.png)

.png?width=171&height=239&name=2025%20Trends%20Report%20Nav%20(1).png)

It is well established that the behavioral health status, inclusive of mental health, of Americans has declined since the onset of the COVID-19 pandemic, with 31.5% of adults reporting symptoms of anxiety or depressive disorder over that period. For comparison, between January and June 2019, 11.0% of adults reported symptoms of anxiety and/or depressive disorder.1 Even with unprecedented investments in behavioral health services over the past two years, the supply of behavioral health providers is insufficient to meet the rapidly accelerating demand for services, resulting in patients seeking care from non-behavioral health providers (e.g., primary care, emergency department).2,3

Background

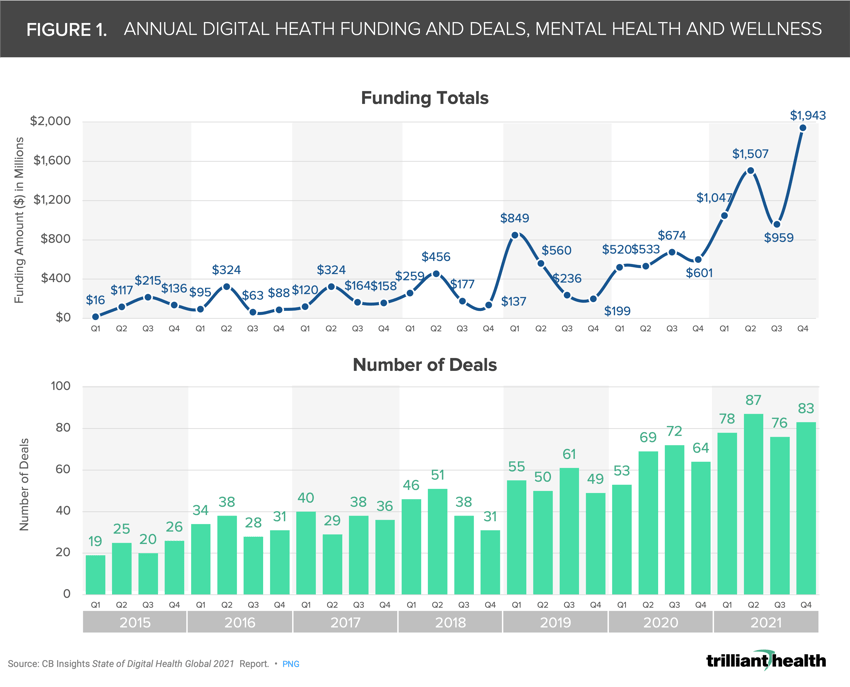

Given the lack of adequate provider supply, investments in tele-enabled and other digital capabilities have been touted as a solution to supplementing the behavioral health workforce.4,5,6,7 Private equity investments in the behavioral health sector, including drug therapies, virtual care, and digital health platforms, funding totaled $5.5B across 324 deals, representing 1,000% and 260% increases from 2015, respectively (Figure 1). Even so, questions remain on how to meet demand more effectively for services with “new” supply.

Analytic Approach

Analytic Approach

Two critical components of addressing the U.S. behavioral health crisis include quantifying 1) how patients are changing care behaviors amid growing virtual care options and 2) trends in patients seeking mental health care in the emergency department. To analyze behavioral health telehealth volumes, we identified visits with a diagnosis code within the major diagnostic category (MDC) 19 (Mental Health Diseases & Disorders) or 20 (Alcohol/Drug Use & Alcohol/Drug Induced Organic Mental Disorders) between January 2019 and December 2021. To analyze volumes in the emergency department, we segmented volumes into three categories: 1) isolated anxiety, 2) schizophrenia, bipolar disorder, and major depressive disorder, and 3) all other.

Findings

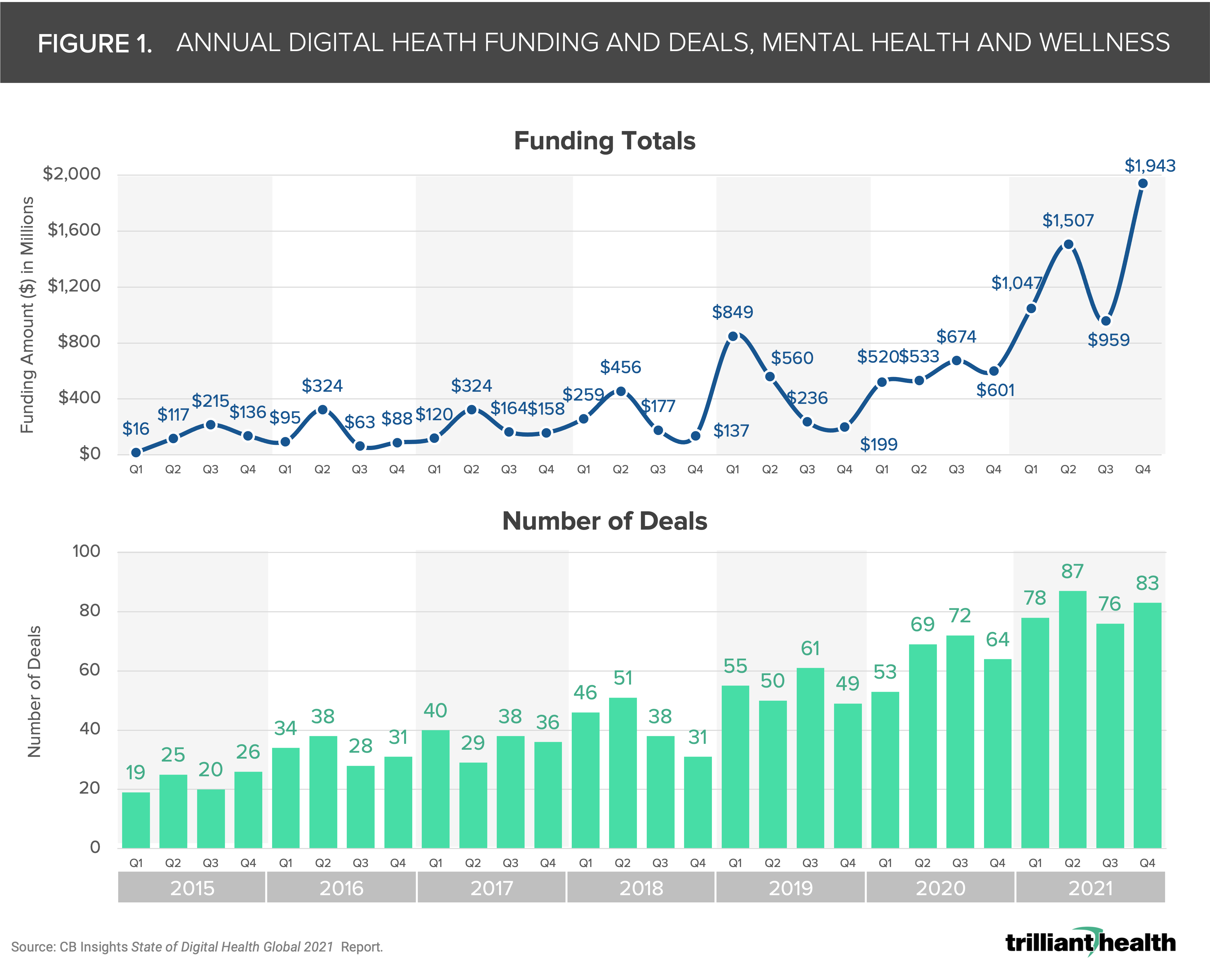

Based upon fundamental economic principles, telehealth is only a viable “substitute good” for behavioral health.8 Over the past two years, patients using telehealth for behavioral health purposes have increased dramatically, with visit volumes in both April 2020 and April 2021 more than 4,000% higher than in April 2019 (Figure 2).

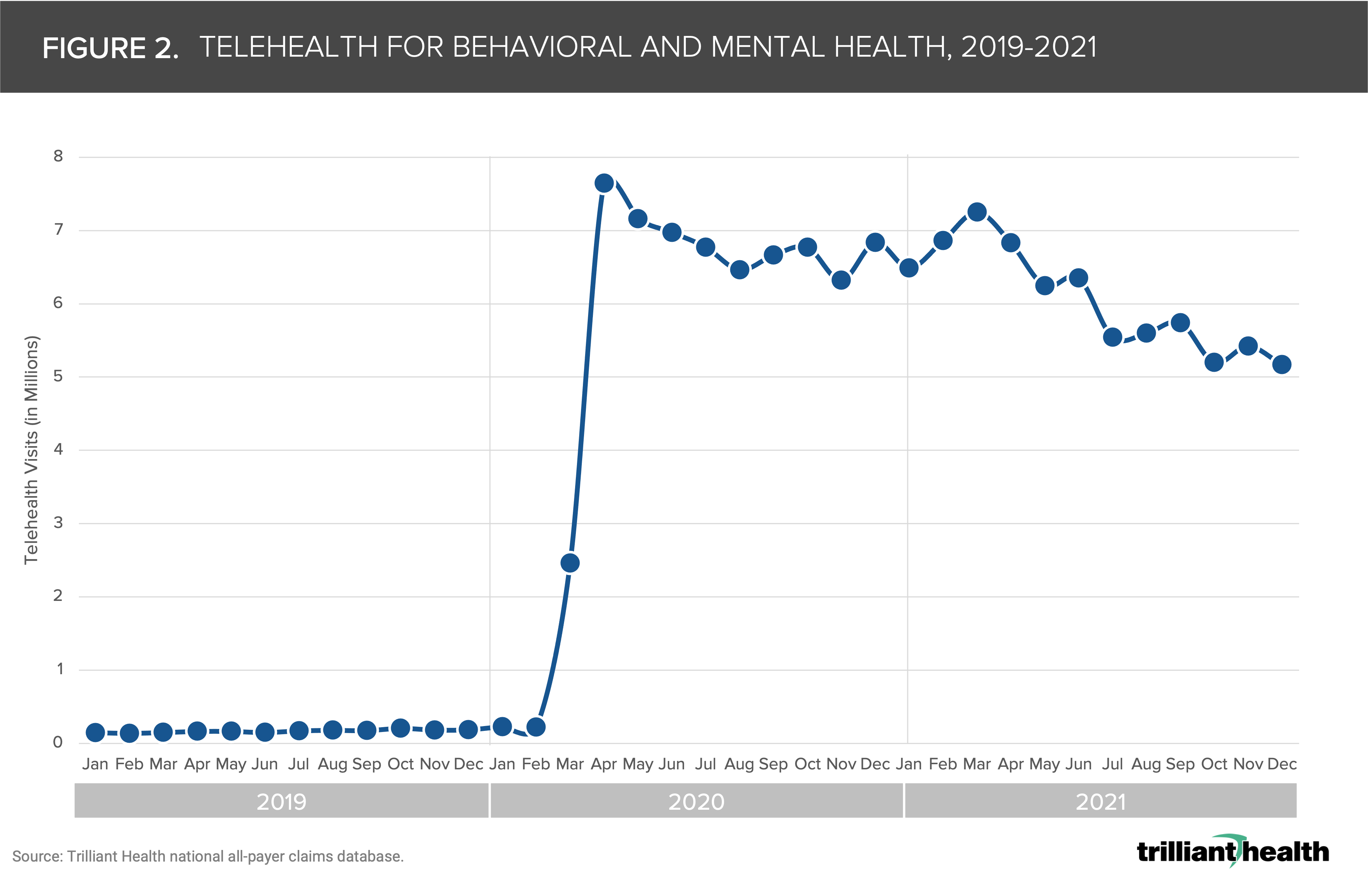

Notably, despite a national trend of delayed and deferred care for medical care, emergency department volumes for behavioral health conditions are consistently higher than pre-pandemic levels (Figure 3).9 During the height of nationwide COVID-19 lockdowns in April 2020, emergency department volumes for anxiety (-27.7%), schizophrenia, bipolar & major depressive disorder (-25%), and all other mental health disorders (-32.4%) declined from April 2019 volumes (Figure 4). However, April 2021 emergency department volumes are significantly higher than April 2019 volumes for each category: anxiety (8.9%), schizophrenia, bipolar & major depressive disorder (35%), and all other mental health disorders (25.2%).

Notably, despite a national trend of delayed and deferred care for medical care, emergency department volumes for behavioral health conditions are consistently higher than pre-pandemic levels (Figure 3).9 During the height of nationwide COVID-19 lockdowns in April 2020, emergency department volumes for anxiety (-27.7%), schizophrenia, bipolar & major depressive disorder (-25%), and all other mental health disorders (-32.4%) declined from April 2019 volumes (Figure 4). However, April 2021 emergency department volumes are significantly higher than April 2019 volumes for each category: anxiety (8.9%), schizophrenia, bipolar & major depressive disorder (35%), and all other mental health disorders (25.2%).

Even as investment activity continues at its current pace, a long-term mismatch between supply and demand for behavioral health services will affect many stakeholders in the health economy. Health systems, for example, must address the staffing, access, revenue, and patient satisfaction implications of increasing emergency department volumes for behavioral health. Every stakeholder should consider the limitations of emerging digital health platforms for treating more severe and complex conditions that usually require a more high-touch approach than a virtual visit.10 In future research, we will explore the increasing severity and acuity of behavioral health conditions since the onset of the pandemic and the implications for settings of care.

Thanks to Kelly Boyce and Katie Patton for their research support.