.png)

.png?width=171&height=239&name=2025%20Trends%20Report%20Nav%20(1).png)

New data reveal how the post-pandemic landscape is reshaping who gets care, who provides it and what it costs.

April 14, 2026According to Trilliant Health’s 2026 Behavioral Health Report, the U.S. behavioral health crisis is becoming more complex, more costly and increasingly misaligned with the system intended to treat it.

Demand for behavioral health care has surged in the years following the pandemic, but the number of providers, availability of services and access to affordable care have not kept pace with that growing need.

Nearly one in four American adults live with a mental illness, more than 48,000 people die by suicide each year and the economic burden exceeds an estimated $300B annually. What is less understood is how the structure of the healthcare system itself contributes to the gap between clinical need and access to care.

.png?width=275&height=260&name=Frame%20195789%20(1).png)

2026 Behavioral Health Report

The U.S. behavioral health crisis did not subside with the end of the pandemic – it was further amplified. Explore more than 50 data stories on the behavioral health crisis, including nationally representative analyses on prevalence, mortality, utilization, pricing and the future of the behavioral health workforce.

How Prevalent Are Mental Illness and Substance Use Disorders in the United States?

Nearly one in four American adults is currently living with a mental illness – and while prevalence has moderated slightly from pandemic-era peaks, it remains elevated compared to pre-pandemic baselines. The data make clear that behavioral health demand is growing in volume and intensity. It is a defining force shaping healthcare utilization, mortality and the financial performance of every sector of the health economy.

Between 2008 and 2024, prevalence of any mental illness among American adults increased by 5.7 percentage points. In 2024, substance use disorder (SUD) affected 17.7% of adults, and 8.1% of adults had both a mental illness and a substance use disorder.

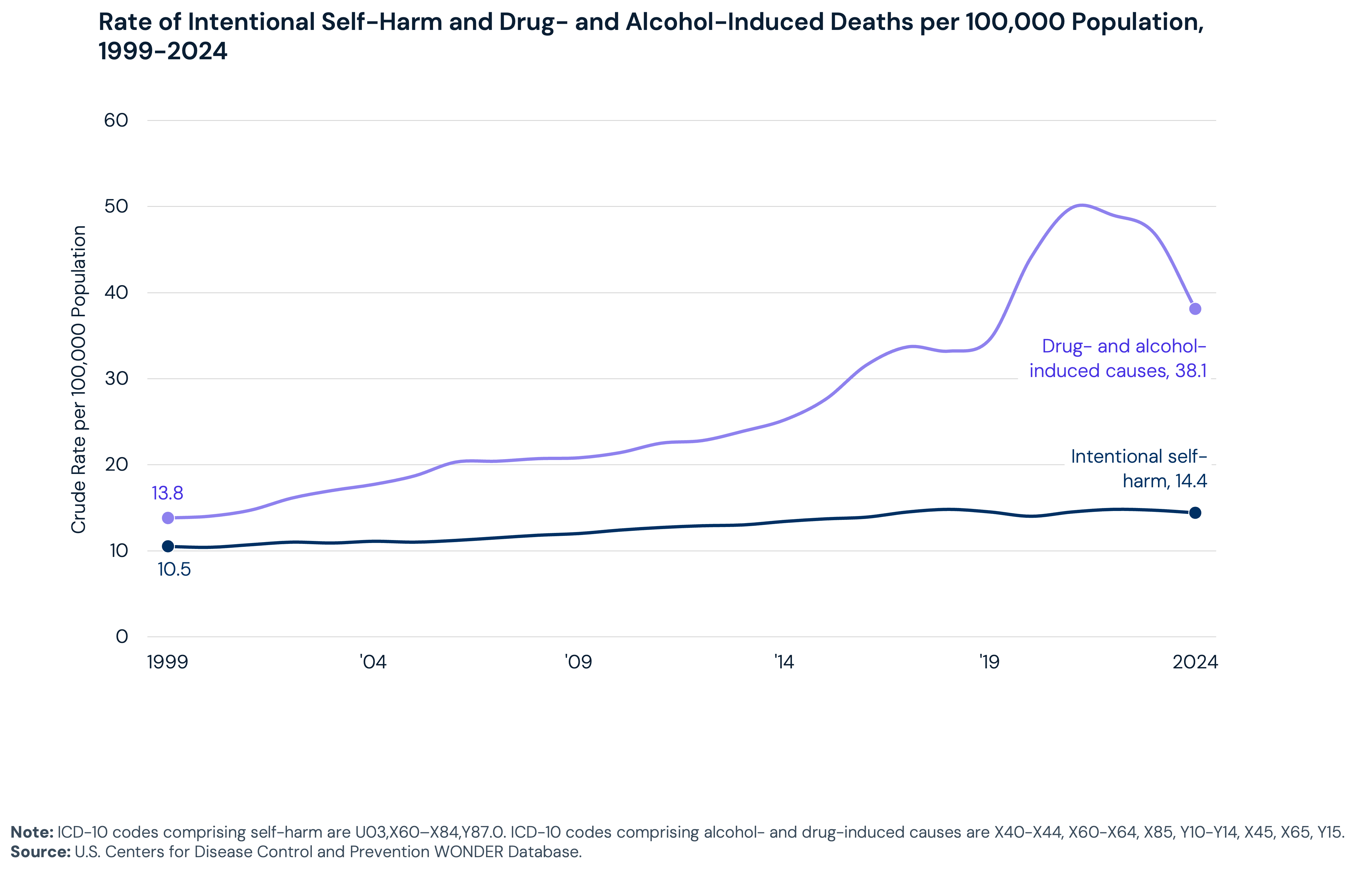

Mortality data reflect similar trends. Intentional self-harm accounted for over 48,000 deaths in 2024, making it the tenth leading cause of death in the United States. Drug- and alcohol-induced mortality has increased 176.1% since 1999, from 13.8 to 38.1 deaths per 100,000 people. That rate peaked at 49.9 per 100,000 in 2021 and has since declined but remains above pre-pandemic levels.

How Does Behavioral Health Impact Different Patient Populations?

The behavioral health crisis does not affect all Americans equally. Prevalence, mortality, access and treatment rates vary dramatically by age, race, insurance status and geography. In many cases, those disparities are widening. Understanding where the gaps are largest is essential for health economy stakeholders making data-oriented decisions regarding behavioral health.

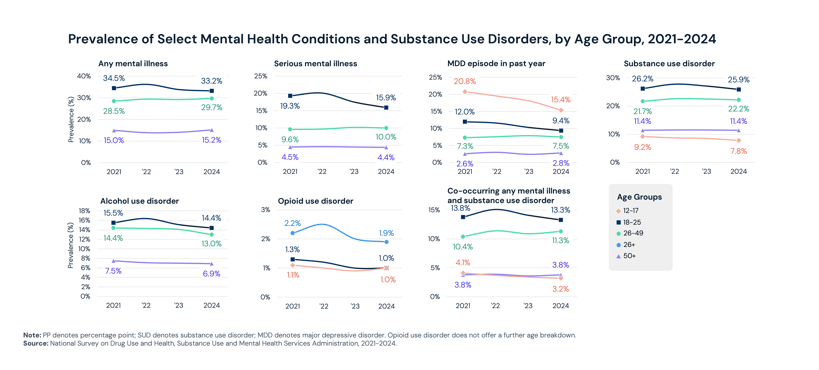

Adults ages 18–25 exhibit the highest prevalence of any mental illness and serious mental illness, 33.2% and 9.4% in 2024, respectively, though those rates are slightly below 2021 levels. More notably, prevalence has increased across nearly all behavioral health conditions over the same period among adults ages 26-49.

Across nearly every behavioral health condition examined, multiracial individuals had the highest prevalence rates: 35.5% for any mental illness, 24.9% for SUD and 13.1% for serious mental illness.

Low-income populations have disproportionately higher disease prevalence and treatment rates. Medicaid and CHIP beneficiaries have the highest rates of both behavioral health prevalence (31.9% for any mental illness) and treatment utilization (27.6% mental health; 7.4% substance use disorder). Notably, the uninsured present a troubling paradox: they have the second highest mental illness prevalence (24.7%), yet the lowest rate of mental health treatment of any insurance group.

Mortality disparities are also widening. While intentional self-harm mortality among White individuals declined 3.5% between 2018 and 2024, it increased 19.5% among Black individuals and 18.3% among multiracial individuals. For drug- and alcohol-induced deaths, American Indian and Alaska Native individuals have the highest mortality rate at 63.4 per 100,000, well above rates for White (40.3) and Black (44.3) individuals.

Mortality also varies by geography. Intentional self-harm mortality rates range from 6.3 per 100,000 in Washington, D.C. to 30.0 in Alaska. Drug- and alcohol-induced mortality ranges from 24.7 in Nebraska to 75.4 in Alaska and 75.2 in New Mexico. Western states consistently have the highest mortality rates, while the Northeast and Mid-Atlantic have the lowest.

How Is Behavioral Healthcare Delivered, and What Role Does Telehealth Play?

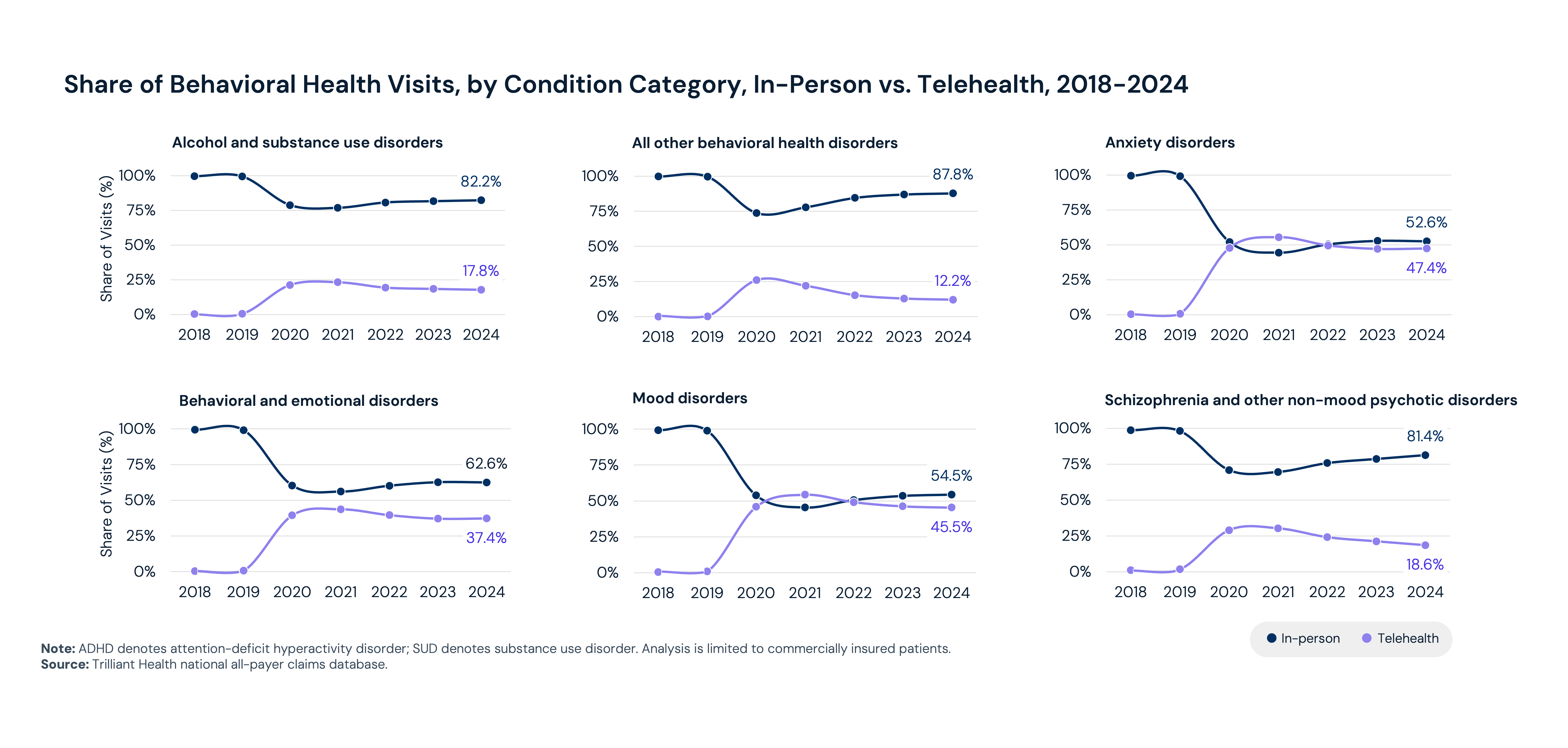

Where and how patients access behavioral healthcare has changed in recent years. Behavioral health has become the dominant use case for telehealth, accounting for 65.6% of all telehealth visits in 2024, up from 18.4% in 2018.

Between 2018 and 2024, behavioral health visits increased 62.6% nationally – growth that reflects expansion in both need and access. Telehealth is a common access point, with behavioral health accounting for 65.6% of all telehealth visits in 2024, up from 18.4% in 2018. During the COVID-19 pandemic, telehealth became the primary care setting for anxiety and mood disorders and approached parity for behavioral health and emotional disorders (e.g., ADHD, conduct disorders). Since 2023, in-person visits have again become most common for all conditions; however, there is meaningful variation. For example, 52.6% of visits for anxiety disorders take place in person compared to 82.2% of visits for alcohol and substance use disorders. However, the most acute patient needs are still going unmet.

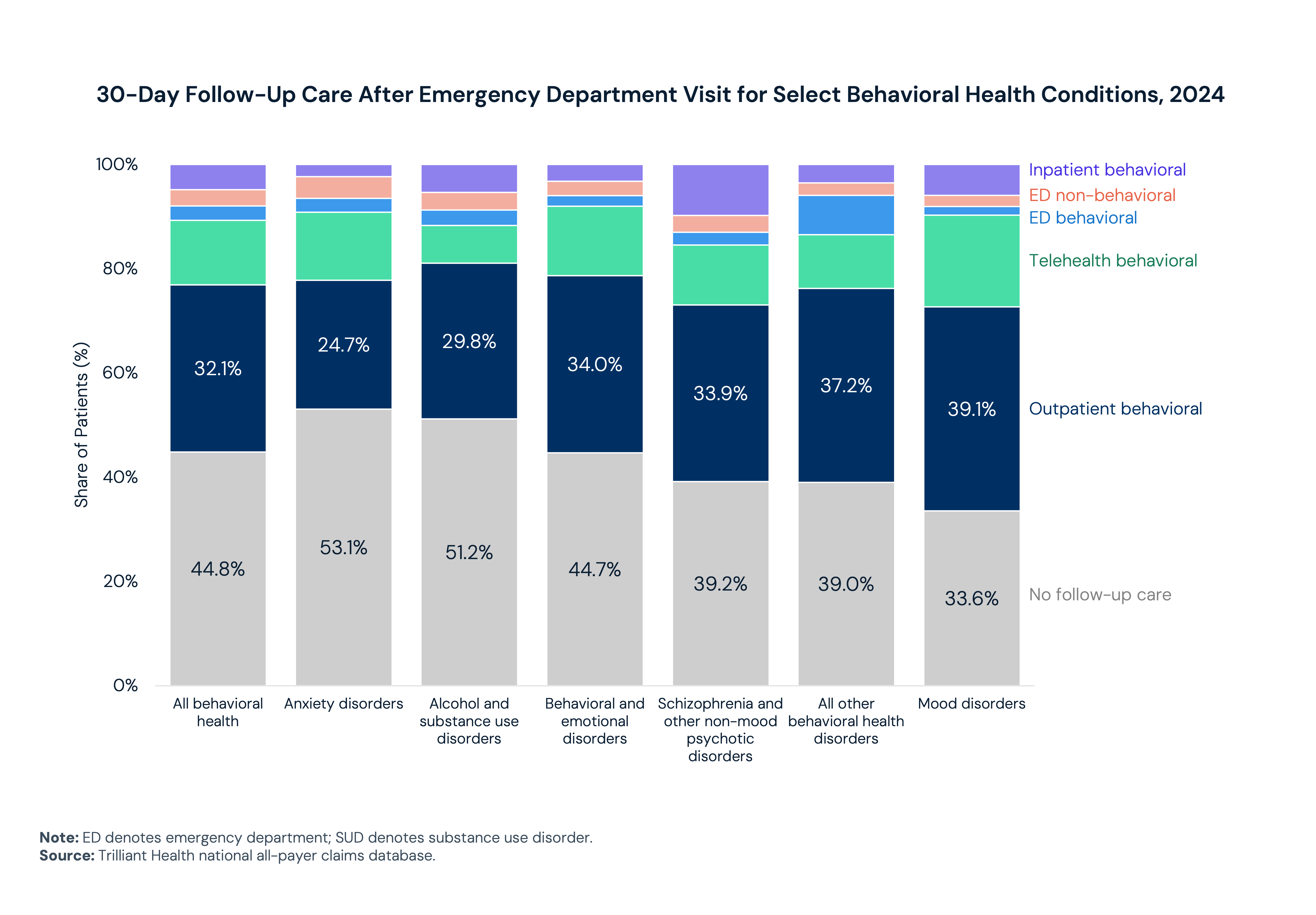

More than half of patients who present to an emergency department (ED) for anxiety or alcohol or substance use disorders did not receive specialized follow-up care within 30 days of discharge. These are high-acuity individuals whose contact with the healthcare system does not convert into continuity of treatment. And they are arriving in larger numbers. Alcohol and SUD now account for 39.1% of all behavioral health ED presentations, up from 33.8% in 2018.

The reason so many of these encounters fail to result in follow-up care is in large part structural. The behavioral health workforce cannot meet the demand placed upon it. By 2038, projected demand is expected to exceed supply by approximately 36,780 full-time equivalents (FTEs) in adult psychiatry and 99,780 FTEs in mental health counseling. The national average adequacy of mental health professionals is 27.3%. The workforce is also burning out – 83% of behavioral health providers reported burnout in a 2023 study, with therapists citing the highest rate of mental health fatigue of any specialty (77%).

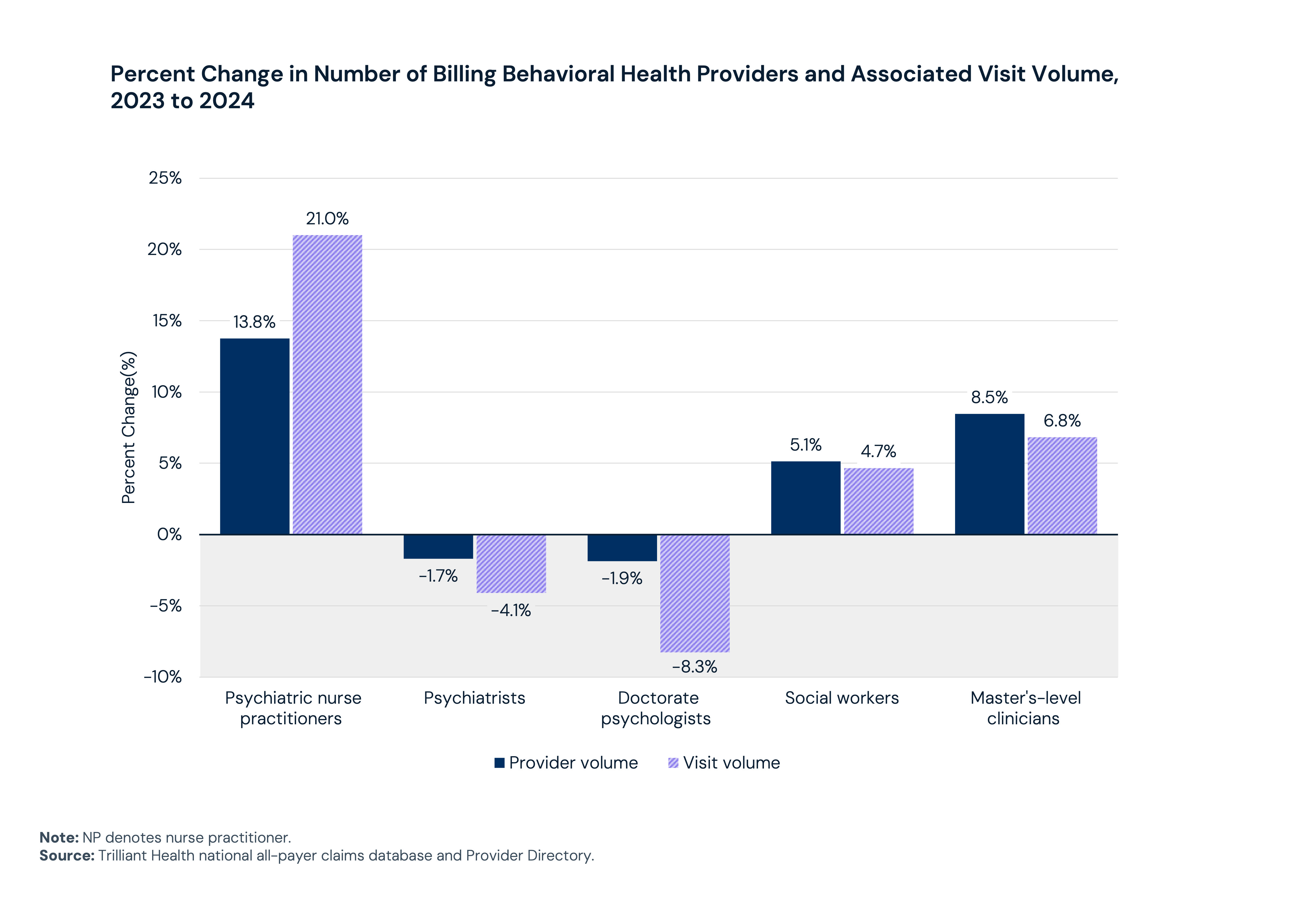

To meet the increasing demand, the behavioral health workforce is adapting. Between 2023 and 2024, provider supply and visit volumes increased among psychiatric nurse practitioners (NPs), social workers and master’s-level clinicians. In contrast, both provider supply and utilization among psychiatrists and doctorate-level psychologists decreased, with declines in visit volume outpacing declines in supply. Telehealth has expanded the geographic footprint of available care, while M&A activity is accelerating as the market consolidates in search of scale.

The gap between the utilization trends and the workforce capacity is a core challenge of behavioral health delivery in the U.S. today. It will require more than adding residency slots or expanding telehealth. Notably, despite 55% growth in the number of residency positions, which have maintained a nearly 100% match rate, supply remains artificially constrained by the number of available positions. It will require a reckoning with who the system is actually built to serve, and what it would take to serve them.

How Has Behavioral Health Prescribing Changed, and What Novel Therapies Are Coming to the Market?

Prescription medication has become a central component of behavioral health treatment, and the patterns of who is prescribing and what they are prescribing are changing. Stimulants have seen the fastest growth of any medication class, while allied health professionals have surpassed psychiatrists as the most common prescriber type. These shifts reflect both changing clinical needs and a workforce adapting to demand.

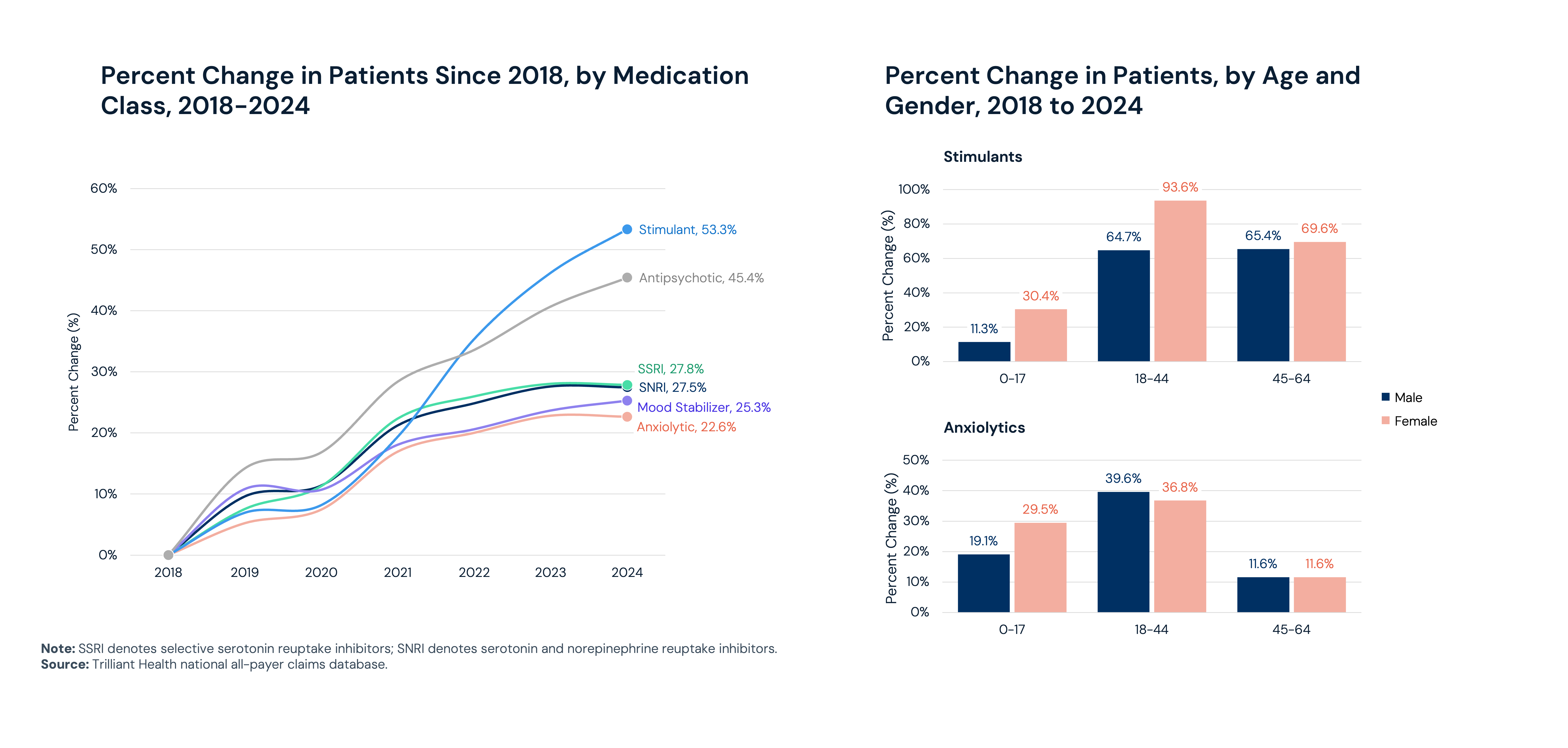

In 2024, 21.4% of women received prescription treatment for mental health, compared to 11.8% of men. Between 2018 and 2024, stimulants experienced the fastest growth of any medication class, up 53.3%, followed by antipsychotics (45.4%). Stimulant use has been particularly pronounced among women ages 18–44, where utilization grew 93.6% over the period.

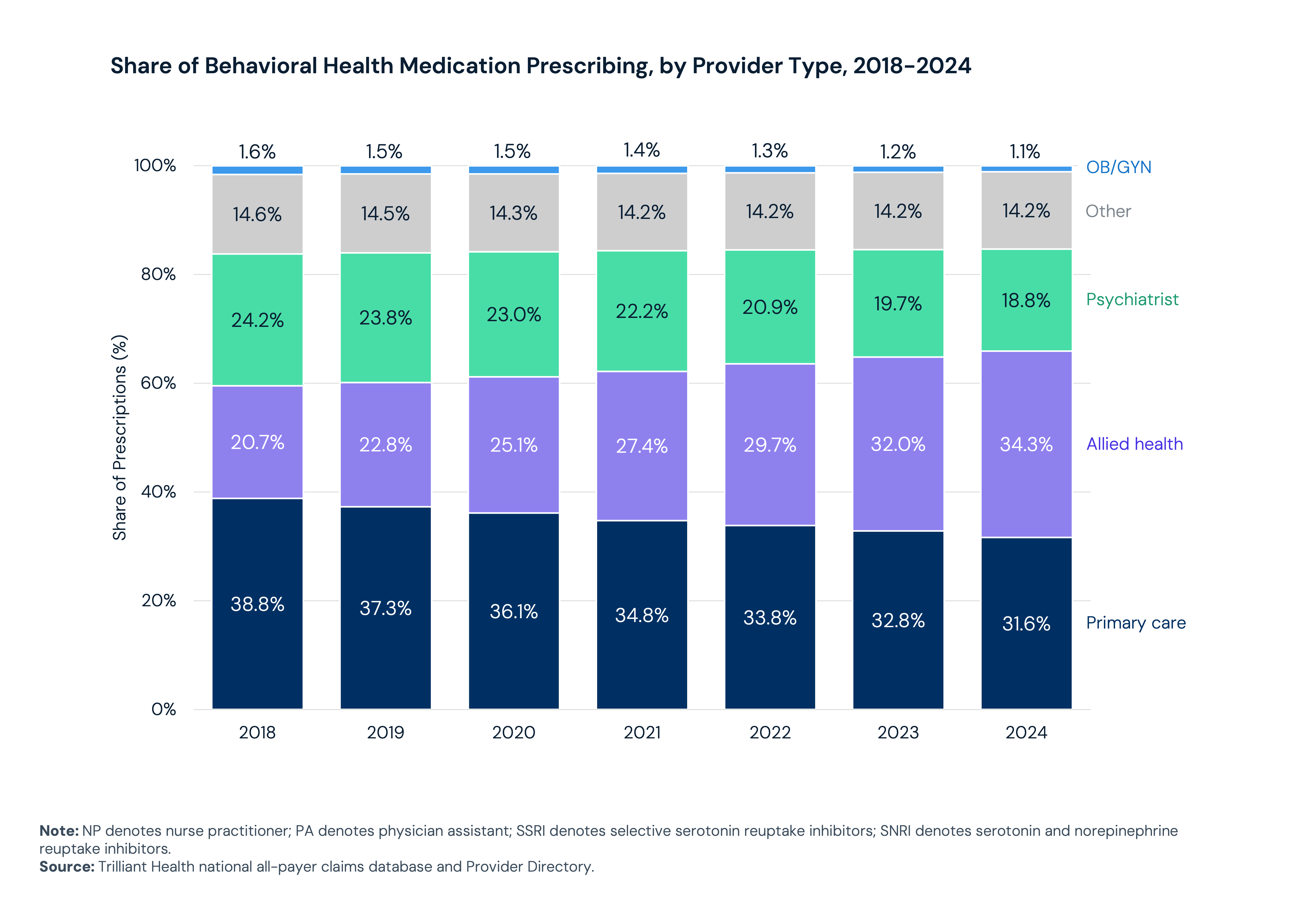

The composition of who prescribes these medications has shifted. Allied health professionals, including nurse practitioners and physician assistants, now account for 34.3% of behavioral health prescription volume, up from 20.7% in 2018. In 2024, they surpassed psychiatrists and primary care physicians to become the most common behavioral health prescriber type. Together, allied health providers and primary care physicians now account for 65.9% of all behavioral health prescription volume, reflective of a workforce that cannot adapt quickly enough to meet demand.

Emerging treatment modalities offer potential, but timelines remain uncertain. Ketamine, psilocybin and MDMA are under active clinical investigations for treatment-resistant depression and PTSD. The FDA approved the first at-home, non-invasive brain stimulation device for depression in December 2025. Prescription digital therapeutics — FDA-regulated software-based treatments — are expanding across conditions including generalized anxiety disorder, major depressive disorder, PTSD and SUD. Adoption of all these modalities will be shaped by regulatory progress, reimbursement decisions and clinical integration with existing care pathways.

How Are Direct-to-Consumer Providers Reshaping the Behavioral Health Market?

The behavioral health market is constantly evolving. Organizations are pursuing scale, integrating digital tools and building payer relationships to expand access and create continuity of care, but structural affordability barriers remain in place. For many patients, the proliferation of direct-to-consumer (DTC) platforms has increased pricing transparency without meaningfully reducing costs.

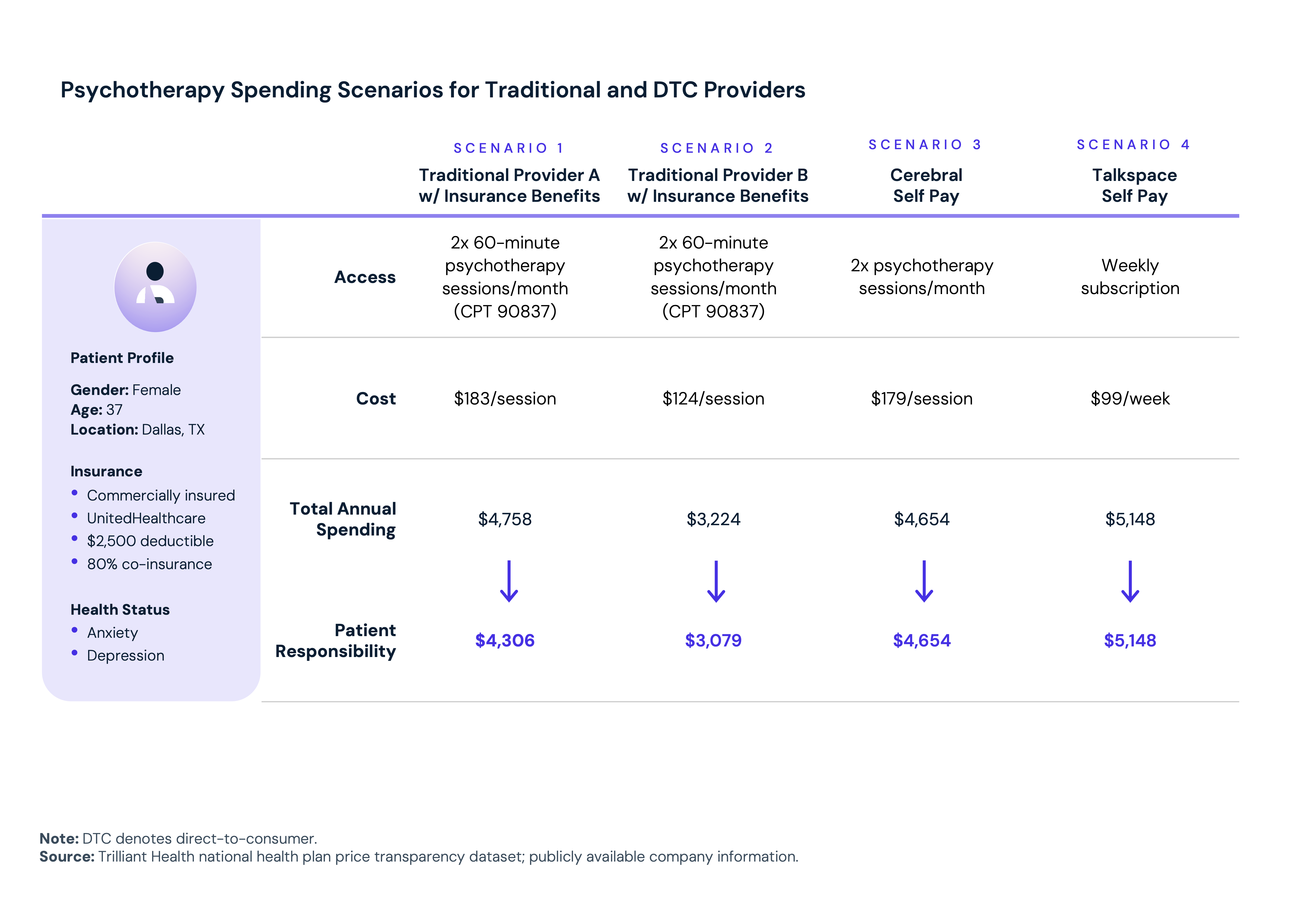

DTC online therapy platforms have proliferated, offering varying combinations of therapy, psychiatric services, medication management and subscription pricing. The transparency these platforms bring to pricing is real but does not necessarily equate to affordability. A commercially insured patient in Dallas, Texas with a $2,500 deductible, comparing two DTC options against two traditional in-network providers for bi-weekly psychotherapy, would face annual costs ranging from approximately $3,200 to $5,200. Navigating those tradeoffs is a barrier for many patients, particularly those with lower health literacy or less bandwidth to engage in benefit optimization.

This market continues to evolve. There were 167 behavioral health mergers and acquisitions in 2025. Mental health drove the market, accounting for 111 deals, including Spring Health's planned acquisition of Alma, expected to close in the second quarter of 2026 and Universal Health Services' announced acquisition of Talkspace in March 2026. These transactions reflect a broader effort to integrate digital tools, provider networks and payer relationships to expand access and create continuity of care at scale.

This market continues to evolve. There were 167 behavioral health mergers and acquisitions in 2025. Mental health drove the market, accounting for 111 deals, including Spring Health's planned acquisition of Alma, expected to close in the second quarter of 2026 and Universal Health Services' announced acquisition of Talkspace in March 2026. These transactions reflect a broader effort to integrate digital tools, provider networks and payer relationships to expand access and create continuity of care at scale.

What Does Behavioral Healthcare Cost, and Why Does It Vary So Dramatically?

The economic burden of the behavioral health crisis is staggering, and the pricing environment is making it worse. Cost is one of the most cited barriers to treatment, yet commercial negotiated rates for identical psychotherapy services can vary by as much as 7x nationally.

In 2019, mental health and substance use disorders together accounted for approximately $200B in U.S. healthcare spending — 8.0% of total personal healthcare expenditure. That figure has almost certainly grown since the pandemic. But the more consequential number may be the cost of what goes untreated: untreated mental illness cost the U.S. economy $477.5B in 2024 and is projected to exceed $1.3T annually by 2040. Premature death ($911.9B) and workforce productivity losses ($252.3B) — through unemployment, absenteeism and presenteeism — account for the majority of projected costs. Emergency department overutilization costs attributable to untreated mental illness are projected to grow 230.2% between 2024 and 2040.

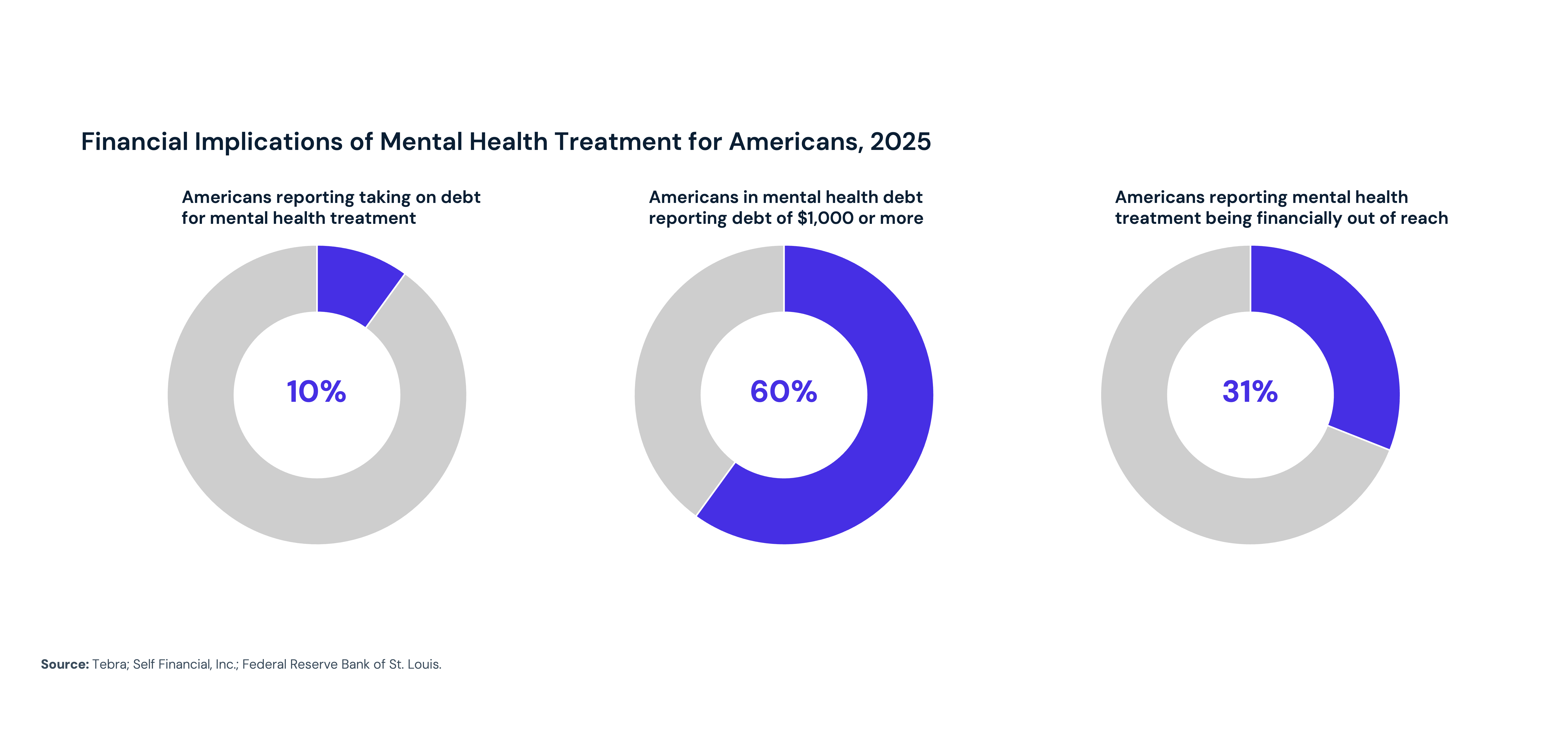

Cost remains one of the most cited barriers to behavioral health treatment — reported by 65.2% of adults with unmet mental health needs and 45.3% of those with substance use disorders. Nearly one in 10 Americans has taken on debt to pay for mental health treatment, and 60% of those individuals accumulated more than $1,000 in debt. The average individual spends $375 out-of-pocket monthly on mental health treatment, and 31% of Americans report that mental health treatment is financially out of reach.

Insights into negotiated rates contextualize this growing spending and unaffordability. Commercial negotiated rates for the same psychotherapy CPT codes vary by as much as 7x nationally. Intensive outpatient therapy has a median rate of $252 per day, but rates vary by a range of 14x. A single inpatient psychiatric room code has a median rate of $1,179 per day and ranges 22x. In a single market (Atlanta, Georgia) applying commercial negotiated rates for one inpatient psychiatric revenue code across 200 seven-day stays yields a spending difference of $7.9M depending solely on which hospital delivers the care.

How Is Behavioral Health Demand Forecasted to Change by 2030?

Behavioral health demand is projected to reach as many as 56.9M visits by 2030, with the fastest projected growth among adults ages 35–49 and in high-growth metros. But demand alone does not determine outcomes: the consequences will ultimately be shaped by how effectively the system confronts the workforce shortages, affordability barriers and structural fragmentation that leave the highest-need patients underserved.

Behavioral health demand is projected to grow at a compound annual growth rate of 0.2% to 1.5% through 2030, reaching up to 56.9M visits. Anxiety disorders alone are projected to account for 27.2M visits by 2030. Growth will be concentrated among adults ages 35–49 and in high-growth metropolitan areas — Austin, Texas leads with a projected CAGR of 3.1%, followed by Phoenix, Raleigh, Denver and Salt Lake City.

But those projections do not tell the full story. The trajectory of demand will be shaped by the availability of providers, the uptake of pharmacotherapy, screening guideline changes and the continued evolution of direct-to-consumer behavioral health platforms. More importantly, the consequences of that demand — in terms of mortality, productivity loss and healthcare spending — will be shaped by the extent to which the system is redesigned to meet it.

But those projections do not tell the full story. The trajectory of demand will be shaped by the availability of providers, the uptake of pharmacotherapy, screening guideline changes and the continued evolution of direct-to-consumer behavioral health platforms. More importantly, the consequences of that demand — in terms of mortality, productivity loss and healthcare spending — will be shaped by the extent to which the system is redesigned to meet it.

What the data makes clear is that incremental responses will not be sufficient. Expanding access requires confronting workforce shortages not just by adding residency slots, but with deliberate geographic distribution strategies, expanded scope-of-practice frameworks and compensation models that reduce burnout and retain providers. Addressing affordability requires reimbursement structures that reflect the actual value of behavioral health services and benefit designs that do not systematically deter utilization. And improving outcomes requires treating behavioral health not as a standalone service line, but as an integral component of whole-person care, one whose presence or absence shapes utilization, costs and outcomes across every other part of the health economy.

The behavioral health crisis is America's most consequential unresolved public health challenge. The question is no longer whether to act – it is whether the actions taken will be commensurate with the scale of the problem.

Get the latest insights delivered to your inbox.

Related Research

Was this shared with you?

Subscribe for weekly insights.

Subscribe to receive weekly insights from Trilliant Health's Research Team

Interested in citing our research? Please follow this guide.