.png)

.png?width=171&height=239&name=2025%20Trends%20Report%20Nav%20(1).png)

Key Takeaways

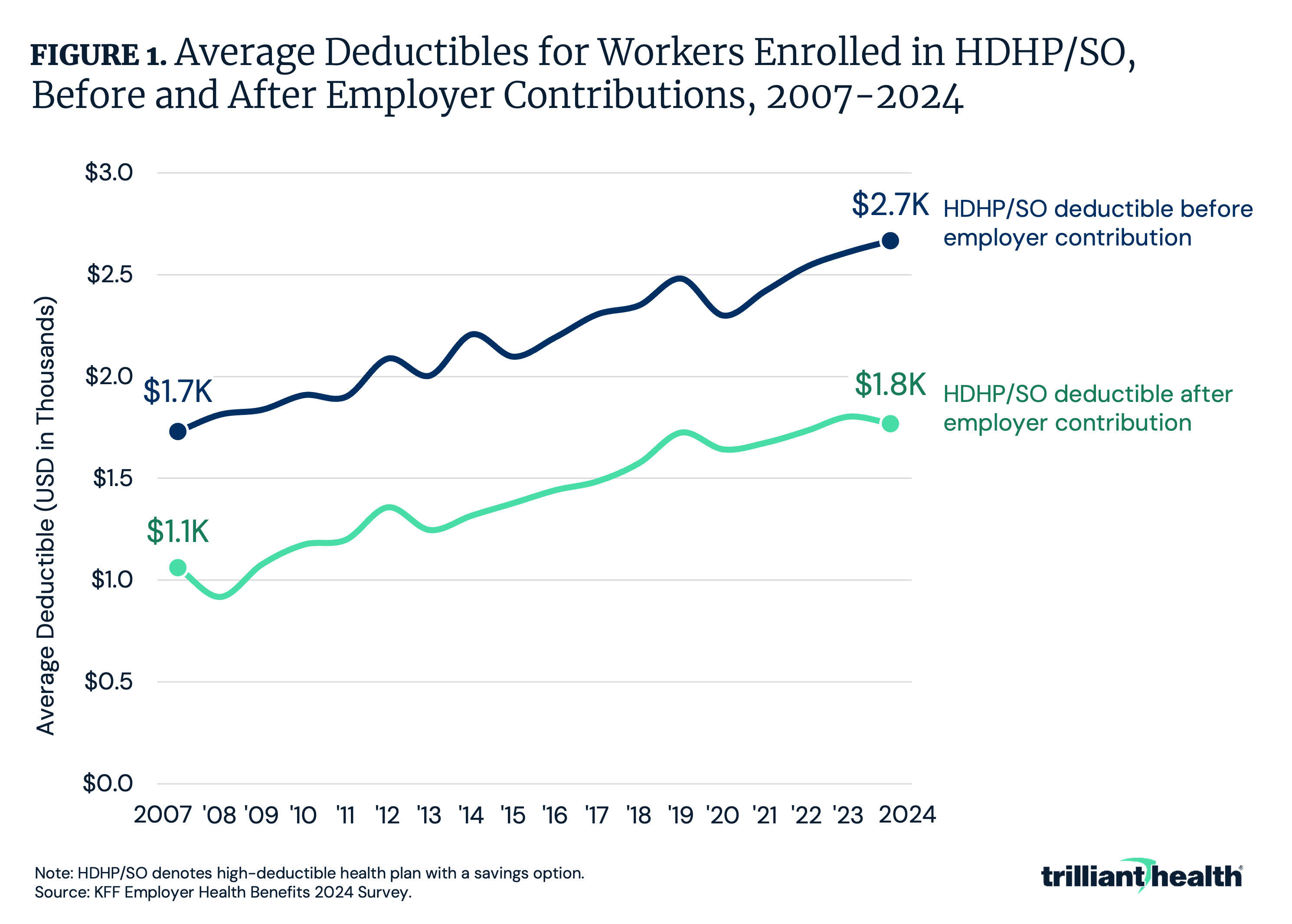

- Since 2007, average deductibles for employees with HDHPs that include savings options, like HRAs or HSAs, have risen by 54.2%, reaching $2.7K in 2024. After accounting for employer contributions, the net increase in HDHP deductibles is 66.6%, reflecting how increases in employer contributions are not keeping pace with growth in HDHP deductibles.

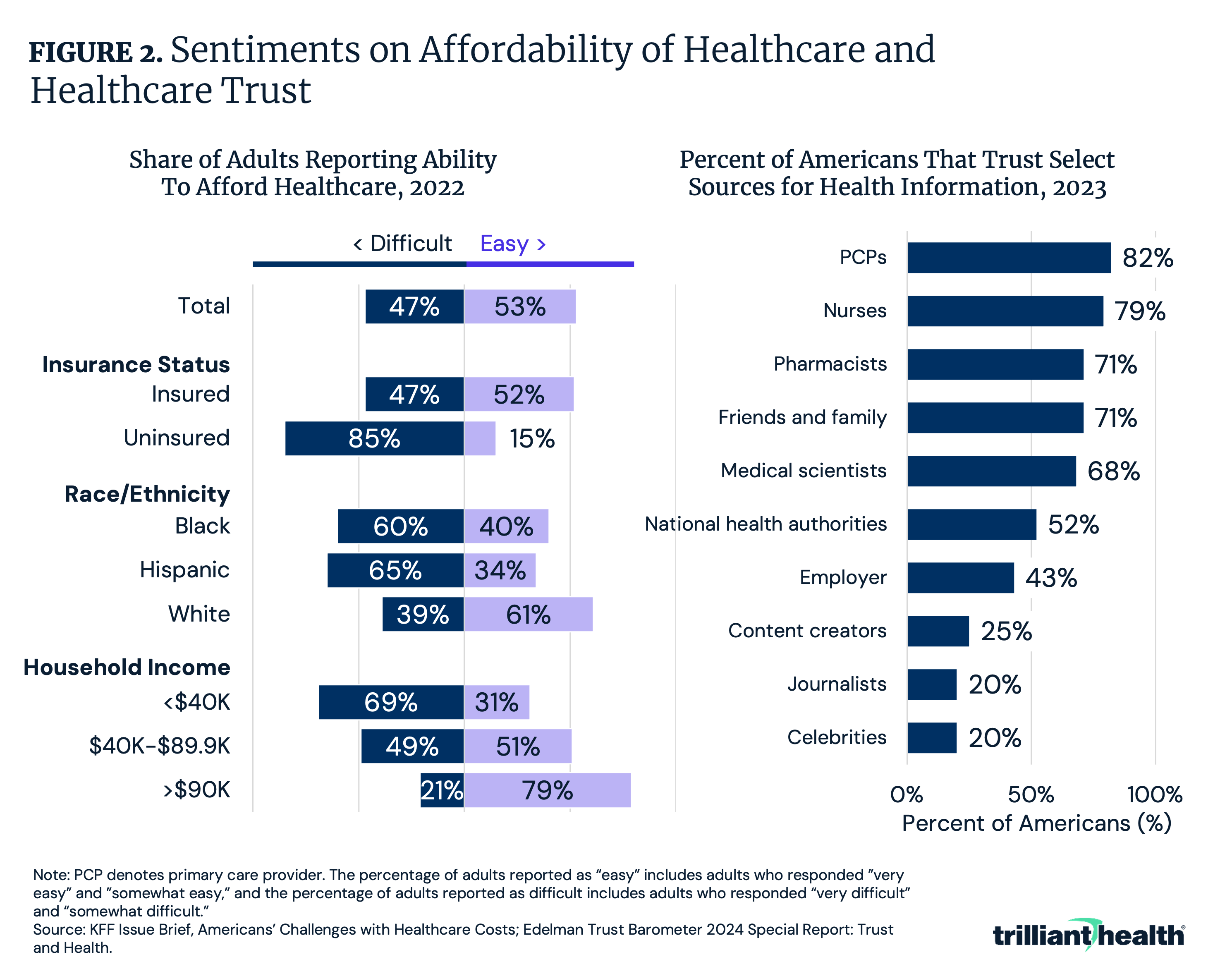

- Among insured Americans, nearly half (47%) find it difficult afford healthcare costs. This share is even higher among the uninsured at 85%.

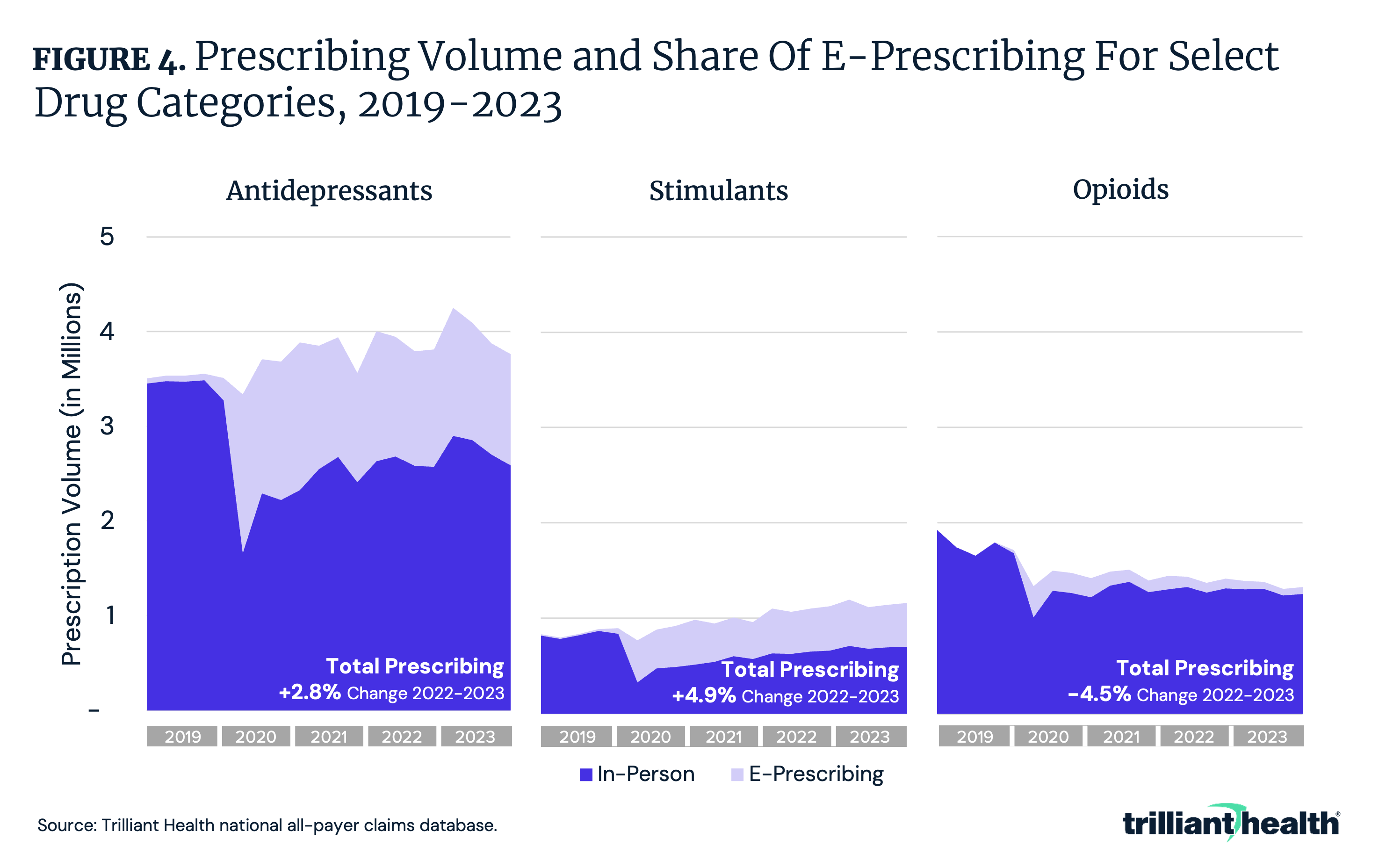

- Tele-prescribing has increased across drug classes since the COVID-19 pandemic. As of Q4 2023, 31.3% of antidepressant prescriptions, 39.9% of stimulant prescriptions and 5.6% of opioid prescriptions originated from a telehealth visit.

Forced consumerism in healthcare, driven by patients having increased “skin in the game,” has not generated tangible systemic value but has led to fragmentation. Patients face increasingly expensive choices for potential treatment paths without clear guidance on the quality or value of those options. This information asymmetry forces patients to navigate a complex web of providers and services to discover the most affordable option within the constraints of provider networks and referral patterns. They also face the added challenge of evaluating direct-to-consumer options, which may be more affordable but often exist outside of the “traditional” healthcare system. The complexity of this task is further compounded by the lack of price transparency in the U.S. healthcare system.

This week, we examine how fragmentation within the healthcare system creates gaps in care and inconsistent quality, fostered by forced consumerism (Trend 6 of our 2024 Health Economy Trends Report).

Continuously Increasing Deductibles Are Not Consumer Friendly

Although high-deductible health plans (HDHPs) were introduced to reduce employee spending on healthcare by increasing employee control, deductibles for these plans have continuously increased, diverging from this original purpose. Since 2007, average deductibles for employees with HDHPs that include savings options, like Health Reimbursement Arrangements (HRAs) or Health Savings Accounts (HSAs), have risen by 54.2%, reaching $2.7K in 2024 (Figure 1). After accounting for employer contributions, the net increase in HDHP deductibles is 66.6%, reflecting how increases in employer contributions are not keeping pace with growth in HDHP deductibles. The increasing financial responsibility has left many employees struggling to cover out-of-pocket costs, prompting some to delay or forgo necessary care, ultimately undermining the intended benefits of HDHPs.

As Fewer Americans Can Afford Healthcare, More Are Looking to Non-Traditional Sources for Health Information

Nearly half (47%) of insured Americans and 85% of uninsured Americans find it difficult to afford healthcare costs (Figure 2). The financial strain not only limits access to care but may also contribute to the growing number of patients seeking non-traditional sources of health information. While most Americans (82%) still trust primary care providers (PCPs) as a source of health information, the high costs of care and undersupply of PCPs can serve as a barrier to solely relying on physicians for direct health advice. Notably, a quarter of Americans report trusting social media content creators for health information, compared to 52% who report trust in national health authorities. To the extent that unaffordable or unexpectedly high-cost care causes people to distrust or avoid seeking care from traditional providers, the more challenging care coordination becomes.

Patients and Health Institutions Have Differing Perspectives on the Continued Adoption of Telehealth

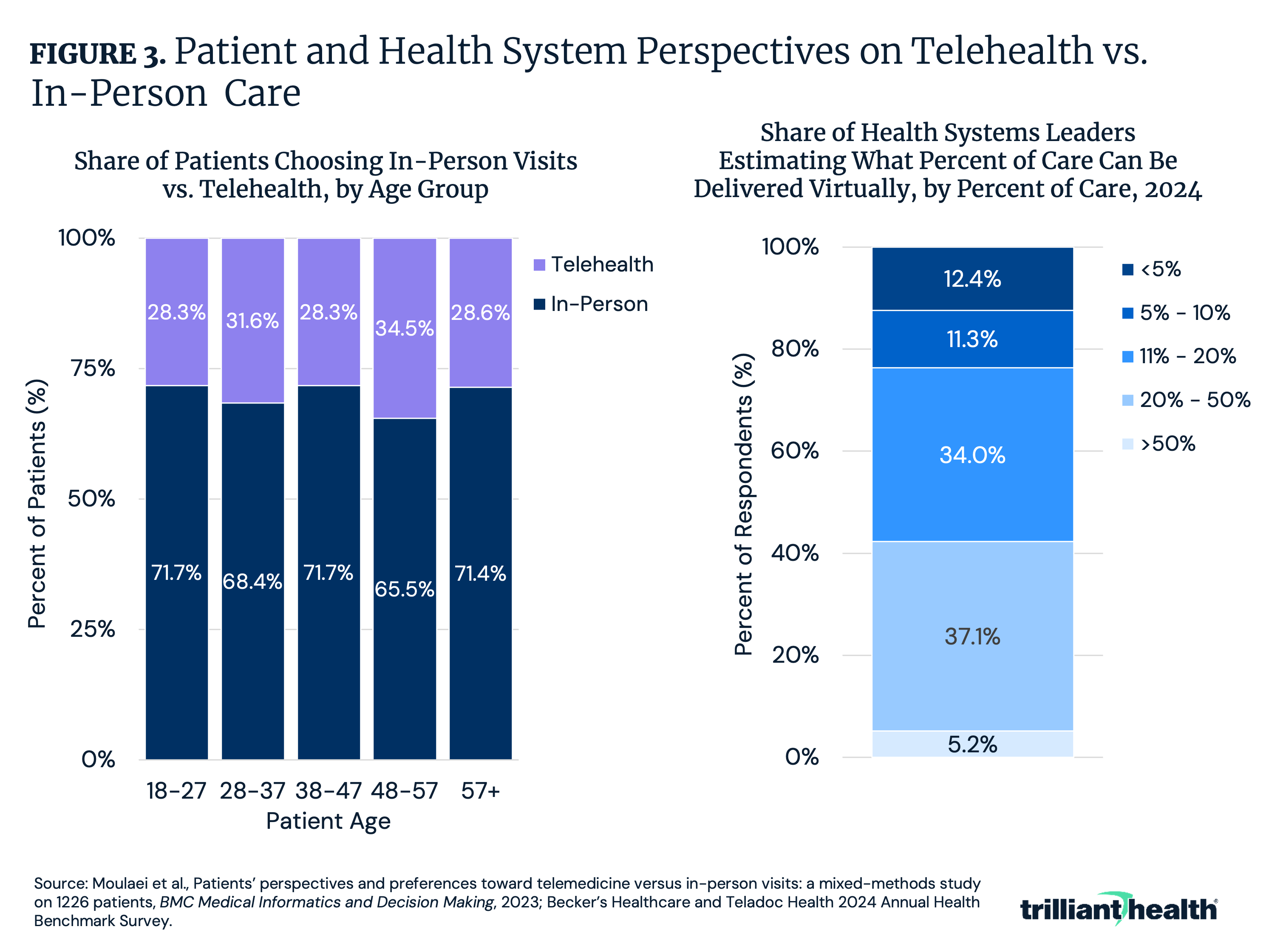

Across age groups, 65% of patients prefer in-person visits to telehealth visits. Surprisingly, patients aged 18-27 and 38-47 reported the highest preference for in-person care, at 71.7% (Figure 3). Despite a clear preference for in-person care, many health systems are continuing to prioritize investments in digital tools like telehealth. As of 2024, the leading investment focus for health systems is expanding virtual health to enhance patient experience and access, with 88.5% of health system executives having implemented or planning investments in this area.1 Additionally, 42.3% of leaders believe that at least 20% of all care types could be delivered virtually, highlighting a potential gap between patient preferences and health systems' digital strategies.

Trends in E-Prescribing for Select Medications

Tele-prescribing has increased across drug classes since the COVID-19 pandemic. Tele-prescribing for controlled substances like opioids and stimulants increased due to pandemic-era regulatory flexibilities but continues to represent a noteworthy share of prescribing. As of Q4 2023, 31.3% of antidepressant prescriptions, 39.9% of stimulant prescriptions and 5.6% of opioid prescriptions originated from a telehealth visit (Figure 3). While tele-prescribing can improve access to medications for many patients, it also raises new questions about regulation and oversight, especially for controlled substances. As health systems and regulators evaluate the future of tele-prescribing policies, balancing accessibility with patient safety will continue to be a critical focus.

Conclusion

The proliferation of forced consumerism in healthcare has created an increasingly unaffordable and fragmented system that does not consistently deliver cohesive, high-value care. Patients face mounting challenges, from managing rising out-of-pocket costs and high deductibles to navigating a complex landscape of provider networks, direct-to-consumer options and telehealth services. While financing innovations like HDHPs and technological innovations like telehealth were designed to enhance choice and access, the unintended consequences have unduly burdened patients financially and introduced added friction, respectively. As healthcare costs continue to rise, patients are increasingly turning to non-traditional sources for health information, many of which may lack medical accuracy and oversight.

In what ways can technology help consumers make better healthcare decisions without further fragmenting their care? How can we balance consumer-driven care with the need for integrated, coordinated care delivery? What tradeoffs are Americans willing to make for convenient care and do they understand these tradeoffs? Are payers, employers and providers prepared to educate consumers about these tradeoffs? What are the clinical implications for patients receiving “transactional” care in the form of prescriptions as opposed to longitudinal care management with established providers? As the healthcare landscape evolves, addressing these gaps will require a focused effort to balance costs, access and information transparency. Only by aligning healthcare strategies more closely with patient needs can we begin to reduce fragmentation and foster a more cohesive, value-driven system that prioritizes both health outcomes and patient experience.

Update: for the latest on this topic, including the rise of direct-to-consumer prescribing and diagnostics, read our 2025 Trends Shaping the Health Economy Report.