.png)

.png?width=171&height=239&name=2025%20Trends%20Report%20Nav%20(1).png)

You are currently viewing the public version of Studies. To unlock the full study and additional resources, upgrade your subscription to Compass+.

Part 1 of 2: The Current Landscape of Provider-Sponsored Health Plans

In an era of constrained revenues, health systems have invested in provider-sponsored health plans (PSHPs) as a growth strategy. In theory, PSHPs allow health systems to control outcomes and costs, enhance profitability, improve population health and facilitate access to comprehensive local networks. Since their inception in the mid-1950s, over 200 provider entities have established PSHPs. Unsurprisingly, the PSHPs with the largest membership are owned by health systems with revenue in excess of $10B.

Background

PSHPs are health insurance companies owned fully or partially by a health system, hospital, physician group or other provider entity, meaning the same entity provides healthcare services and insurance. Some PSHPs cover a single product (e.g., Medicaid managed care), while others offer a diverse portfolio of insurance products for public and commercial sectors. Providers can create these plans by acquiring an existing insurer, converting from a preferred provider organization network into a licensed health insurance company or creating a joint venture with an established insurer.

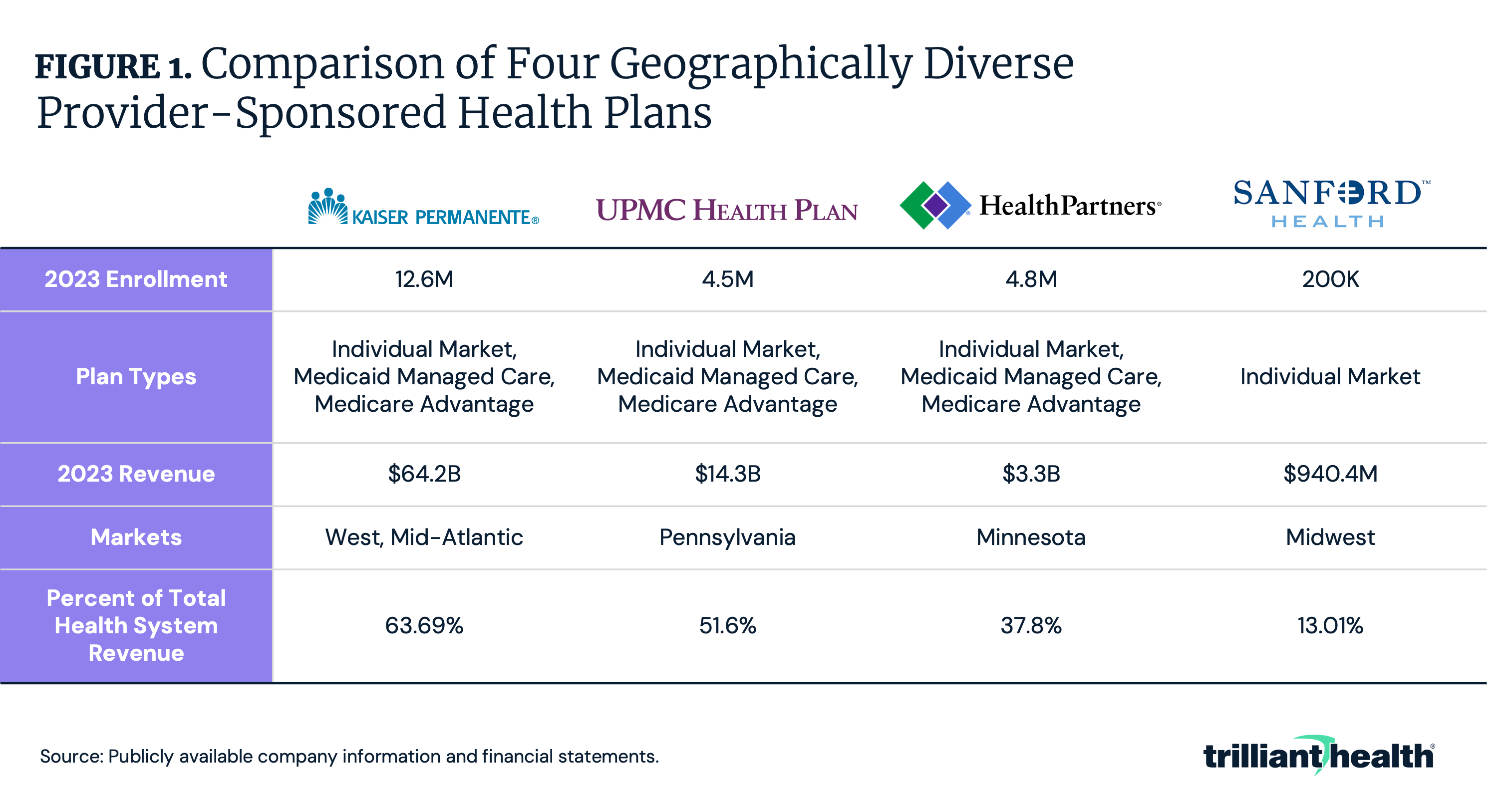

Comparing four geographically diverse PSHPs, total enrollment across insurance products ranged from 200K enrollees (Sanford Health) to 12.6M enrollees (Kaiser Permanente) (Figure 1). PSHPs contributed to more than 50% of Kaiser Permanente and UPMC’s total system revenue, while health plans only accounted for 12% of Sanford Health’s total system revenue.

Notably, more than one in ten health plans started between 1957 and 2017 were no longer active in 2024. Despite potential cost-saving benefits, PSHPs have delivered mixed results. Only four of the 43 PSHPs formed or acquired between 2010 and 2015 were profitable in 2015.1 The disappointing financial results were attributable to a variety of factors, including difficulties in scaling, marketing, enrollment, hyper-regional focus and regulatory compliance.

Even profitable plans have seen revenue fluctuations, creating uncertainty around their viability as a revenue diversification strategy. Despite their inconsistent operating results, PSHPs remain a cornerstone of many health systems’ strategies. Therefore, we analyzed enrollment, market share and the types of insurance products offered by various health systems to understand the current landscape and challenges faced by PSHPs.

Health System Trends

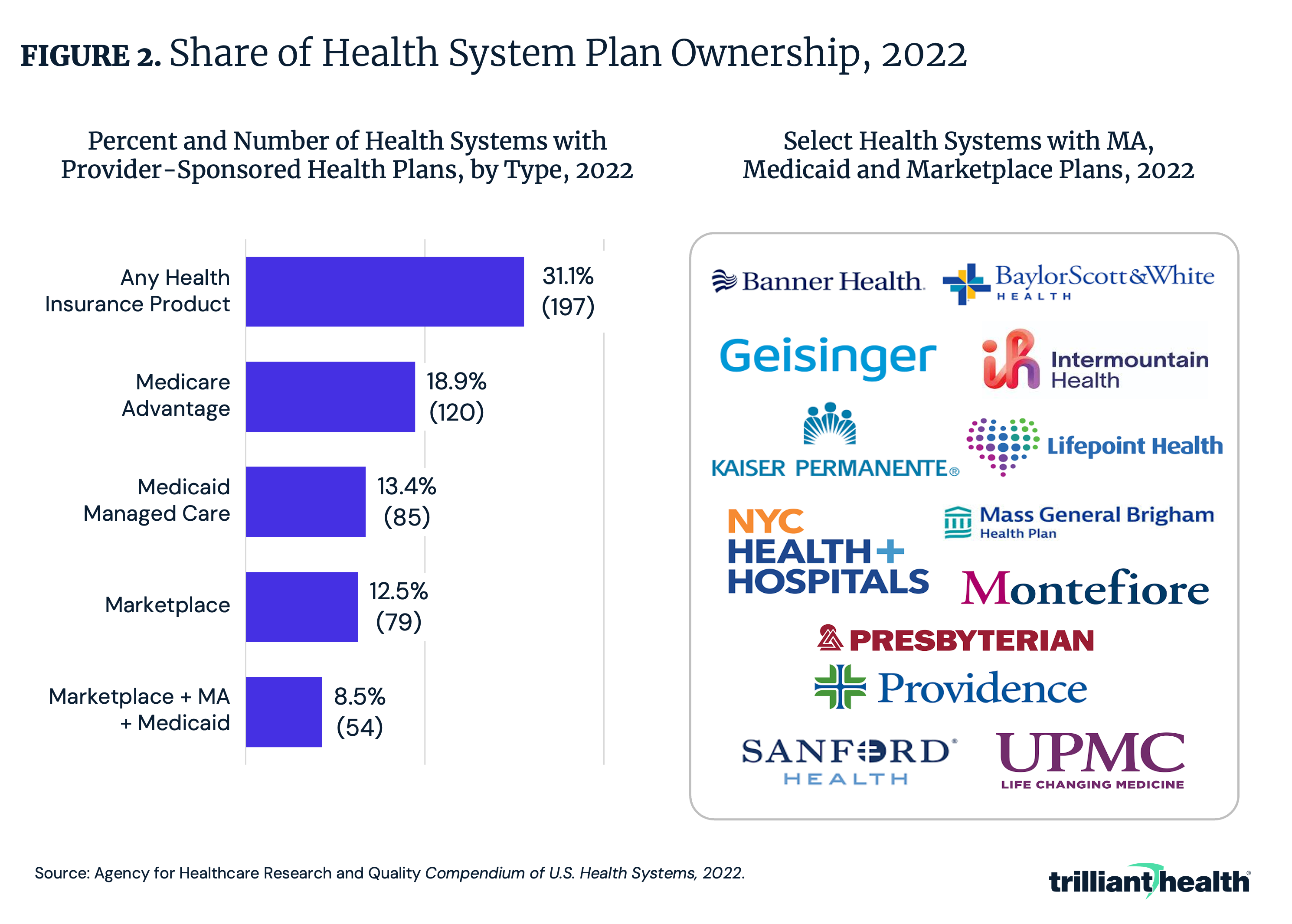

In 2022, 197 health systems, representing 31.1% of all U.S. health systems, offered PSHPs (Figure 2). Of these, 120 (18.9%) offered Medicare Advantage (MA) plans, 85 (12.5%) offered Medicaid managed care plans, 79 (12.5%) offered Marketplace plans and 54 (8.5%) offered all of the above. Notably, prominent health systems such as Kaiser Permanente, UPMC, Baylor Scott & White and NYC Health+Hospitals offered MA, Medicaid and Marketplace PSHPs in 2022.

Thanks to Marina Kheyfets, Sarah Millender and Katie Patton for their research support.