.png)

.png?width=171&height=239&name=2025%20Trends%20Report%20Nav%20(1).png)

Counterpoint

Hal Andrews | August 1, 2023|

The story of Don Quixote recounts the adventures of a would-be gallant knight who imagines that he is doing noble deeds to rescue people in distress. Virtually everyone who encounters Don Quixote quickly realizes that he is a fool. The story of healthcare innovation is of legions of Don Quixotes – benefits brokers, strategy consultants and Beltway policy shops – believing their (often imaginary) “solutions,” or rather PowerPoint presentations, would solve the problems in the U.S. healthcare system. The difference is that, despite repeatedly failing like Cervantes’ protagonist to deliver tangible results, these modern-day Don Quixotes are revered and lavishly remunerated, a not insignificant portion of that oft-cited “healthcare waste.” Over the past few months, Counterpoint has addressed a few of these fantastical quests:

Of course, the most quixotic policy notion of the last 50 years is that the Affordable Care Act (the “ACA”) would constrain healthcare costs. Instead, the ACA codified a “cost-plus” revenue model for commercial health insurance. By requiring that medical loss ratios be 80-85%, the ACA capped profits on commercial health insurance at 15-20%, perversely incentivizing health plans to allow costs to increase in order to increase profits. |

|

The Case for (a Return to) the First Principles of Value For Money in the Health Economy Instead of quixotic schemes that enrich benefits brokers and strategy consultants, America’s healthcare system needs to return to “first principles”: “If we never learn to take something apart, test the assumptions, and reconstruct it, we end up trapped in what other people tell us — trapped in the way things have always been done. When the environment changes, we just continue as if things were the same. First-principles reasoning cuts through dogma and removes the blinders. We can see the world as it is and see what is possible.”1 Stakeholders in the health economy often tout being “consumer-focused” without understanding the “first principles” embraced by every business that is truly consumer-focused: how do we deliver value to our customers? In the health economy, a return to first principles theoretically begins with the Hippocratic Oath. Everyone remembers most of this phrase: “I will do no harm or injustice to them.”2 Although other portions of the Hippocratic Oath are no longer in vogue, even a return to the principle of “do no harm” would account for the variable of safety in the healthcare value equation. In 2009, I co-authored the Hospital Value Index™, which defined value this way: “Value in healthcare is the same thing as value with any other commodity, product or service. Value is the combination of what you receive in exchange for what you paid and the likelihood that you will want it again. The elements of healthcare value include price, quality, efficiency, effectiveness, outcomes, process, experience and on-going perception, to name a few points on our radar. Inherent in value is the cost required to create the good, and the relationship of that cost to its price, demand and availability. Some people believe that paying $150,000 for a Bentley automobile is a good value because of the quality of materials and craftsmanship involved in production, as well as its brand reputation. Other people think that buying ten Bic pens for $3.00 is also a good value, because Bic pens are reliable, efficient and easily replaced. Value in healthcare is difficult because patients are more like Bentleys (they are all different) than Bic pens (they are all the same). Yet a laboratory lipid panel processed by a Bioscanner 2000 with automated output, normal range benchmarks and results reporting is analogous to the Bic pen, demonstrating that some components of healthcare are quite commoditized.” Commoditization in the health economy has accelerated since 2009, with generic pharmaceuticals and LASIK surgery being notable examples. A more recent example is Amazon’s “Prime Day 2023” offer of 24/7 virtual care for $12/month through One Medical. The increasing commoditization is catalyzed by the fact that numerous healthcare goods and services are relatively indistinguishable in quality: an ankle x-ray, a blood draw, a telehealth consultation, etc. As a general principle, commodity goods and price transparency are frequent companions. CMS and Congress are currently myopically focused on hospital price transparency, although CMS recognizes its shortcomings: “In both of those final rules, we stated that our policies requiring public release of hospital standard charge information are a necessary and important first step in ensuring transparency in healthcare prices for consumers. We also recognize that the release of hospital standard charge information is not itself sufficient to achieve our ultimate price transparency goals. The regulations are, therefore, designed to begin to address some of the barriers that limit price transparency, with a goal of increasing competition among healthcare providers to bring down costs.”3 Fortunately, another part of CMS’s Transparency in Coverage initiative – health plan price transparency – reveals an existing market rate for both inpatient and ambulatory healthcare services. As we have previously demonstrated, quality – using CMS mandated reporting measures – is tightly correlated, while negotiated rates for the same plan for the same service in the same market are widely divergent.

Note: Analysis was conducted using negotiated and derived rates (CMS definition) for UnitedHealthcare and Blue Cross Blue Shield of Illinois. Source: Trilliant Health’s national all-payer claims database, Provider Directory and national Health Plan Price Transparency dataset and analysis of Hospital Readmissions Reduction Program (HRRP) data.

Note: Analysis was conducted using negotiated and derived rates (CMS definition) for UnitedHealthcare and Blue Cross Blue Shield of Illinois. Source: Trilliant Health’s national all-payer claims database, Provider Directory and national Health Plan Price Transparency dataset and analysis of Hospital Readmissions Reduction Program (HRRP) data.

Note: Analysis was conducted using negotiated and derived rates (CMS definition) for UnitedHealthcare and Blue Cross Blue Shield of Illinois. Source: Trilliant Health’s national all-payer claims database, Provider Directory and national Health Plan Price Transparency dataset and analysis of Ambulatory Surgical Center Quality Reporting (ASCQR) Program data.

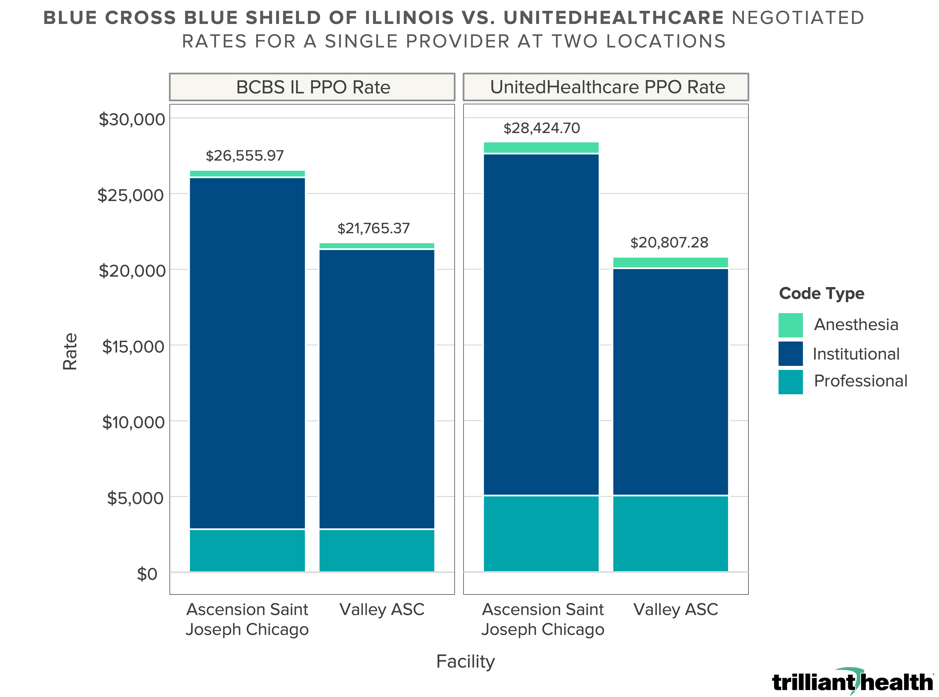

You don’t have to be a partner at McKinsey or Mercer to see that the facility market rate for inpatient joint replacements in Chicago varies by almost 300% – from $16,074.18 to $63,502.46 – while the facility market rate for outpatient joint replacement varies by more than 50%, from $12,193.17 to $18,488.28. Based on the AHA’s logic, prices in Chicago for joint replacements will not regress to the mean but instead rise to the highest published price. I have my doubts. Even as the health plan price transparency data reveals a lack of correlation between quality and negotiated rates, astute observers will note that a market rate already exists in Chicago for joint replacements, obviating the need for every reference-based pricing consultancy. For joint replacements without major complications or comorbidities – DRG 470 – there are 19 hospitals that are in-network with UHC performing the procedure at or below the market mean negotiated rate of $24,362, of which 15 have expected or better-than-expected quality outcomes. Similarly, for joint replacements with major complications or comorbidities – DRG 469 – there are 20 hospitals that are in-network with BCBS IL performing the procedure at or below the market mean negotiated rate of $41,108, of which 17 have expected or better-than-expected quality outcomes. How does this manifest in real life for consumers and employers? Take, for example, a physician who routinely performs knee replacements on UHC and BCBS IL patients at two different locations:

Note: Analysis was conducted using negotiated rates (CMS definition) for UnitedHealthcare and Blue Cross Blue Shield of Illinois. (June 2023 file) Source: Trilliant Health’s national all-payer claims database, Provider Directory and national Health Plan Price Transparency dataset.

Logic, and basic economic principles, would suggest that every provider must be able to deliver services profitably at, or even slightly below, the market range of reimbursement for a particular service or exit that service line. Harvard’s Regina Herzlinger wrote about this in 1997: “The American health care industry is filled with opportunities to establish focused factories, ranging from those that perform only one procedure, like cataract surgery, to those that provide the full panoply of care for a disease like cancer. To fulfill the promise of focused factories, however, the industry will have to resize – that is, replace its unfocused multipurpose providers and redundant, underutilized technology with muscular focused factories, loaded with cost-saving, quality-enhancing medical technology.”4 In an era where everyone wants simple answers, health plan price transparency data provides one. Employers could bend the cost curve significantly merely by steering “away” from a handful of providers who are outliers on price or quality for a particular service line, in turn revealing the fallacy of “narrow networks” and steerage “to” a limited set of providers. Whether health plans and brokers fail to understand this or have instead chosen not to share this with employers is an interesting question. Your government affairs team will confirm that CMS and Congress are determined that every American can see what I can see in the health plan price transparency data. What I can see will be kryptonite to numerous renowned franchises in the health economy, absent a return to first principles. Is your franchise one of them?

1. https://fs.blog/first-principles/ 2. https://www.nlm.nih.gov/hmd/greek/greek_oath.html 3. https://public-inspection.federalregister.gov/2023-14768.pdf#page=754 4. Herzlinger, Regina. Resizing – The “Trade Fat For Muscle Diet.” Market-Driven Health Care, Addison-Wesley Publishing Company, Inc., 1997, page 158. |

%20.png?width=2632&height=1414&name=DRG%20469%20(HIP%20%26%20KNEE%20REPLACEMENT%20WITH%20MCC)%20.png)

.png?width=2562&height=1398&name=DRG%20470%20(HIP%20%26%20KNEE%20REPLACEMENT).png)

%20.png?width=2796&height=1056&name=CPT%2027447%20(TOTAL%20KNEE%20ARTHROPLASTY)%20.png)