.png)

.png?width=171&height=239&name=2025%20Trends%20Report%20Nav%20(1).png)

Study Takeaways

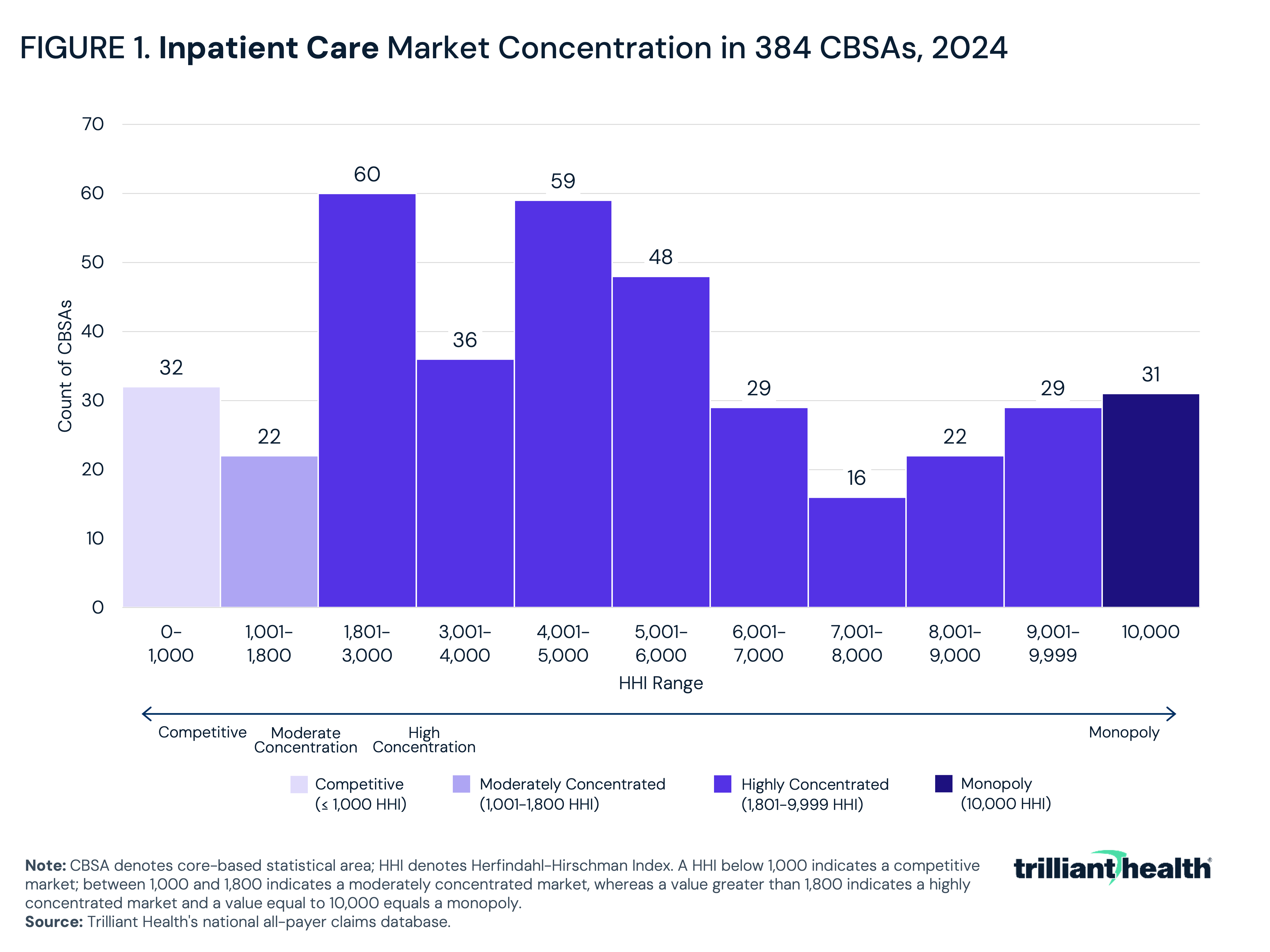

- In 2024, 77.9% of the 384 CBSAs analyzed had highly concentrated markets for inpatient care, with an additional 8.1% classified as a monopoly market.

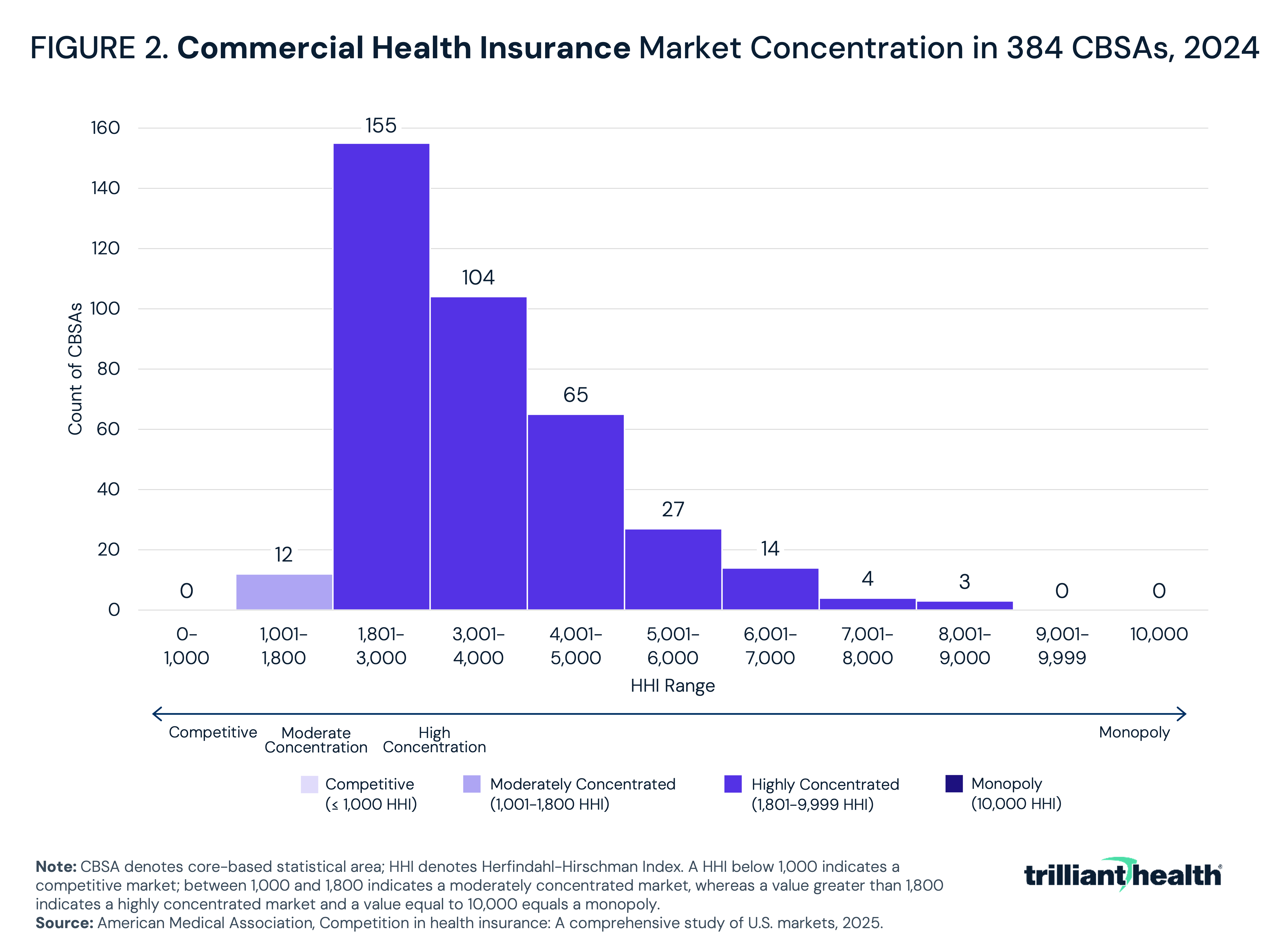

- In 2024, 96.9% of the 384 CBSAs analyzed had highly concentrated commercial health insurance markets.

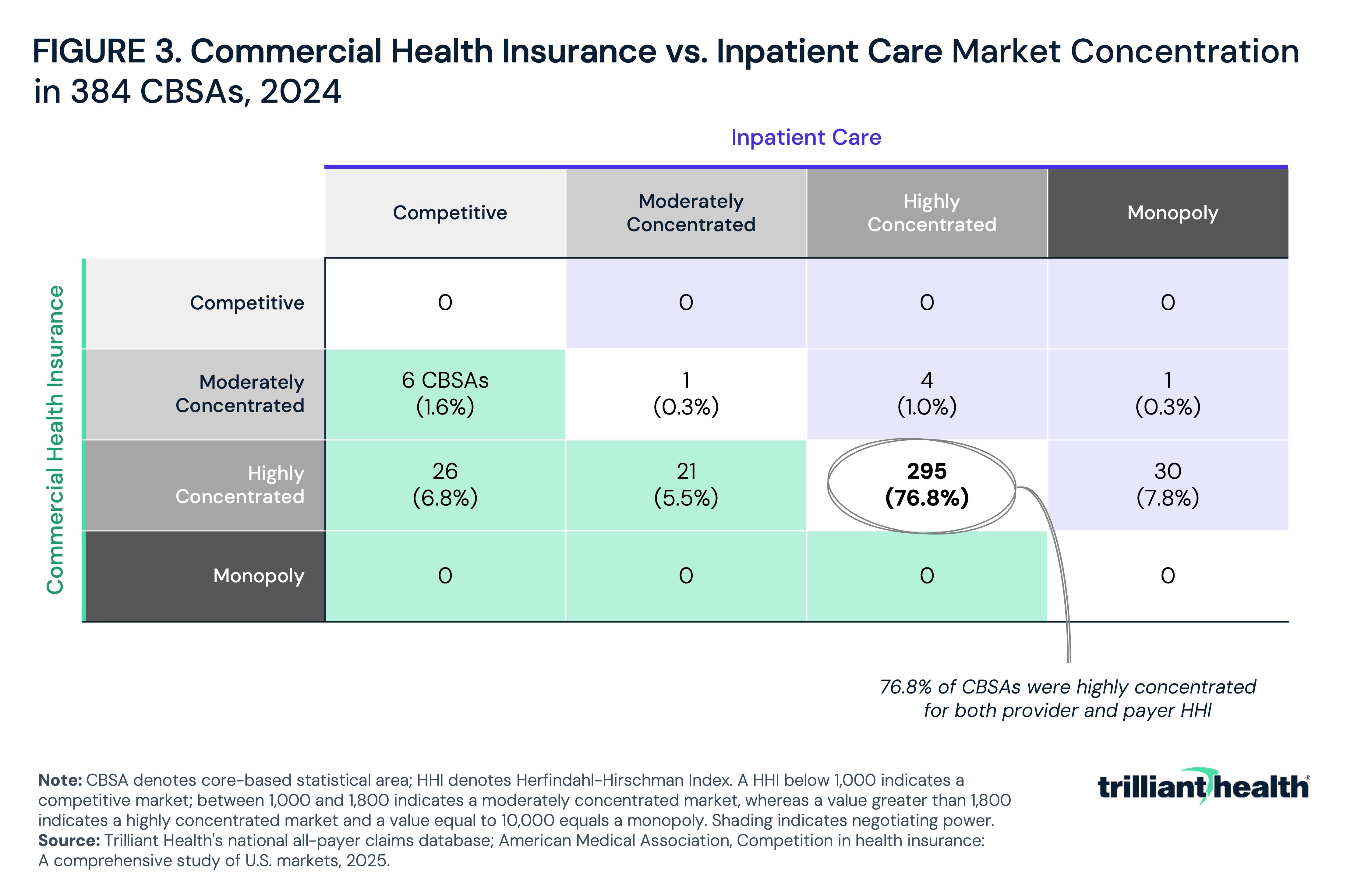

- Notably, 76.8% of CBSAs were highly concentrated in both inpatient care and commercial health insurance, and 7.8% had a monopoly inpatient care market with a highly concentrated commercial health insurance market.

Analyzing healthcare market competition based on provider or insurer concentration, in isolation, provides an incomplete narrative. Because the relationship between providers and payers ultimately shapes local market dynamics, focusing exclusively on hospital or payer concentration is insufficient to draw meaningful conclusions to inform regulatory policy. For decades, health insurers have been scrutinized over market power, while increasing hospital consolidation has resulted in a persistent narrative that dominant health systems leverage their network status to secure unjustifiably high negotiated rates. The validity of these similar, but previously independent, narratives depends on the market-level competitive conditions for both providers and payers.

Background

The Federal government utilizes the Herfindahl-Hirschman Index (HHI) as the standard measure of market concentration. HHI is calculated by squaring the market share of each firm competing in a market and summing the resulting numbers. It approaches zero when a market is occupied by several firms of relatively equal size and reaches its maximum of 10,000 when controlled by a single firm. As of 2023, the U.S. Department of Justice (DOJ) and Federal Trade Commission (FTC) considers markets with an HHI between 1,000 and 1,800 to be moderately concentrated and those exceeding 1,800 to be highly concentrated. Transactions that increase HHI by more than 100 points in highly concentrated markets are presumed likely to enhance market power.1 These thresholds represent a more aggressive approach to anti-competitive behavior by DOJ, compared to pre-2023 guidelines that were more generous in defining highly concentrated markets (2,500 vs. 1,800) and required a larger change in HHI (greater than 200 vs. 100) to trigger a presumption of illegality.

The use of HHI in healthcare has traditionally focused on horizontal competition, either measuring provider market share based on inpatient discharges or payer market share based on the number of health plans and their covered lives. While standard economic theory would suggest that hospitals operating in less competitive markets would achieve greater margins, research has shown that even hospital monopolies frequently operate with negative margins, indicating that market structure alone does not confer financial advantage.2 Separately, while improved care continuity and clinical integration have been a primary justification for hospital mergers and acquisitions, the evidence supporting these outcomes remains limited – and literature has consistently found that hospital consolidation has been associated with higher prices.3,4 Markets where hospital and payer concentration are mismatched may create meaningful imbalances in negotiating leverage, with downstream effects on negotiated rates and overall spending.

This analysis seeks to examine the interplay between provider consolidation and payer market dynamics to provide foundational context to inform regulatory policy.

Analytic Approach

Provider HHI was calculated using national all-payer claims, which captures facility-level inpatient discharges. For the 384 metropolitan CBSAs analyzed, market shares were assigned to individual hospital systems based on their share of total inpatient discharges. HHI was then computed by summing the squared market shares of all systems operating within each market. CBSAs were classified as competitive (HHI 0–1,000), moderately concentrated (1,001–1,800), highly concentrated (1,801–9,999) or monopoly (10,000) in accordance with DOJ and FTC guidelines. Payer HHI was sourced from the American Medical Association's Competition in Health Insurance: A Comprehensive Study of U.S. Markets, 2025, which reports insurer-level enrollment shares and HHI values for fully insured and self-insured commercial markets by CBSA. Using the same concentration thresholds, each of the 384 metropolitan CBSAs analyzed was classified as having a competitive, moderately concentrated, highly concentrated or monopoly payer market. As of 2024, the sample of studied CBSAs accounted for 86.4% of the U.S. population, with the largest CBSAs being New York-Newark-Jersey City, NY-NJ, Los Angeles-Long Beach-Anaheim, CA and Chicago-Naperville-Elgin, IL-IN.5

Findings

Of the 384 CBSAs analyzed, the majority (77.9%) had a highly concentrated provider market in 2024 (Figure 1). Among highly concentrated markets, the average HHI value was 5,249, and 60 markets had a payer HHI that was relatively close to the cutoff for moderately concentrated, while 29 approached monopoly status. The next most prevalent category was competitive, representing 32 markets (8.3%), including Los Angeles-Long Beach-Anaheim, CA (154 HHI), New York-Newark-Jersey City, NY-NJ (192 HHI) and Chicago-Naperville-Elgin, IL-IN (214 HHI). Notably, 8.1% were considered a monopoly market, including Bellingham, WA, Ithaca, NY and Fairbanks-College, AK. Finally, 5.7% were moderately concentrated with a value between 1,001 and 1,800, including Providence-Warwick, RI-MA (1,033), Nashville-Davidson-Murfreesboro-Franklin, TN (1,059) and Milwaukee-Waukesha, WI (1,077). Using the pre-2023 guidelines, 11.2% would have been considered competitive, and 10.2% would have been considered moderately concentrated.

In analyzing payer HHI, 96.9% of CBSAs were considered highly concentrated in 2024 (Figure 2). Among highly concentrated markets, most CBSAs (155) had a commercial market HHI value between 1,801 and 3,000. The remaining 3.1% of markets were moderately concentrated. Notably, there were not any competitive or monopoly payer markets. More specifically, nearly half (47%) of CBSAs had one health insurer that had market share of at least 50%. Nationally, the five largest health insurers by market share were: UnitedHealth Group (16%), Elevance Health (12%), CVS/Aetna (12%), Cigna (9%) and Health Care Service Corporation (8%). Collectively, however, Blue Cross Blue Shield insurers would lead the list with a combined commercial market share of 43%.

When looking at provider and payer HHI together, the majority of markets (76.8%) were highly concentrated for both sectors in 2024 (Figure 3). For example, Houston-Pasadena-The Woodlands, TX and Tampa-St. Petersburg-Clearwater, FL were characterized as highly concentrated for both inpatient care and health insurance (Figure 4). The next most common scenario was a monopoly inpatient care market in a highly concentrated commercial health insurance market (7.8%), as seen in Auburn-Opelika, AL, followed by a competitive inpatient care market paired with a highly concentrated commercial health insurance market (6.8%), like Denver-Aurora-Centennial, CO. An additional 21 CBSAs (5.5%) had a moderately concentrated inpatient care market alongside a highly concentrated commercial health insurance market, such as Nashville-Davidson-Murfreesboro-Franklin, TN. Six CBSAs (1.6%) – including New York-Newark-Jersey City, NY-NJ and Seattle-Tacoma-Bellevue, WA – were characterized by a competitive inpatient care market paired with a moderately concentrated commercial health insurance market. Four CBSAs (1.0%), including Orlando-Kissimmee-Sanford, FL, had a highly concentrated inpatient care market alongside a moderately concentrated commercial health insurance market. Providence-Warwick, RI-MA was the only market where both sectors were moderately concentrated, while Glens Falls, NY was the only market with a monopoly inpatient market paired with a moderately concentrated commercial insurance market.

Conclusion

Based on current FTC and DOJ guidelines, there were not any competitive health insurance markets in the 384 metropolitan CBSAs studied in 2024, and there were very few (31) competitive inpatient care markets. In commercial health insurance, 96.9% of metropolitan CBSAs were classified as highly concentrated, and in nearly half (47%) of those, a single insurer accounted for 50% or more of commercial health insurance options. Among inpatient care markets, 77.9% were highly concentrated and 8.1% were monopolies.

Examining provider and payer HHI together reveals insights that neither measure captures alone. Markets where the provider market is more concentrated than the payer market, or vice versa, represent distinct competitive environments with different implications for rate setting. The fact that 76.8% of markets have matched concentration levels between providers and payers suggests that most markets feature a relative balance of market power when negotiating commercial rates. Situations where neither party holds a disproportionately dominant position should moderate the most extreme pricing outcomes even in the absence of traditional competition. Where that symmetry breaks down (i.e., one side holds meaningfully greater concentration than the other), the conditions for outsized rate-setting leverage, and ultimately higher costs for patients and employers, are more likely to emerge. Denver-Aurora-Centennial, CO is an example of this asymmetry, with a competitive inpatient care market paired with a highly concentrated commercial insurance market, which would theoretically suggest that payers have more negotiating leverage than providers.

Importantly, the commercial health insurance market has largely moved beyond the era of horizontal consolidation to vertical integration. With concentration already high in all but 12 metropolitan CBSAs, the incremental competitive impact of additional insurer-to-insurer mergers is limited. UnitedHealth Group's acquisition of Optum-owned physician practices has produced one of the largest employed physician networks in the country. CVS Health's acquisition of Aetna combined a major insurer with a pharmacy benefit manager and retail health platform. Cigna's ownership of Express Scripts similarly integrates pharmacy and benefits management functions. These vertical strategies enable insurers to compete not only on premium pricing and network breadth, but on the ability to direct care, manage costs and capture margin across the care continuum. The latter strategy, also known as “profit tunneling,” allows health insurers to evade profit regulation, ultimately undermining regulatory intent and increasing healthcare spending.6 These complex dynamics are not captured in HHI alone.

While the hospital market continues to integrate horizontally, health systems have integrated vertically by acquiring physician groups, outpatient facilities and health plans. Ascension acquired AMSURG, one of the largest ambulatory surgery center operators in the country, gaining ownership of hundreds of outpatient surgical sites. HCA Healthcare acquired Brookdale's home health and hospice operations and has developed a sizeable urgent care platform, extending its reach well beyond the hospital setting. Community Health Systems and other large systems have similarly pursued outpatient and post-acute acquisitions to capture patient volume – and margin – that would otherwise migrate outside their walls. These moves position large health systems not just as providers negotiating with insurers, but as integrated enterprises.

Antitrust policy and Congressional legislation that focuses solely on either hospitals or health insurers is fundamentally flawed in the absence of a complete picture of how market dynamics interact across both sides. The use of HHI as a comprehensive indicator of the relationship between competition and price also warrants scrutiny, as research has found that some of the most competitive hospital markets are also the most expensive (e.g., New York-Newark-Jersey City, NY-NJ, Los Angeles-Long Beach-Anaheim, CA and Chicago-Naperville-Elgin, IL-IN).7 Unlike other industries, more competition in healthcare does not always ensure lower prices. Further, the Congressional Budget Office (CBO) also has concluded that "policies that increase antitrust enforcement or reduce providers’ incentives to consolidate would have less of an immediate effect on prices; however, those policies would contribute to price reductions over the longer term," which raises reasonable questions about the extent to which historic antitrust frameworks are well-suited to addressing competition in the near term.8 CBO estimated that “adopting all of the provider-competition policies…would reduce prices by a small amount (from more than [1% to 3%]),” which is significantly lower than historic or projected growth in healthcare costs. These considerations suggest that a more nuanced and integrated view of market power (i.e., one that accounts for both provider and payer concentration, as well as vertical integration) may be more useful in analyzing market power and in conceptualizing competition in healthcare.

Get the latest insights delivered to your inbox.

Was this shared with you?

Subscribe for weekly insights.

Subscribe to receive weekly insights from Trilliant Health's Research Team

Interested in citing our research? Please follow this guide.