Notably, HCA’s financial results during 2020 were the best in HCA’s history (until 2021) despite significant year-over-year declines in admissions, surgeries and emergency room visits. The explanation? Rate.

What makes HCA’s enviable success in negotiating managed care rates more remarkable is the longstanding information asymmetry between the providers of healthcare services – physicians, clinics, surgery centers, hospitals – and health insurers. Similarly, that information asymmetry has allowed health insurance brokers to treat employers and employees like mushrooms for decades.

Ironically, this information asymmetry has been not only endorsed but also enforced by the Federal government, with the Sherman Act forbidding disclosure of negotiated rates for healthcare services, among other things. Until last month, the best that a provider could hope for was to meet the safe harbor issued by the Department of Justice to understand “market rates” cobbled together by Truven and Lexis/Nexis. In a slightly surprising development, the DOJ withdrew that guidance on February 3, 2023, upending decades of precedent.1

Additionally, as discussed in last month’s Counterpoint, the abject failure of dozens of value-based care initiatives is most attributable to one factor: the inability of providers to understand the total cost of care for any patient cohort. The result? Policymakers and pundits decry the spiraling costs of U.S. healthcare even as no health economy stakeholder can do anything about it without either violating the law or jeopardizing their financial performance.

Instead of focusing on the potential benefits of eliminating longstanding information asymmetry in price, policy wonks have suddenly decided that price fixing by the government – which the Sherman Act prohibits among market participants – is the solution to the undeniable healthcare cost crisis in America. In February 2021, the Rand Corporation published a report titled “Impact of Policy Options for Reducing Hospital Prices Paid by Health Plans,” which was repeatedly cited in the Congressional Budget Office’s report “Policy Approaches to Reduce What Commercial Insurers Pay for Hospitals’ and Physicians’ Services” released in September 2022.2,3

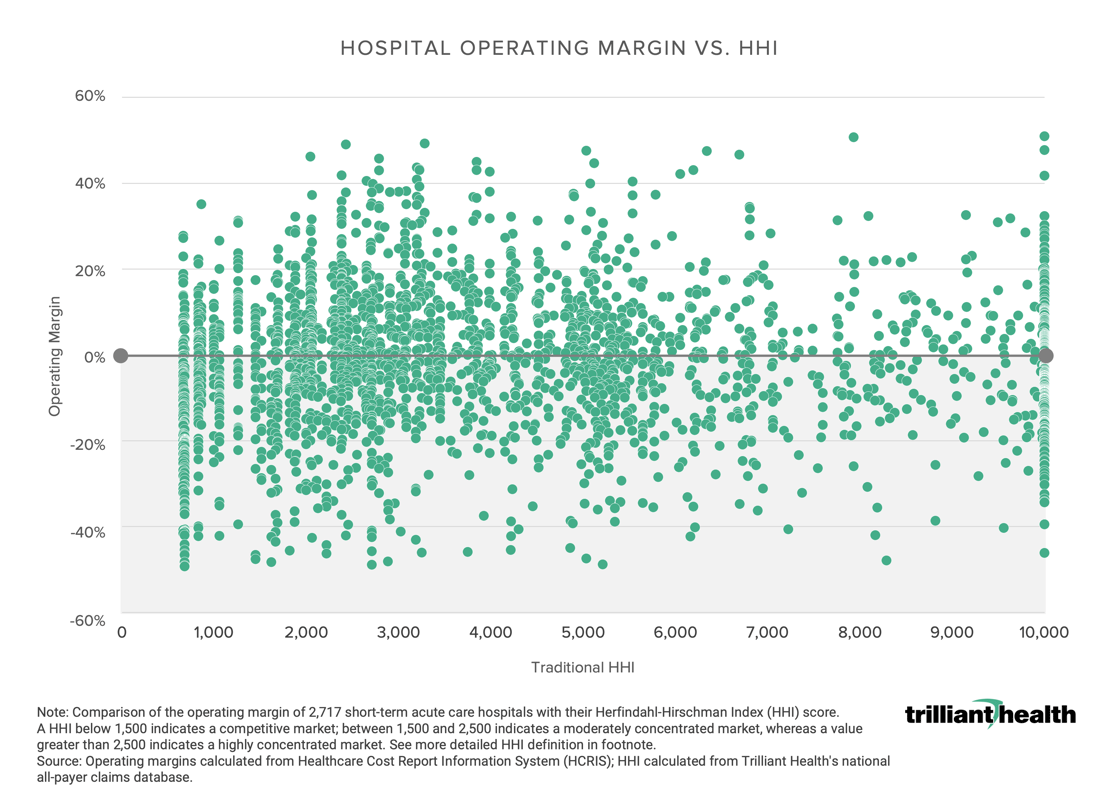

The most recent example is the fantastic assessment of price regulation in “A Road Map for Action” published in Health Affairs last month, which “believes that it is important to open the door to regulating some provider prices in some settings” and recommends Federal and state intervention to increase competition “by increasing the number of competitors, either by inducing more market entrants or by breaking up existing combinations in service lines where there could be more sellers of efficient size.”4 As to the former, Joseph Schumpeter noted that “history is a record of ‘effects’ the vast majority of which nobody intended to produce,” and it is easy to imagine how “regulating some provider prices in some settings” might evolve. As to the latter, recommending duplication of service in the world’s most expensive healthcare system as a cost reduction measure is a bit peculiar, particularly in the midst of a provider staffing shortage.

The thought of imposing a utility-like regulatory structure on the already heavily regulated healthcare industry, particularly hospitals, is interesting on many levels. America’s electric grid and hospitals share an aging infrastructure, and both have endured capacity challenges in the past few years. At the same time, the history of regulatory intervention in U.S. electricity markets reveals uneven and unexpected results, as this paper from the Department of Justice describes:

In the 1990s, consumers became increasingly dissatisfied with regulated prices as the high capital costs of nuclear and other investments in prior decades continued to be reflected in rates, while innovative generating technologies and low natural gas prices made potential alternative sources seem very attractive. Furthermore, the experience from the deregulation of other industries, such as airlines and trucking, suggested that profit motives could lead to more efficient operations and investment and that price competition could ensure that these efficiency improvements were passed on to consumers.5

While the Health Affairs authors correctly note that “[h]igh prices relative to costs should entice providers to enter markets and innovators to find cost-saving strategies,” they fail to mention the recent investments in healthcare made by the largest retailers in the economy, each of which clearly promotes (radically) lower price points than traditional healthcare providers. Moreover, the Health Affairs authors suggest, without apparent irony, that the solution for rural hospitals “is a fixed payment to local hospitals to cover their fixed costs (based on their market share),” which sounds a lot like cost-based reimbursement. Most notably, the authors’ enthusiasm for “administered prices” fails to consider the long-term implications on care access and quality, most recently demonstrated by the catastrophe unfolding throughout the National Health Service in England.6

As the DOJ paper states:

The goal of market restructuring should be to create an environment that encourages operational efficiencies and economically justified investment decisions while limiting market power, the cost of implementing competition and any adverse impact on reliability (or perhaps even putting in place reliability improvements). If that kind of environment can be fostered, then consumers will benefit from restructuring in the long run.7

Perhaps unsurprisingly, none of the articles promoting price regulation as a panacea address the one thing that keeps consumers from price discovery for healthcare services: the tax deduction for employer-sponsored health insurance premiums. Instead of employing classic economic principles to encourage “free market” characteristics like most every sector of the American economy, the “experts” recommend increased government intervention to codify, or rather fossilize, a Byzantine reimbursement scheme while simultaneously promoting value-based care.

Federal action to create a true “market economy” for healthcare through the elimination of the tax deduction for employer-sponsored health insurance seems unlikely. As a result, in the words of the Allman Brothers, there “ain’t but one way out” of what ails the America’s “system of care”: health plan price transparency.

The American Hospital Association fought against price transparency by claiming that price transparency would lead to increased prices, citing a 1997 study of ready-mix concrete in Denmark.8 That is not, of course, the American experience, as vividly demonstrated by President Carter’s deregulation of the airline industry and the power of the Internet to inform consumers about cost, quality and value of common goods and services, which Southwest Airlines, Sprint and Charles Schwab notably exploited.9,10 And, of course, concrete as a product is less susceptible to significant innovation than a basket of healthcare goods and services that can increasingly be delivered in a variety of care settings, including the home.

Rate opacity has been the “secret sauce” for every health economy stakeholder for decades, the most important element in competing, if blindly. Health plan price transparency should force health economy stakeholders to compete on cost and quality and access and convenience, which the rest of the economy knows are the elements of value. Many things in healthcare, like flu shots and ankle x-rays and cataract surgery, are commodities; increased price transparency coupled with technological advances leads to increased commoditization, which generally leads to lower price.

In a world of health plan price transparency, can HCA continue to command its current negotiated rates based on value? Can UnitedHealthcare defend its network rates based on its MLR? Can you justify your rates to consumers? If you are explaining, you are losing…

.png?upscale=true&width=1120&upscale=true&name=Copy%20of%20Article%20%232%20Cover%20(2).png)