.png)

.png?width=171&height=239&name=2025%20Trends%20Report%20Nav%20(1).png)

.png)

Service Line Intelligence

2026Behavioral Health Report

Katie PattonClara PetrucelliMaggie JacksonAustin MillerAllison Oakes, Ph.D.

Applying an Economic Framework to Study Behavioral Health Trends

For decades, the U.S. health economy has operated as if the fundamental rules of economics — demand, supply and yield — do not apply. However, the U.S. healthcare system is what game theorists call a “negative-sum game,” and the rules of that game are immutable. This reality impacts every health economy stakeholder.

.png)

Demand

Primary Data Source: National All-Payer Claims Dataset

.png)

Supply

Refers to the various providers of health services ranging from hospitals and physician practices to retail pharmacies, new entrants and virtual care platforms.

Primary Data Source: Provider Directory

%20(1).png)

Yield

Refers to the intersection of demand and supply (i.e., negotiated rate) and is also influenced by market factors such as policy regulations and reimbursement incentives.

Primary Data Source: Health Plan Price Transparency Dataset

.png)

Demand

The U.S. Behavioral Health Crisis Did Not Subside With the End of the Pandemic — It Was Further Amplified

23.4%

Adults with any mental illness in 2024

1-in-3

Young adults ages 18–25 with any mental illness in 2024

89.3%

Growth in utilization related to anxiety disorders from 2018 to 2024

65.6%

Proportion of telehealth volume attributed to behavioral health in 2024

What's in the Report

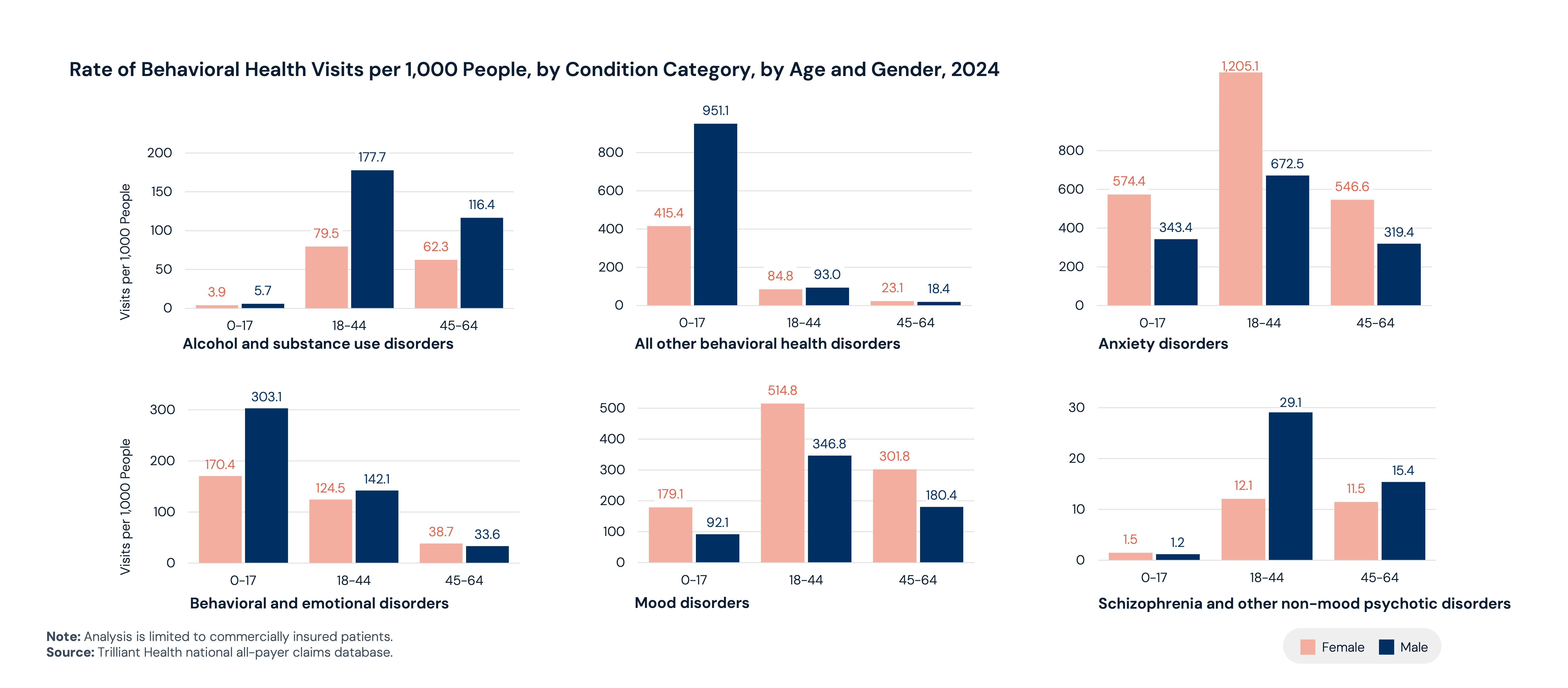

Increasing behavioral health prevalence is concentrated among young adults: Adults ages 18–25 continue to exhibit the highest prevalence of any mental illness (33.2%) and serious mental illness (15.9%), though rates have declined since 2021. As of 2024, anxiety disorders among women ages 18-44 represents the highest behavioral health utilization category (1,205.1 visits per 1,000 people). In contrast, adults ages 26–49 have experienced increases in nearly all mental health and substance use disorders (SUD), with the rate of any mental illness increasing by 1.2 PP and 0.9 PP for co-occurring any mental illness and SUD from 2021 to 2024.

Multiracial individuals demonstrate the most intense behavioral health need: Multiracial individuals have the highest prevalence across major behavioral health conditions, including any mental illness (35.5%), compared to 25.1% of White and 20.9% of Black individuals. Multiracial individuals also have the highest SUD prevalence (24.9%) compared to White (18.5%) and Black (18.3%) individuals.

Sharp increase in drug- and alcohol-induced deaths driven by adult men: Drug- and alcohol-related mortality is higher among men than women, ranging from 2.2x to 2.9x across age groups. Over the past two decades, the drug- and alcohol-induced mortality rate has increased substantially among men ages 18–44 (114.7%), 45–65 (106.9%) and 65–84 (118.7%). Among adolescents, males have the highest intentional self-harm mortality rate, increasing by 45.2% between 2004 and 2024.

Behavioral health accounts for the majority of telehealth use: Telehealth for the treatment and management of behavioral health conditions has emerged as a substitute for in-person care. Since 2018, the proportion of telehealth volume that is attributed to behavioral health has increased from 18.4% to 65.6%.

Stimulants show fastest growth among behavioral health medications: Between 2018 and 2024, the share of patients taking stimulants increased the most (53.3%), followed by antipsychotics (45.4%). However, anxiolytics represent the medication class with the highest overall patient volume.

.png)

Supply

The Behavioral Health Workforce Is Not Equipped to Meet Demand — and the Gap Is Widening

27.3%

National mental health professional adequacy rate in 2025

99,780

FTE shortfall projected in mental health counseling by 2038

34.3%

Share of behavioral health medications prescribed by allied health providers, exceeding PCPs and psychiatrists

83%

Behavioral health providers reporting burnout in 2023

What's in the Report

Over half of large metros have a psychiatrist shortage: Nationally, there are approximately 10,000 people per one psychiatrist. Across CBSAs with populations over 1M, 56.9% are in a shortage relative to this benchmark. For example, while San Francisco, CA has a relative surplus of 541 psychiatrists, Atlanta, GA has a deficit of 348 psychiatrists.

Mental health professional shortage areas span every U.S. state: The percent adequacy of mental health professionals is 27.3% as of 2025, ranging from 5.7% in West Virginia to 52.3% in New Jersey.

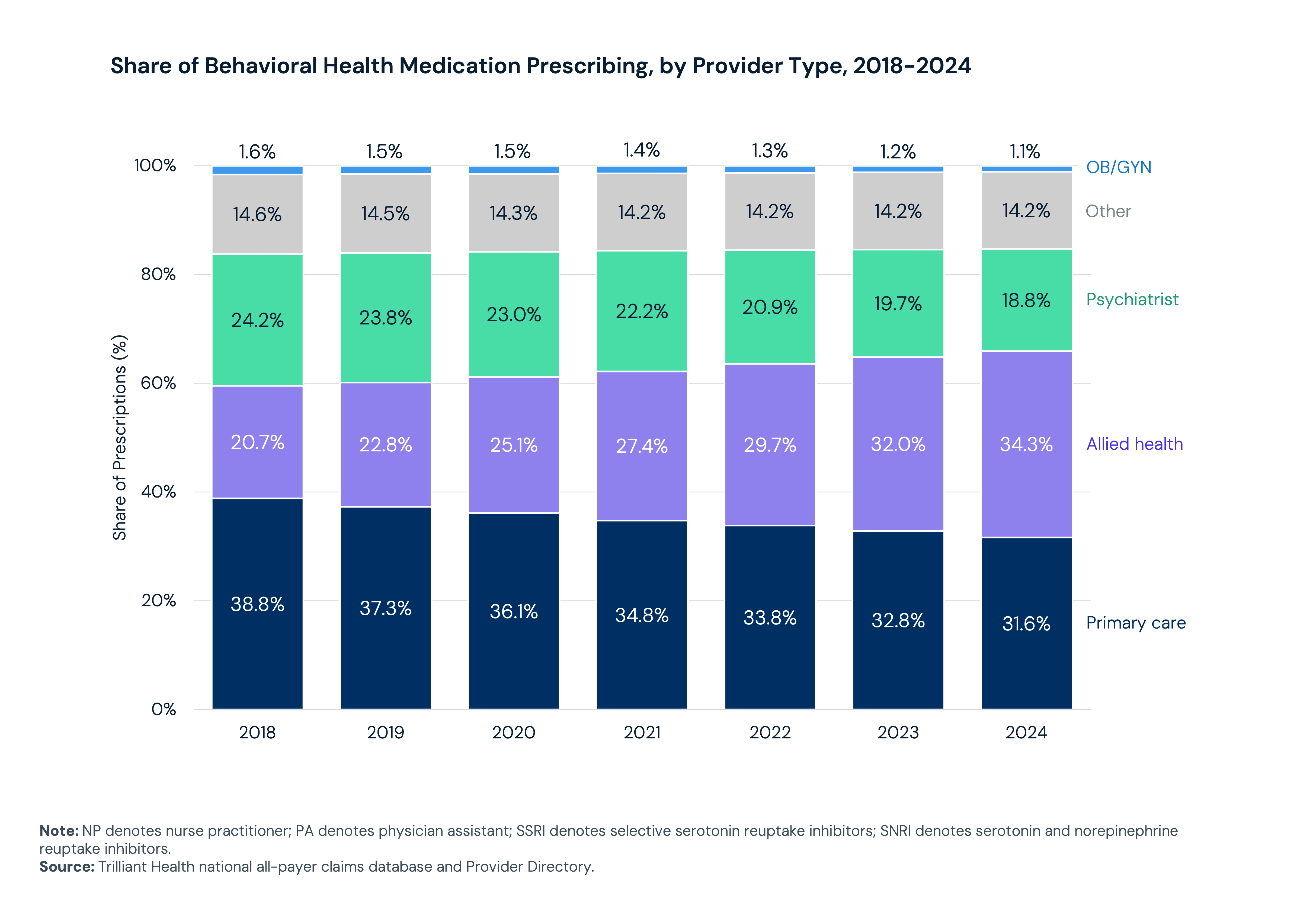

Allied health providers are managing a growing share of behavioral health prescription volume: Prescribing patterns for SSRIs, SNRIs, mood stabilizers and stimulants have shifted substantially in recent years. From 2018 to 2024, allied health providers (i.e., NPs and PAs) became the most common prescribing provider type, increasing from 20.7% to 34.3% of total prescription volume.

Increase in ABA therapy highlights behavioral health vulnerabilities: Since the introduction of new CPT codes in 2019, ABA visit volume has increased substantially across all payer types, reaching a growth rate of 309.2% in 2025.

.png)

Yield

The Nature of the U.S. Healthcare System Is Fundamentally Misaligned With Providing High-Value Care to Behavioral Health Patients

$477.5B

Estimated cost of untreated mental illness to the U.S. economy in 2024

65.2%

Percent of adults with mental health needs who cite cost as a barrier to treatment

7x

Variance in commercial negotiated rates for psychotherapy for the same CPT code

What's in the Report

Annual economic burden of untreated mental illness exceeds $477B: Untreated mental illness cost the U.S. economy an estimated $477.5B in 2024 and is projected to exceed $1.3T annually by 2040. Most projected costs are attributed to premature death ($911.9B) and workforce productivity losses ($252.3B) including unemployment, absenteeism and presenteeism.

Cost is a primary barrier to accessing behavioral health services: Cost remains a major barrier to behavioral health treatment, cited by 65.2% of adults with unmet mental health needs and 45.3% with substance use disorders. In addition, many also report insufficient insurance coverage.

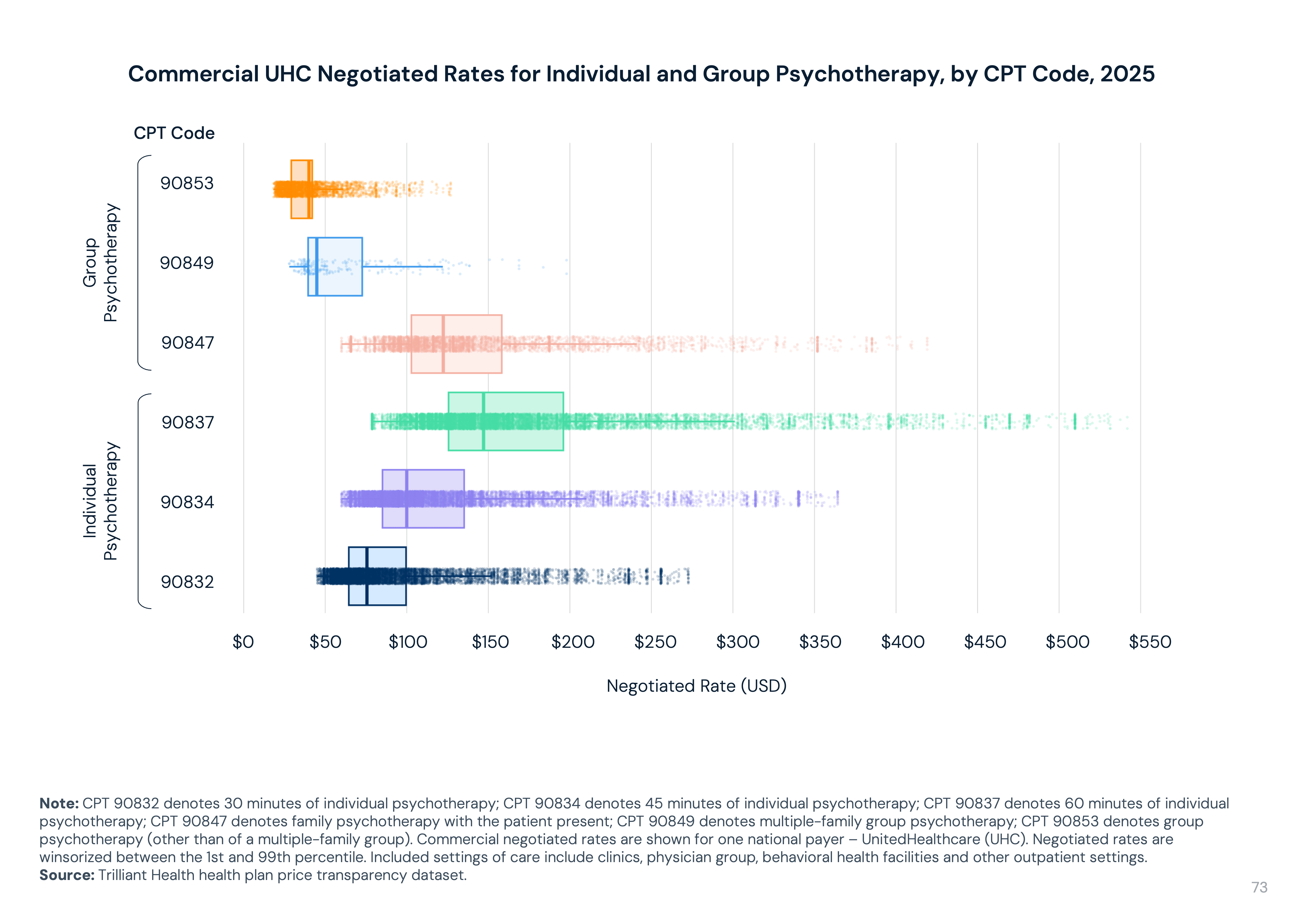

Psychotherapy negotiated rates vary by up to 7x: Commercial negotiated rates for UnitedHealthcare for individual and group psychotherapy codes vary by up to 7x. For example, the median negotiated rate for CPT 90837 (individual psychotherapy) is $147 but ranges from $78 to $542.

.png)

Conclusion

Stakeholder Imperatives for Action

.png)

Service Line Intelligence | BEHAVIORAL HEALTH

Read the Full 2026 Behavioral Health Report

ABOUT THE REPORT

84 Pages | PDF Download

About Trilliant Health

.png)