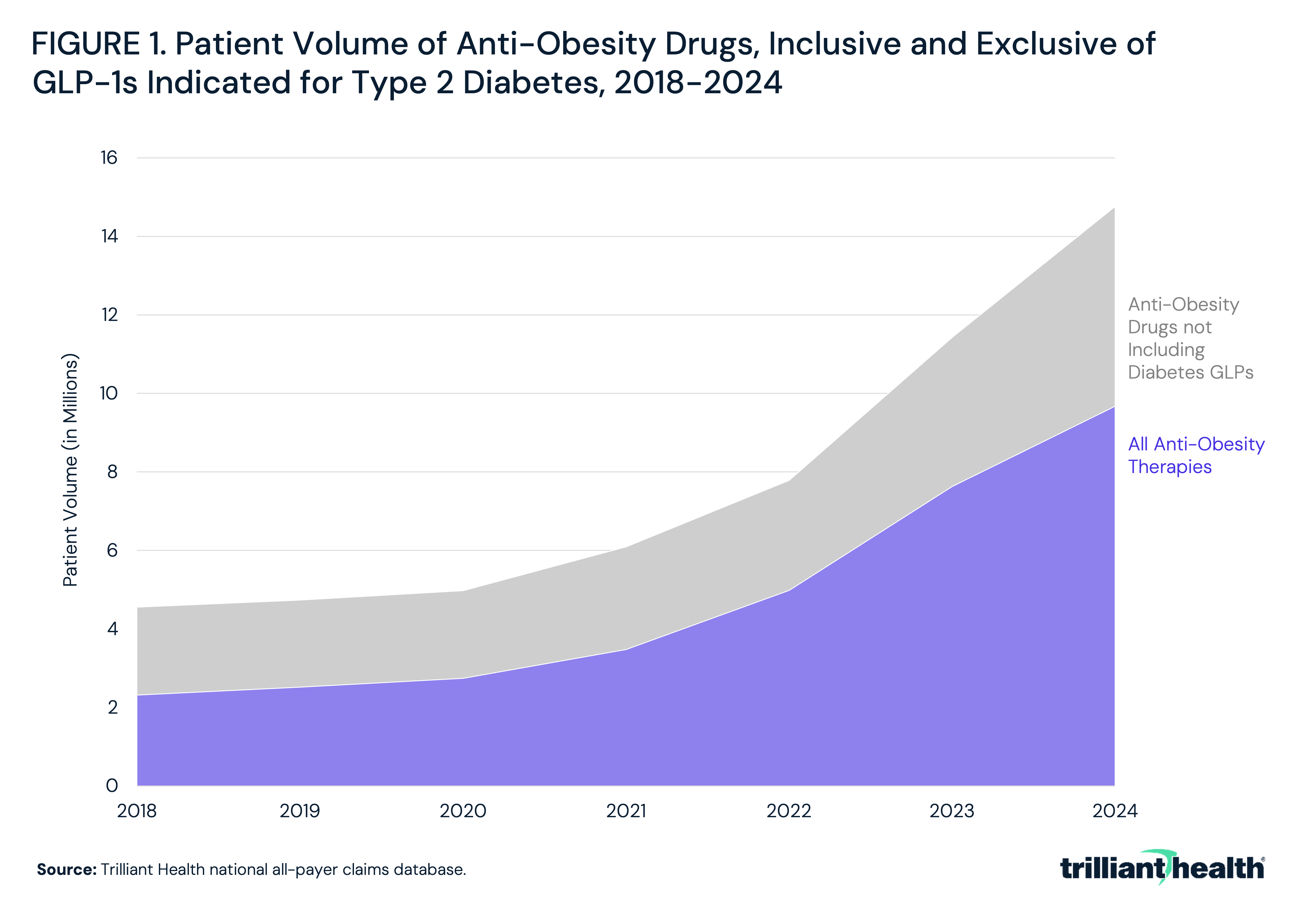

From 2018 to 2021, patient volume for anti-obesity therapies increased by 16.4%, compared to 94.5% from 2021 to 2024, following the approvals of Wegovy® in June 2021 and Zepbound® in November 2023 (Figure 1). Total patient volume inclusive of GLP-1 therapies indicated for type 2 diabetes – which are often prescribed off-label for weight loss – increased by 50.4% from 2018 to 2021 and 178.0% from 2021 to 2024. From 2021 to 2024, percent growth inclusive of GLP-1 therapies indicated for type 2 diabetes was approximately 1.9x higher than growth excluding these therapies.

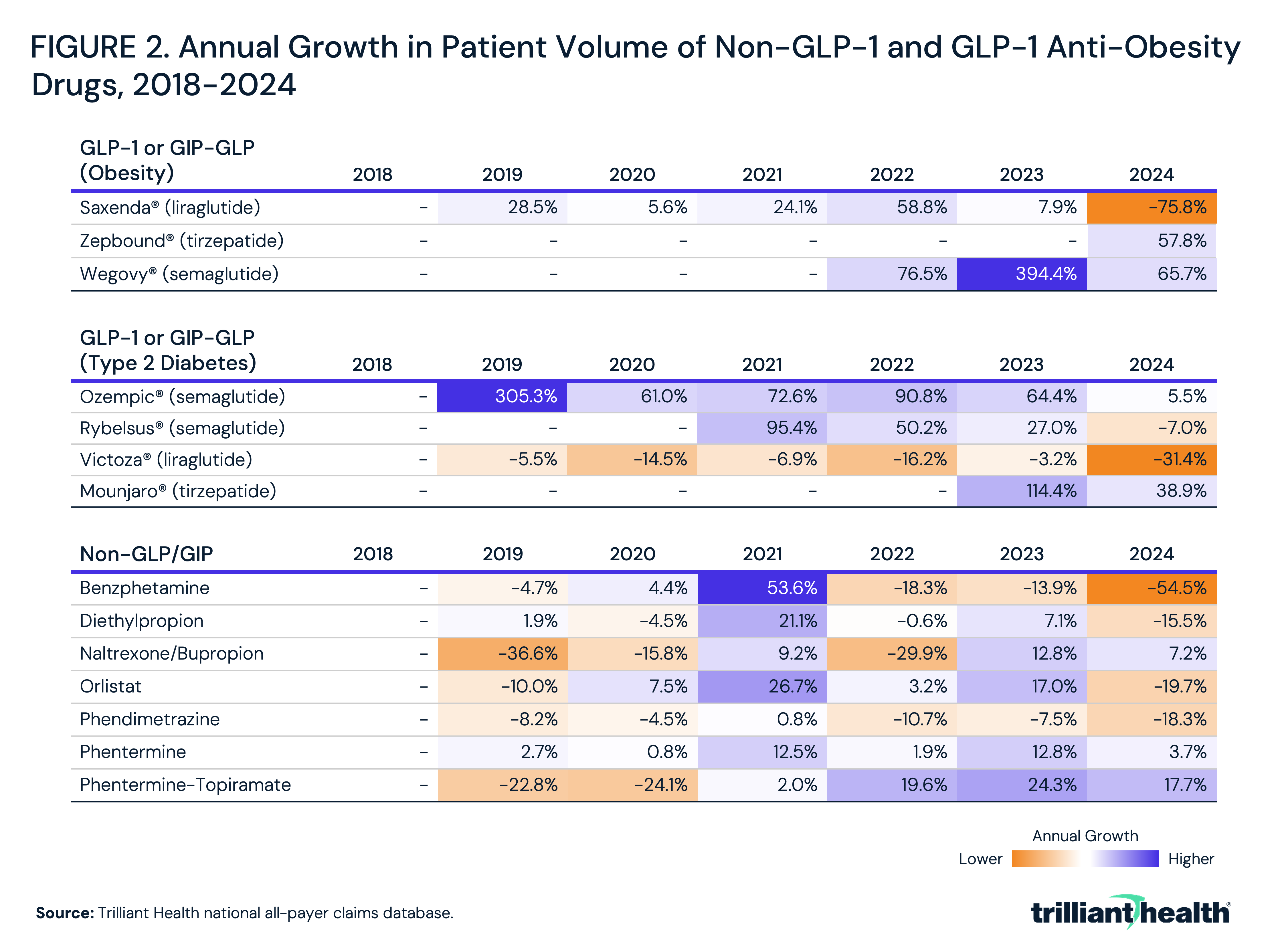

Annual growth in patient volume varied substantially across anti-obesity drugs from 2018 to 2024. Among non-GLP-1 therapies, several exhibited inconsistent or negative growth, with benzphetamine, diethylpropion and phendimetrazine declining from 2023 to 2024 (-54.5%, -15.5% and -18.3%, respectively) (Figure 2). Orlistat also declined in 2024 (-19.7%) following prior growth, while naltrexone/bupropion increased by 7.2%. Phentermine maintained relatively stable growth, ranging from 0.8% to 12.8% annually, and phentermine-topiramate had more consistent acceleration in recent years, increasing 17.7% in 2024.

In contrast, GLP-1 and GIP/GLP-1 therapies demonstrated consistently higher growth rates, though trends varied by product and indication. Semaglutide products showed rapid growth, with Ozempic® increasing 305.3% in 2019 and maintaining strong growth through 2023 (64.4%) before moderating to 5.5% in 2024, while Wegovy® grew 394.4% in 2023 and remained elevated at 65.7% in 2024. Following approval in 2023, Zepbound® increased by 57.8% in 2024. Oral semaglutide (Rybelsus®) also grew, though growth turned slightly negative in 2024 (-7.0%). Tirzepatide (Mounjaro®) demonstrated continued uptake following its approval, increasing 114.4% from 2022 to 2023 and 38.9% from 2023 to 2024. Earlier GLP-1 therapies had different trends, with Victoza® (type 2 diabetes) declining across most years, including a 31.4% decrease in 2024, while Saxenda® (obesity) declined by 75.8% in 2024 after modest growth in prior years.

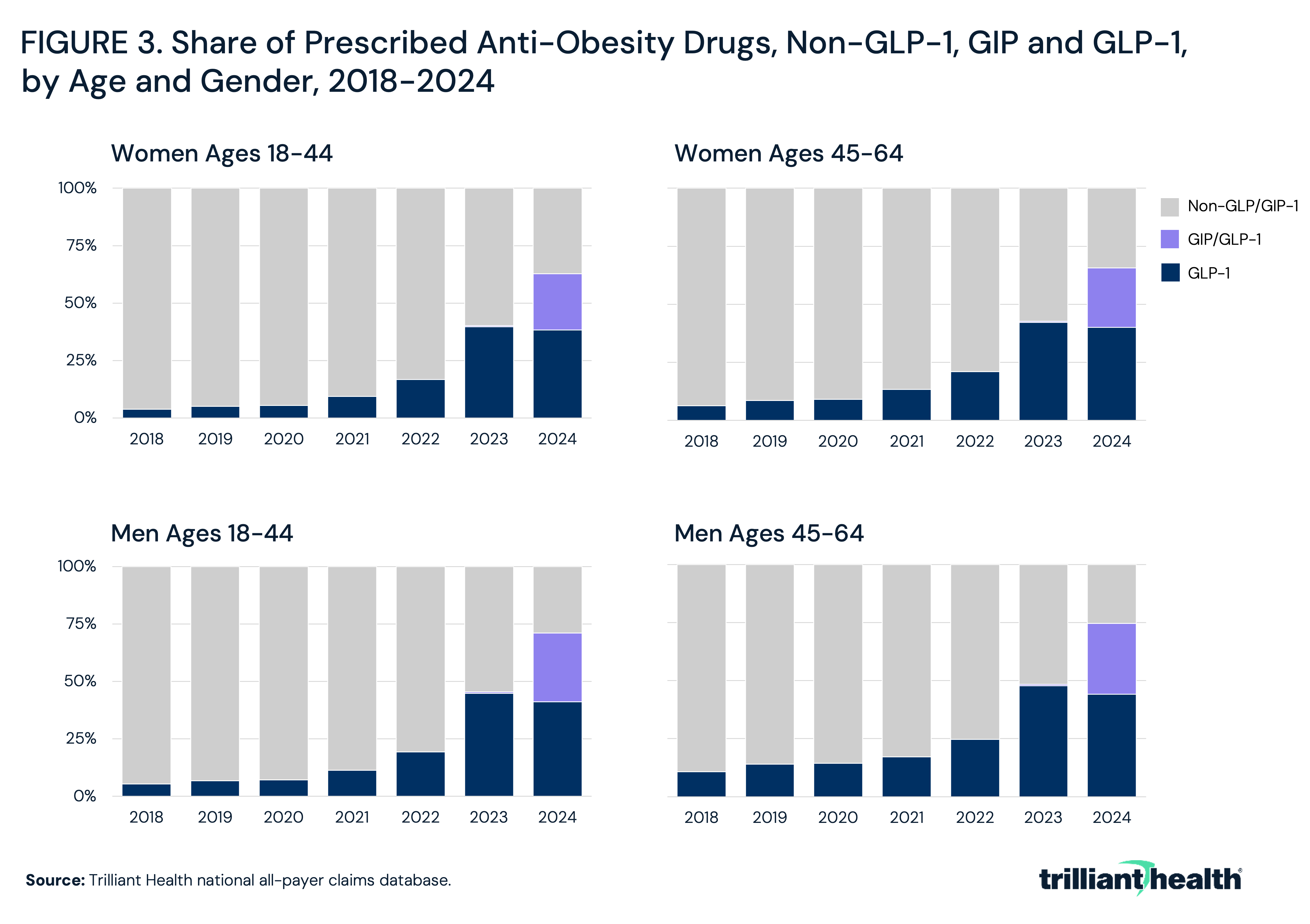

When limited to GLP-1 and GIP/GLP-1 therapies indicated for obesity, the share of prescribed anti-obesity drugs shifted markedly across age and gender cohorts between 2018 and 2024. In 2018, non-GLP/GIP therapies accounted for the majority of prescriptions across all groups, ranging from 89.3% among men ages 45-64 to 96.1% among women ages 18-44, while GLP-1 shares remained below 10.8% in all cohorts (Figure 3). By 2021, GLP-1 uptake increased modestly but remained a minority share, reaching 9.4% among women ages 18-44 and 13.4% among women ages 45-64, with somewhat higher shares among men (11.3% and 17.1%, respectively). More rapid adoption began in 2022, with GLP-1 shares increasing to 16.8%–21.0% among women and 19.3%–24.7% among men.

Adoption accelerated further in 2023, with GLP-1 therapies reaching 39.7%–47.7% of prescriptions across cohorts, though non-GLP/GIP therapies still accounted for a slight majority in all groups. By 2024, the composition of prescribing shifted substantially with the emergence of GIP/GLP-1 (i.e., Zepbound®) therapies, which accounted for 24.5%–30.5% of prescriptions across cohorts. When combined, GLP-1 and GIP/GLP-1 therapies represented the majority of anti-obesity prescriptions in all groups, ranging from 62.7% among women ages 18-44 to 74.6% among men ages 45-64. In contrast to prior years, GLP-1–only therapies accounted for a smaller share – 38.3%-44.1%. Over the same period, the share of non-GLP/GIP therapies declined substantially, though it remained highest among women ages 18-44 (37.3%) and lowest among men ages 45-64 (25.4%).

Notably, these distributions differ materially compared to analyses that include GLP-1 therapies indicated for type 2 diabetes, which are often prescribed off-label for weight loss. When GLP-1/GIP medications indicated for type 2 diabetes are included in the analysis, they increase from 37.8% of prescription volume in 2018 to 86.9% of total prescription volume by 2024.

Among patients taking non-GLP anti-obesity medications between 2021 and 2024, the majority had no observed GLP-1 use within one year, both inclusive and exclusive of GLP-1 therapies approved for type 2 diabetes. For weight loss GLP-1 therapies, the “No GLP-1” category ranged from 86.0% in 2021 to 88.7% in 2024 (Figure 4). The “Any GLP-1 Use” category declined from 14.0% to 11.3% over the period, while the “GLP-1 One Year After” category increased from 1.1% to 3.0% by 2023 before decreasing to 2.6% in 2024. The “GLP-1 One Year Before” category increased from 2.4% to 4.5% in 2022. When GLP-1s indicated for type 2 diabetes were included in the analysis, the “No GLP-1” share was lower but remained the largest category, ranging from 73.0% in 2021 to 81.4% in 2024. In this specification, the “Any GLP-1 Use” category declined from 27.0% to 18.6%, while both “GLP-1 One Year After” and “GLP-1 One Year Before” increased through 2022 (3.3% and 10.9%, respectively) before decreasing to 4.2% and 5.4% in 2024.

Conclusion

The data reveal a meaningful increase in utilization and prescribing share of GLP-1 therapies alongside continued but reduced utilization of non-GLP anti-obesity medications. From 2018 to 2021, prior to the approval of Wegovy® in June 2021, patient volume for anti-obesity therapies increased by 16.4%, compared to 94.5% from 2021 to 2024. Notably, most patients receiving non-GLP therapies had no observed GLP-1 use within the same year, including diabetes-indicated GLP-1s. These patterns reflect concurrent and differentiated use of both drug classes within the market, with GLP-1 therapies accounting for a growing share of overall prescribing and non-GLP therapies representing a smaller portion of treatment. Additionally, the results suggest that patients newly starting an anti-obesity medication are overwhelmingly starting with GLP-1s, rather than legacy non-GLP products.

The observed increase in uptake of GLP-1 medications relative to legacy anti-obesity therapies likely reflects differences in prescribing behaviors and standards, clinical efficacy and patient and provider awareness despite the decades-long availability of some earlier pharmacologic options. Likely, DTC prescribing infrastructure has become a demand driver for GLP-1 therapies, particularly following the commercialization of Ozempic®. Telehealth-enabled platforms and vertically integrated weight management companies have contributed to increased visibility and availability of pharmacologic weight management.

A primary and persistent concern with the use of anti-obesity medications is the cost-effectiveness across available treatment modalities. GLP-1 therapies have demonstrated substantially greater average weight reduction than legacy non-GLP agents in clinical trials, but have significantly higher lifetime costs – relative to both older pharmacologic options and, in some cases, bariatric surgery.6,7 However, many clinicians who have historically prescribed legacy anti-obesity medications may continue to default to these medications in the absence of clear formulary access for GLP-1s or sufficient time and infrastructure to navigate prior authorization requirements that payers may have.

Differences in treatment duration can also influence whether non-GLP obesity medications can be “replaced” by GLP-1 therapies. Many legacy non-GLP anti-obesity medications, such as phentermine or combination therapies like naltrexone-bupropion, are often prescribed in shorter, episodic courses (e.g., 12 weeks), but other non-GLP weight loss drugs like CONTRAVE® are indicated for chronic weight management. Additionally, while not typically classified as addictive in the traditional sense, some, particularly centrally acting agents like phentermine, carry risks related to misuse or psychological dependence. Understanding how patient preferences and perceptions interact with provider recommendations and formulary availability is critical in projecting future demand for these therapies.

In contrast, GLP-1 therapies are designed as chronic treatments for a chronic disease, meaning they function as ongoing management rather than a curative intervention. As such, clinical benefit is contingent on sustained adherence over time, with evidence indicating that discontinuation is frequently associated with weight regain. This fundamental difference implies that GLP-1 adoption is not simply a substitution effect, but a structural shift toward long-duration pharmacologic management of obesity.

Health insurance brokers are increasingly advising employers on whether to separate (“carve out”) pharmacy and medical benefits to more directly manage utilization and financial exposure to GLP-1 therapies. For payers and self-funded employers, the long-term return on investment for GLP-1 coverage depends not only on the magnitude of weight loss achieved but on downstream reductions in obesity-related comorbidities, healthcare utilization and productivity costs.8,9,10,11 Bariatric surgery is associated with higher upfront costs but has demonstrated durable long-term outcomes. A rigorous cost-effectiveness framework that accounts for adherence rates, treatment duration and long-term clinical outcomes across all three modalities – non-GLP pharmacotherapy, GLP-1 therapy and surgical intervention – is necessary to inform both benefit design decisions. Moreover, the variation in workforce demographics and health status necessitates population-specific cost-effectiveness assessments, such as stratifying by age, baseline comorbidity burden and expected treatment adherence, to inform benefit design decisions.

At the same time, the growing evidence of GLP-1 therapies' broader cardiometabolic benefits, including demonstrated reductions in cardiovascular events independent of weight loss, may increasingly shift prescribing behavior towards GLP-1s. Patient perception is a crucial variable, particularly given the cultural visibility of GLP-1 medications driven by DTC advertising and media coverage. This has created patient demand patterns that independently influence prescribing, as patients who are aware of and actively seeking GLP-1 therapies may perceive non-GLP anti-obesity options as clinically inferior.

While cost and insurance coverage remain commonly cited as barriers to GLP-1 therapy utilization, the logic driving patient decision-making is different from coverage limitations. The introduction of lower-cost alternatives, including generic formulations of liraglutide following the loss of exclusivity for Saxenda® in 2025, may modestly improve affordability within the GLP-1 class. However, utilization of liraglutide is historically lower than other GLP-1 therapies (i.e., semaglutide and tirzepatide).

Affordability, particularly in healthcare, is perennially a political issue that can mask a larger societal issue. While many patients may express the sentiment that, “If my employer covered it, I would take it,” there is a separate matter of personal accountability. Patients who perceive these therapies as life-changing often weigh the cost against other discretionary expenses. For patients motivated by health outcomes – or in many instances personal aesthetics – and where monthly prices are not cost-prohibitive, there is a greater willingness to invest in these therapies, even in the absence of insurance coverage. Said differently, the barrier is not always “I can’t afford it,” but rather “I am unwilling to allocate personal resources,” highlighting the interplay between cost perception influencing real-world adoption.

Presently, the cost/benefit analysis of GLP-1 therapies is indeterminate, calling into question whether GLP-1 therapies will continue to be the dominant approach to medication-led weight loss. Clinical evidence indicating that weight regain following GLP-1 discontinuation is common implies that effective obesity management may require indefinite pharmacologic treatment, which has implications for lifetime cost and adherence. Payers evaluating the long-term financial impact of GLP-1 coverage, providers counseling patients on treatment initiation and health systems planning for chronic disease management infrastructure must all account for the reality that current GLP-1 prescribing may be predicated on indefinite use. Additionally, real-world adherence rates and long-term safety data are still being understood.

Get the latest insights delivered to your inbox.

Was this shared with you?

Subscribe for weekly insights.

Subscribe to receive weekly insights from Trilliant Health's Research Team

Interested in citing our research? Please follow this guide.