.png)

.png?width=171&height=239&name=2025%20Trends%20Report%20Nav%20(1).png)

Counterpoint

Hal Andrews | August 10, 2022As noted in Part II, there are 927 CBSAs in the United States, of which 225 have the maximum HHI score of 10,000 because the “market is controlled by a single firm.”1

Read that again – “controlled by a single firm.” What does that even mean? What are the market characteristics of the markets that are “controlled by a single firm?” How do these markets “controlled by a single firm” compare to the 702 CBSAs that are not “controlled by a single firm?” How is it that the U.S. government uses such a simplistic formula as the key ingredient in analyzing competitive effect in 927 widely divergent and diffuse CBSAs?

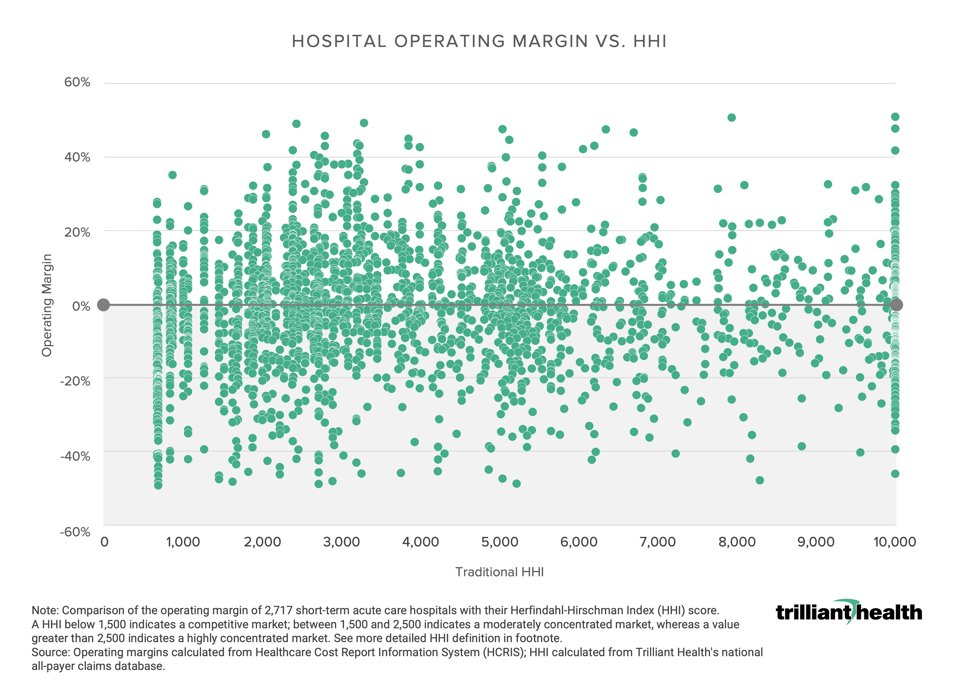

An equally simple analysis reveals the fallacy of HHI for healthcare markets, as there is no discernible correlation between average hospital operating margin and market competitiveness, for reasons discussed in Part II.

Notably, the average operating margin of a hospital with a maximum HHI score of 10,000 is negative: -0.98%. In 44 of the 225 CBSAs “controlled by a single firm,” that single firm has an operating margin higher than 10%; in contrast, in 132 CBSAs “controlled by a single firm,” that single firm’s operating margin is negative. Only in healthcare does the average monopoly generate negative operating margins.

What characterizes “monopoly” healthcare markets is not monopolistic behavior by a single hospital or health system but rather insufficient demand to support a duopoly. The lack of demand in these markets is not uniformly characterized by inability to pay, although “monopoly” healthcare markets are invariably poorer than those that are not monopolies. Instead, the lack of demand results from a population that is too small to support two firms delivering duplicative services, irrespective of the price of those services.

Industry pundits prattle incessantly about the “waste” in the U.S. healthcare system. Is it possible that a significant part of the waste might possibly be needless duplication of the most expensive part of the healthcare system?

It is inevitable that more U.S. hospitals will close, as the demand for their services is increasingly inadequate to generate revenue sufficient to offset the massive capital, operating and labor costs of simply keeping a hospital open. A myopic focus on the market share for inpatient services in any market as a proxy for competition for healthcare services in that market only serves to delay the inevitable.

The result? America trades idyllic and academic notions of price competition for the inevitable waste of duplication of government-mandated services and the decline in quality that manifests with declining volumes. The American people are better served by market-driven rationalization of duplicative healthcare services than government-mandated asphyxiation of them, as anyone who has witnessed the closure of a hospital knows with certainty.

Alas, we get the government – and the healthcare system – we deserve. In the words of an industry sage from Florence, Alabama, “the healthcare system works exactly as it is designed.”

Perhaps the system would be different if industry lobbyists focused their energies on something other than gaming the system or delaying the inevitable, as they did with readmission penalties and price transparency and medical loss ratio calculations and Medicare Star Ratings, and generic drugs.

Of course, if the Federal government and the healthcare industry wanted real competition, employer-paid premiums for health insurance would not be tax-deductible…